tobiasjo/E+ via Getty Images

iShares MSCI Peru ETF (NYSEARCA:EPU) is an exchange-traded fund that provides investors with exposure to Peruvian stocks. While iShares suggest the fund is exposed to a “broad range of companies in Peru”, bear in mind that Peru’s equity market is not especially developed; EPU had only 26 holdings as of January 20, 2023. The expense ratio is reported as 0.58%.

The fund is based on its chosen performance benchmark, the MSCI All Peru Capped Index. This is a capped version of the regular MSCI Peruvian equity index. Essentially the purpose of the capped version is to limit the size of certain holdings; in this case, the main effect is to prevent the largest holding from exceeding 25% of the portfolio. The largest holding is Southern Copper Corp (SCCO). SCCO represented 24.66% of the fund as of January 20, 2023.

SCCO is a mining company which, as you might have guessed from the name, mines copper. The company also mines molybdenum, zinc, and silver. It is one of the largest copper mining companies in the world. Copper is an industrial metal and tends to appreciate in price (and demand, etc.), during up-swings in the global business cycle. We are currently in recessionary territory, so it would be unsurprising to see EPU performing badly. Including SCCO, EPU has significant exposures to cyclical stocks (see below).

Morningstar.com

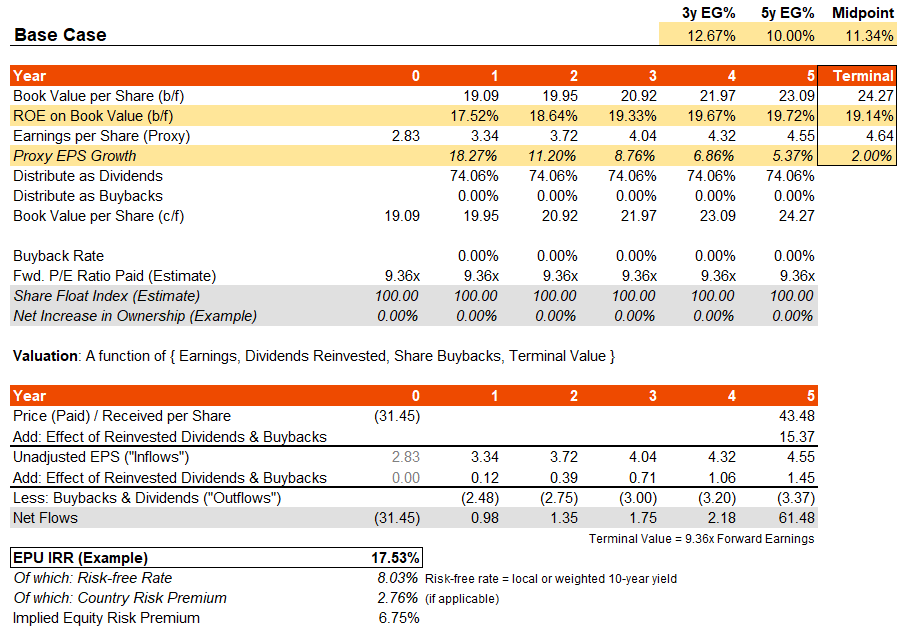

According to Morningstar, the fund’s forward price/earnings ratio was 9.36x as of recent, with a price/book ratio of 1.64x, implying a forward return on equity of circa 17.5%. Given a trailing price/earnings ratio of 11.07x from iShares, EPU’s forward one-year earnings growth forecast is thus circa 18.3%. Morningstar’s consensus analyst estimate for three- to five-year average earnings growth is some 11.36%. Assuming that is the case, and EPU’s portfolio holds up in terms of long-term price/earnings multiple, and continues to pay out large dividends, the forward IRR is strong (see below).

