aerogondo

Introduction

EPR Properties (NYSE:EPR) is a real estate investment trust (REIT) that specializes in the ownership of properties related to the entertainment industry. The portfolio of the company includes a diverse range of properties such as movie theaters, theme parks, and family entertainment centers.

The future of EPR Properties is largely dependent on the future of AMC Entertainment (AMC) (APE). While AMC Entertainment’s debt levels are skyrocketing and its free cash flow is negative, I believe AMC is in big trouble. Many polls show that people prefer to watch new movies at home rather than going to the theater. It’s like comparing the internet to books in 1999.

EPR Properties’ Future

EPR primarily rents to movie theaters, with AMC Entertainment as its largest tenant. The movie theater industry does well when the economy is doing well but can struggle during a recession. Regal’s parent company, Cineworld, has recently filed for Chapter 11 bankruptcy in October of 2022.

Since the Corona crisis, AMC Entertainment has also been in troubled water. AMC Entertainment is a movie theater chain that saw significant revenue declines as a result of the Corona crisis measures.

With the help of meme investors, AMC Entertainment was able to avoid bankruptcy in early 2021. A gamma squeeze occurred when short sellers were forced to buy AMC stock because its price had soared after the cash infusion. AMC saw an opportunity to avoid bankruptcy by raising funds through the issuance of stock. The business had financially improved. Now, there are fresh rumors of impending bankruptcy.

Let’s delve into AMC a little deeper. From the company’s balance sheet, we can see that AMC has $685M in cash and short-term investments. It has a total debt of $5.3 billion (a net debt of $4.6 billion). For a number of years now, AMC’s debt level has steadily risen while its free cash flow has been negative. Debt must be refinanced therefore prior to maturity, which is unfavorable in the current high interest rate environment. Considering that the company generated $620M in EBITDA for 2019, the ratio of its current net debt to that figure is still very high at 8.8. Thus, its future rests on the willingness of its creditors to refinance its debt. If interest rates rise sharply, interest coverage will fall. AMC could be in trouble if it couldn’t meet its debt obligations.

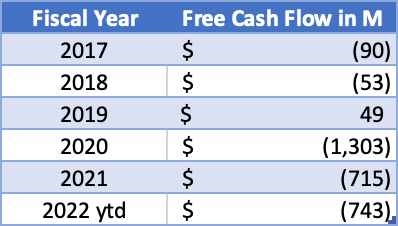

AMC’s free cash flow (SEC and author’s own calculations)

Another movie theater, the parent company of Regal Cinemas, Cineworld, has filed for chapter 11 bankruptcy in October 2022. Cineworld financials didn’t look good as it has net-debt of $5B. In a good year like 2019, EBITDA was $843M. Net-debt to 2019 EBITDA ratio was very high at 6. AMC’s ratio is higher at 8.8. So yes, investors are rightly concerned about the future of AMC Entertainment.

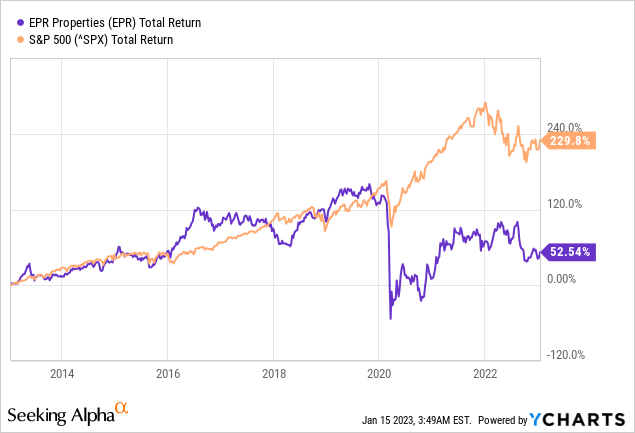

Investors sold the stock, causing the price to fall. The stock has performed poorly in recent years, with a total return of only 53% over the past 10 years. But over the long term, the stock outperformed the S&P500.

There is a significant risk that EPR will lose its largest tenant, AMC Entertainment, if the company goes bankrupt. Data from the 2019 fiscal year’s annual report:

For the year ended December 31, 2019, approximately $123.8 million or 17.6% and $75.8 million or 10.8% of the Company’s total revenue (including revenue from discontinued operations) were derived from rental payments by AMC and Regal, respectively.

