DNY59

While the “pandemic era” is effectively over, lasting impacts still weigh on many equities. As detailed in “VNQ: Social And Technological Changes Are Making Many REITs Obsolete,” the commercial real estate market faces among the most considerable permanent changes. In my view, many of the negative secular trends facing the REIT market began before 2020 and were triggered by technological and social changes over the past decade. However, lockdown policies, as well as the related recession and inflation, have accelerated the trend.

One specific REIT facing challenges by this wave is the entertainment REIT EPR Properties (NYSE:EPR). Over 41% of EPR’s income is derived from movie theaters, with AMC Entertainment (AMC) being its largest tenant with 15% of its total 2022 sales. AMC has faced a significant decline in sales and chronic negative cash flows over recent years. The company’s cash balance is dwindling rapidly, and it generally appears likely to go bankrupt this year. Of course, that does not mean EPR will lose much of its sales since AMC may remain in business, with its potential bankruptcy likely being a debt restructuring deal instead of liquidation. However, if the theater business is in secular decline and closures occur (which appears likely), EPR may lose some of its sales. Like most REITs, EPR’s profit margins are relatively thin, so a slight loss of sales could significantly upset its cash flow.

More broadly, there is growing evidence that the US is facing a recession this year. In general, entertainment commercial properties are at high-risk since most have not recovered from 2020 losses. While AMC is undoubtedly the most prominent single risk facing EPR, I believe the more considerable risk is the potential decline in the broader sector that EPR is exposed to. EPR’s stock is down significantly over the past year, and its yield is high at ~8%, making it a potential value play for risk-tolerant investors. That said, investors may want to fully assess the probability of EPR going bankrupt if consumer trends continue to deteriorate for a prolonged period.

Risks Facing EPR’s Core Business

EPR’s commercial property portfolio does not fit into a traditional segment. Both the retail and lodging segments, which it is associated with, have been under great strain in recent years. As detailed in CBRE’s recent 2023 market outlook, those two segments carry the most significant economic risks today, with many lower-quality properties in distress. The important caveat is that high-quality resort hotels, retail venues, and similar are seeing above-trend growth. While large department stores and cheap hotels are suffering, many more people are flocking to higher-quality properties.

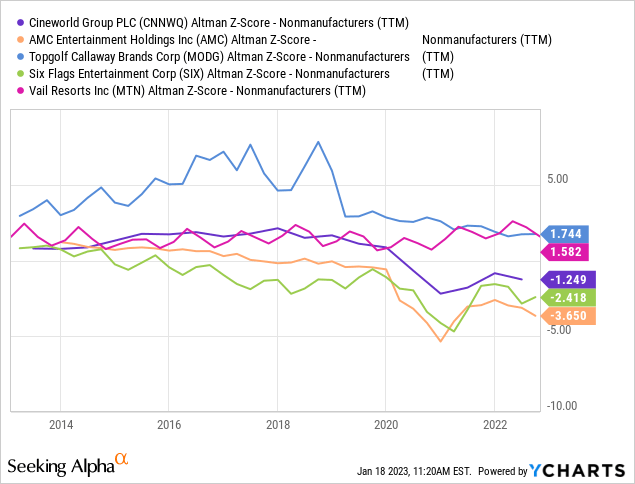

In general, this trend may bode well for EPR properties. As people find more entertainment avenues at home, they demand higher-quality venues. For example, many theaters, including AMC, are shifting toward “dine-in” experiences, where customers are generally expected to spend more money. While EPR’s tenants may be more robust than their general peer group, they are still relatively high-risk enterprises. For example, AMC, Regal (via Cineworld – recently bankrupt), and Topgolf (via Callaway Brands) (MODG) make up collectively around 42% of EPR’s total sales (annual report pg. 14), so their success is vital for EPR. Additional public tenants include Six Flags (SIX) and Vail Resorts (MTN). All five of these companies have experienced tremendous increases in bankruptcy risk, using the Altman Z-score metric, over the past five years. See below:

Altman Z-scores below 1.8X indicate higher bankruptcy risk, with levels below zero indicating high immediate bankruptcy risk. Of these, Cineworld is already in bankruptcy, while AMC and Six Flags are at increased risk. Vail and Topgolf are more robust, but their balance sheets and financial trends indicate higher risk exposure. All five of these companies have seen their sales rise back to normal since 2020, but only Topgolf and Vail have made full revenue recoveries. Of course, the Altman Z-score does not account for the fact that these firms suffered significant declines in 2020 due to government mandates that created immense short-term negative impacts on their businesses.

In my view, EPR’s most significant economic risk may not be that people stop going to its entertainment properties but that its tenants cannot increase sales at the same pace as expenses. Importantly, with wages (particularly in lower-pay service jobs) and other operating costs rising quickly, this segment’s business should see revenue rise ~20%+ since 2019 to see the same bottom-line profits. Essentially all “Experiential” companies (theaters, resorts, casinos, restaurants, etc.) generally require large labor forces of near-minimum-wage part-time workers. By far, the most significant labor shortages are seen in lower-wage jobs. I believe the inverted US population pyramid ultimately drives this trend; since there are comparatively fewer 15-26-year-olds than in decades past, there are not enough people willing to fill low-paying service jobs, and they will never be for decades to come. I believe that fact is essential for EPR since the (demographic) worker shortage trend creates margin strain for virtually all tenants.