Author’s Calculations

The implied IRR is circa 17.5%. Bear in mind that local interest rates are high; the Peruvian 10-year yield is over 8%. Meanwhile, Professor Damodaran suggests a country risk premium of almost 3%. The underlying ERP is therefore roughly 6.75%, which is admittedly very healthy after accounting for high local interest rates and an already risk-adjusted ERP (with the CRP included).

The forward earnings multiple is a source of risk, perhaps; however, it is both low in nominal terms and relative terms. For example, while core inflation rates in Peru have risen recently, to about 6.5% year-over-year, they have risen almost everywhere in the developed (and less developed) world. Assuming Peruvian inflation rates fall back to trend, it is unlikely the local 10-year would hold at over 8%. Let’s say it’s back down to 6% at most in five years’ time, and assume an ERP of at least 5.5%, with a 2% nominal earnings growth rate (actually below the current 25-year average for core inflation). That would result in an implied forward price/earnings multiple of 10.53x, following a “Gordon growth model” approach. I would not assume P/E expansion given local idiosyncratic risk as reflected in the CRP recommendation from Damodaran. However, it suggests that the current earnings multiple is at a reasonable floor.

Having said all this, while holding onto Peruvian equities is likely to generate a strong return in nominal terms, there are two further important considerations. One is the business cycle, and our current global positioning. The second is FX risk. Firstly, we are heading into a recessionary period for the global economy. Nevertheless, equities have already fallen substantially across the world, and so it is possible we are nearing (or have already seen) the lows, with equity markets generally leading the real economy by 6-18 months (variable; assume around 12 months).

Fidelity.com

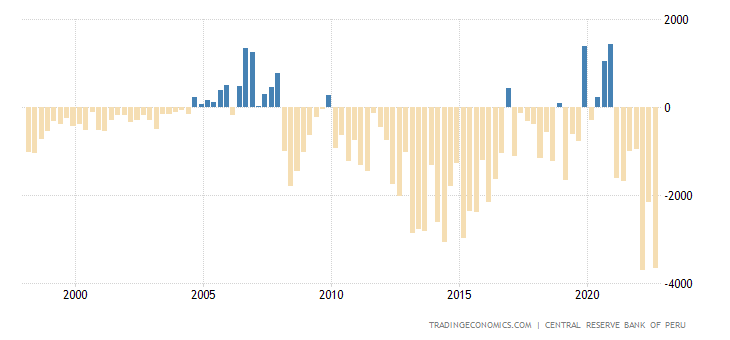

As for FX risk, you have a sharp current account deficit locally (see below), albeit on a PPP basis you have a possibly fairly valued currency (perhaps even undervalued). Also, the nominal interest rate differential is greatly in favor of the Peruvian sol. PPP values matter less than yield differentials in good times; if equity markets turn up, it is possible that the current account will improve and inflows will support local FX strength.