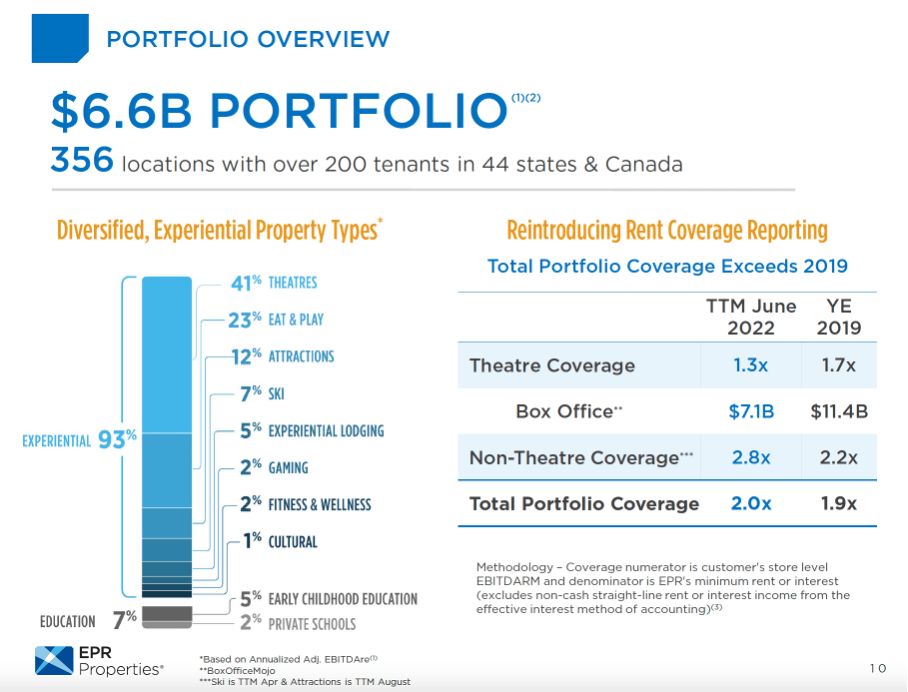

EPR Properties is gradually getting out of the exposure to movie theater businesses. Third quarter results show that cinemas accounted for 41% of total sales in that quarter. In 2019, this figure was 45%. I think this is still a high allocation for a high-risk sector.

EPR’s Portfolio Overview (3Q22 investor presentation)

Looking ahead, I anticipate that movie theaters will become less popular as streaming becomes more popular. People can rent a movie and watch it with their family or friends at home. According to Grand View Research, the movies and entertainment market will grow at a 7.2% CAGR from 2022 to 2030. The following are growth drivers from the report:

New marketing and distribution platforms, such as IPTV, digital newspapers, DTH, and digital cable, as well as online music and movie sales, are expected to accelerate industry growth.

Grand View Research writes that new cinema services provide subscribers with access to the most recent international films before they are released in theaters. Amazon (AMZN) Prime, Netflix (NFLX), and Disney+ (DIS) all offer competitive movie streaming services. I do not believe that movie theaters will grow at a 7.2% CAGR in the coming years; rather, I believe that the sector will decline due to competitive threads.

According to a 2014 survey, 57% of Americans would rather stay at home and watch a movie than go to the theater. According to a 2020 survey, only 12% of people would see a movie in a theater first if there was a 90-day wait to see it. In addition, a recent poll from 2021 found that 56% preferred to stream at home, while only 44% preferred to see the same film in a theater.

It’s like the internet versus books in 1999.

EPR’s Balance Sheet Is Strong

According to EPR’s balance sheet, net debt is $2.6 billion, while trailing twelve-month EBITDA is $469 million. The company has enough cash on hand to meet its short-term obligations. According to its annual report for 2021:

As of year-end we had $288.8 million of cash on hand, no borrowings on our $1 billion unsecured revolving credit facility, and no scheduled debt maturities until 2024. Lastly, we were pleased to announce a 10% increase in our monthly dividend to common shareholders for 2022, bringing the annual cash dividend per common share to $3.30.

According to its 2021 annual report, the majority of its debt will mature after 2026. I believe their debt is easily serviceable by their earnings.

Debt maturities (EPR cash flow statements)

Fitch assigned EPR Properties a BBB- rating (outlook stable) on March 22, 2022. Fitch mentioned the following:

The upgrade reflects the company’s commitment to conservative leverage metrics, the recovery in consumer demand for experiential real estate, and Fitch’s expectations that the company will diversify tenant and industry concentration through external activity. Fitch expects the company to sustain metrics appropriate for the rating, including REIT leverage (net debt excluding preferred/recurring operating EBITDA) in the low-to-mid 5x range.