TradingEconomics.com

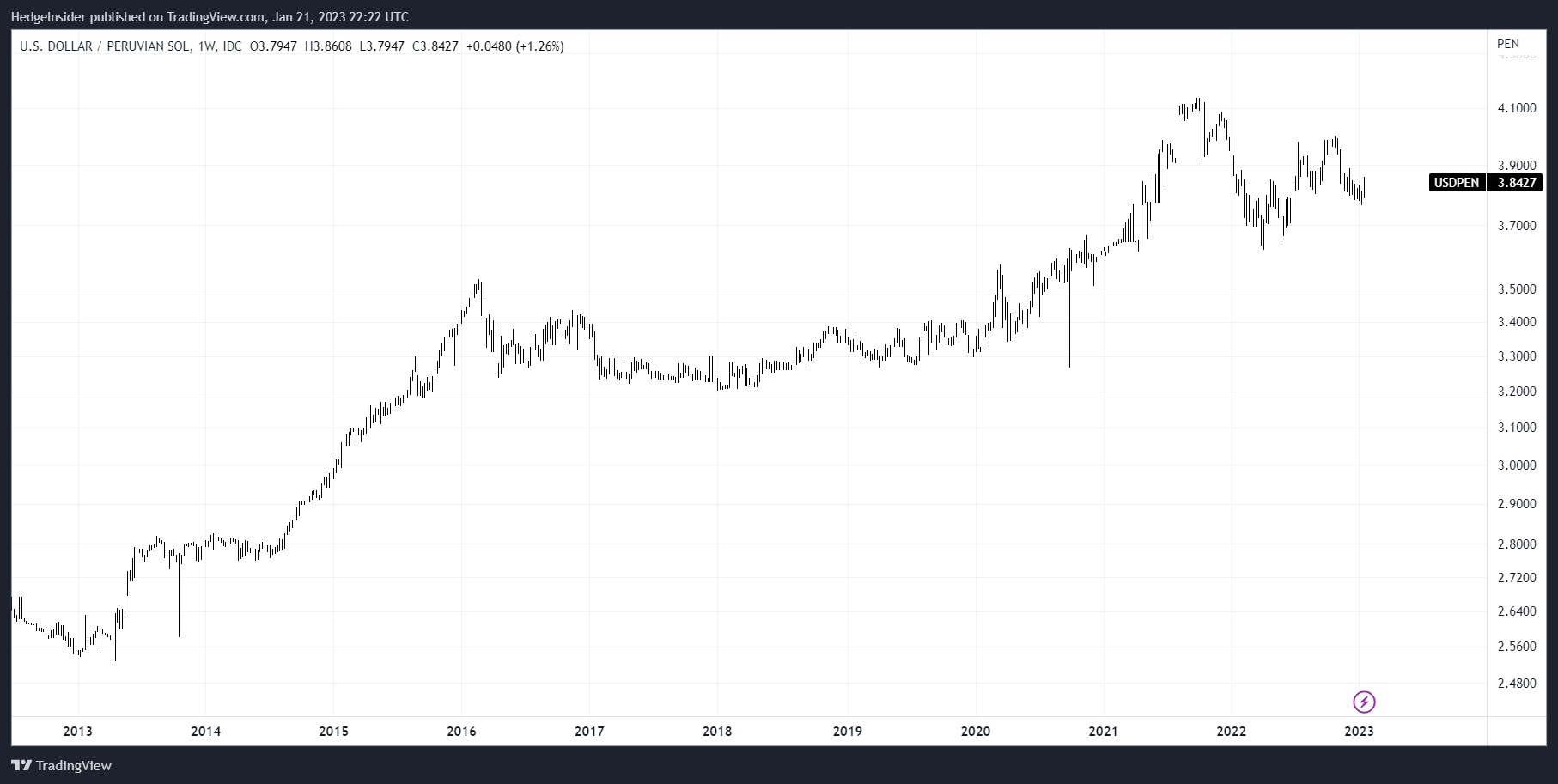

Local FX strength will support Peruvian sol-denominated equities that fall under EPU’s portfolio, thus improving value in USD terms. However, this is risky. EPU offers a high nominal IRR, but it is certainly a cyclical bet. I would also peruse the FX chart and note that for USD/PEN (the exchange rate for U.S. dollars into Peruvian sols), the sol is trading poorly relative to 2015 when the local current account was similarly bad in nominal terms.

TradingView.com

Therefore, perhaps further sol (or “PEN”) downside is unlikely, and perhaps we are finally ready to see a bounce-back in EPU.

I think it is important to note here, though, that while EPU likely offers a strong multi-year return (with dividends reinvested, and the expense ratio both included), EPU would be a multi-year hold. On a valuation basis, the high nominal IRR is close to being fair. It might be on the high side, and thus on a raw valuation basis EPU probably deserves to be trading between 5-15% higher than present prices, yet most of the upside is long term.

I would take a bullish view on EPU, as I am optimistic for global equities and the global economy on a multi-year time horizon. However, this is strictly a long-term view.

Be the first to comment