Dividends And Share Repurchases

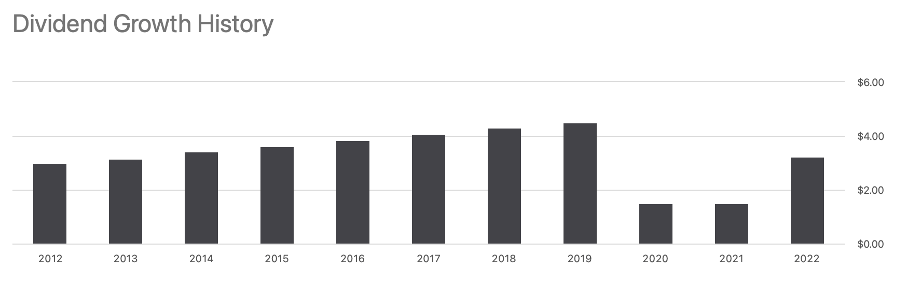

While EPR Properties’ future remains uncertain, the company recently announced a significant increase in its dividend per share. The dividend rate is currently $3.25 per share, with an 8.2% dividend yield. From 2012 to 2019, the annual dividend rate increased by 4.2% on average.

Dividend growth history (Seeking Alpha EPR ticker page)

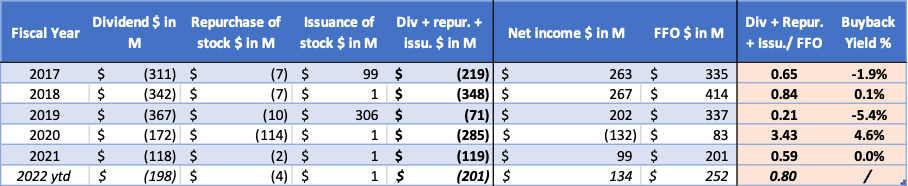

The cash flow statement demonstrates that the company can effectively manage its shareholder return through its funds from operations. While shareholder return was 3.4 times FFO in 2020, it is now at a better ratio of 0.8.

EPR cash flow statement (SEC and author’s own calculations)

Valuation Is Favorable When FFO Is Expected To Maintain

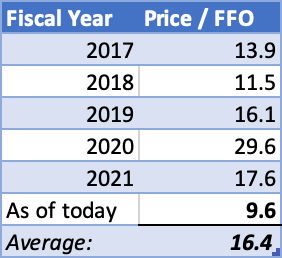

Finally, a word about the company’s stock valuation. The price to funds from operations has historically averaged 16.4. This ratio is currently 9.6, indicating that the company’s stock is significantly undervalued.

Price / FFO (SEC and Author’s own calculations)

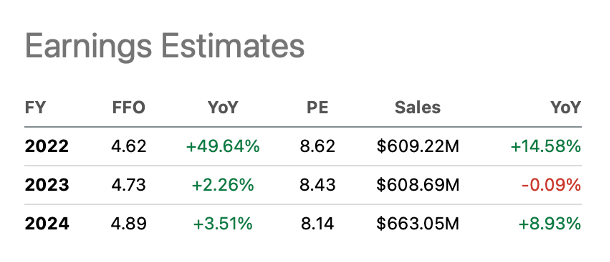

Analysts continue to forecast strong growth in revenue and funds from operations, resulting in a favorable forward price to funds from operations of 8.2 for 2024. This is still too optimistic in my opinion, especially if AMC goes bankrupt.

As I previously stated, I do not believe EPR will be in a position to increase funds from operations for many years to come as AMC appears to be in trouble. In 2019, AMC accounted for 18% of total EPR Properties revenue, with theater revenue accounting for 41% of total revenue.

Earnings Estimates (Seeking Alpha EPR ticker page)

Final Remark

Movie theaters account for 41% of EPR Properties’ total revenue in the third quarter of 2022. While I believe that movie theaters will eventually be phased out due to streaming services, some analysts believe that they will remain operational.

Nonetheless, from a stock valuation standpoint, the stock looks attractive as the dividend yield is currently high at 8.2%. However, if movie theaters are completely phased out, EPR will receive roughly 40% less revenue (and FFO as a simple assumption). Given the risks associated with the entertainment industry, I believe the dividend yield of 8.2% is still on the high side. In that case, the dividend yield is roughly 40% lower (4.92%).

I believe the stock’s valuation remains unappealing, given that investors could soon invest in risk-free assets yielding more than 5%. In a normal scenario, I doubt EPR could significantly increase dividends per share when movie theaters are declining in popularity over time. I don’t see the share price increasing by 50% (for example), resulting in a 5.4% dividend yield. In this high-interest-rate environment, this is simply not logical.

Conclusion

The majority of EPR’s tenants are in the movie theater industry, with AMC Entertainment being the largest. Cineworld, Regal’s parent company, recently filed for Chapter 11 bankruptcy protection in October 2022. Since the Corona crisis, AMC Entertainment has also been in troubled water. There are new rumors of a possible bankruptcy. AMC Entertainment is likely to go bankrupt, and EPR may lose its largest tenant. According to surveys from 2014, 2020, and 2021, many people prefer to watch new movies at home rather than going to the theater. Streaming services like Amazon Prime, Netflix, and Disney+ may pose serious threats to the movie theater industry. It’s like comparing the internet to books in 1999.

Be the first to comment