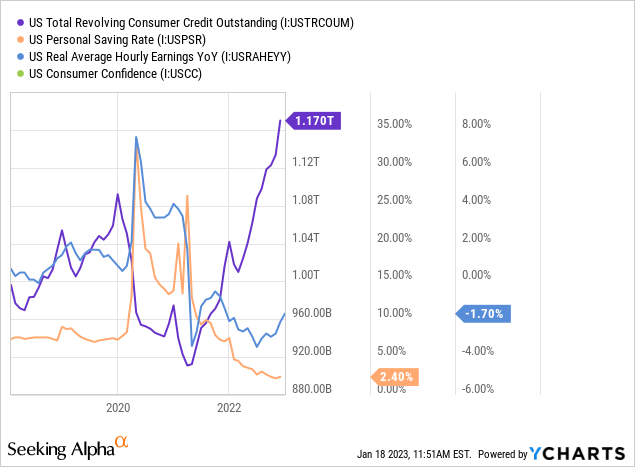

Of course, with the economy seemingly entering another recession, many of EPR’s tenants are at high risk of experiencing revenue declines. Over the past two years, strong “rebound sales” for high-quality resorts and retail venues have been strong, supporting EPR’s safety. However, all of EPR’s tenants sell “luxury” experiences that can easily be avoided if people cannot afford them. Today, personal savings levels are very low amid falling real incomes. This trend has led to low consumer sentiment and immense credit card debt growth. See below:

Revolving consumer debt is rising exceptionally quickly today as people offset falling incomes and low savings with more borrowings. In the short-run, this trend supports EPR’s tenants since people continue spending money despite strain. However, credit card debt can only rise so quickly before people are forced to rein in spending. In my view, if there is a recessionary rise in unemployment this year, it is virtually inevitable that discretionary spending will collapse as credit card debt caps are reached.

Overall, I believe it is clear that EPR’s tenants face significant risk in 2023 and beyond. Many have indeed seen sales recover, but many have not made full recoveries, and virtually all have seen costs grow disproportionately amid labor shortages. Further, it appears very likely that spending on “experiential” experiences will fall this year and may remain low amid persistent economic strains on households. Thus far, these strains have been masked by rising credit card debt, but debt can only replace income for so long, so there may be a sudden drop-off in non-essential consumer spending early this year.

How Will EPR Be Impacted?

In my view, there is a very high probability that most of EPR’s tenants will see a greater strain in 2023 than they did in 2022. There is also a seemingly high probability that AMC, and perhaps other EPR tenants, will experience chapter 11 bankruptcy this year. However, while these are negative factors for EPR, EPR trades at a nearly 50% discount from its pre-pandemic price. The REIT’s “P/FFO” is also around 40% below the REIT sector median at 9X, while its debt to capital is just 11% higher.

The critical question is not whether or not EPR faces business risks; it would be foolish to state otherwise given the evidence; it is whether or not EPR is sufficiently discounted to offset those risks. We must consider how much EPR’s sales may decline from these risk factors to determine this. Secondly, we must consider how these trends may impact the long-term valuations of the commercial assets EPR owns.

Over the past twelve months, EPR generated around $475M in net operating income (operating income plus depreciation). In 2019, the company generated an NOI of $512M, falling to $290M in 2020. At its TTM NOI and an estimated “fair” capitalization rate of 8% (based on early 2022 metrics), its properties are estimated to be worth a total of ~$5.94B ($475M/8%). Last quarter, the company had around $705M in tangible non-real estate assets and $3.22B in total liabilities. Combined, these figures place my base equity value estimate for EPR at ~$3.4B. After subtracting ~$300M in preferred equity (based on the combined market value of its E, C, and G series shares), EPR estimated common equity value is ~$3.1B. The stock’s market capitalization is currently $3.06B, trading close to its estimated NAV.

If we assume no changes in commercial real estate market activity nor EPR’s net operating income, then the stock appears to be very near or slightly below its estimated fair value. That said, it is likely so close to its fair value that it is not likely a long opportunity. While the stock was much higher in 2018/2019, its NOI was stronger, capitalization rates were lower, and its debt was lower. The stock may have also been overvalued at that time. Thus, I do not believe EPR is a solid short opportunity, as some analysts predict.

If we change our assumptions, estimating either a 10-20% decline in EPR’s long-term NOI or a ~1-2% increase in “fair” capitalization rates for its properties, EPR would easily be overvalued today. Considering EPR’s NOI fell ~40% below TTM levels in 2020, I do not believe a lasting 10-20% decline is unlikely, particularly considering economic trends. Additionally, given the rise in mortgage rates and risks in specific real estate segments, a rise in the “fair” capitalization rates of EPR’s assets to 9-10% does not seem unlikely.

Assuming the capitalization rate of EPR’s assets rises to 9% and its NOI declines to $430M (~10% below TTM levels), the estimated “fair value” of its properties would be around $4.77B (430/9%). Adding EPR’s ~$705M in other tangible assets and subtracting $3.54B in liabilities and preferred equity, the company’s estimated fair equity value would be $1.94B. That translates to a share price target of $25.4, ~46% below its current level. Crucially, with EPR’s higher debt level and more volatile NOI, a slight change in its conditions could dramatically hamper the value of its equity.

The Bottom Line

There is no substantial evidence today that EPR will face bankruptcy or existential risk this year. Many of EPR’s tenants are under strain, some of which are pandemic related and likely ending. However, many companies in EPR’s portfolio began to experience tension around 2018, potentially due to rising labor costs (and the associated shortage). EPR’s properties are of higher quality and seemingly less likely to experience “technology-induced obsolescence,” but cyclical recession risks loom large, and many are still struggling with sales declines. In my view, these trends will likely negatively impact EPR’s NOI or the value of its assets (cap rate increase), likely harming EPR’s equity value.

Based on my NAV estimates, I believe EPR’s fair value per share is likely within the $25-$40 range. Since the stock is on the high end of that range today, I do not believe it’s a long opportunity. Further, because I have a bearish bias on the economy and think some of EPR’s tenants will face bankruptcy, I am slightly bearish on EPR and believe it will likely decline over the coming months.

Be the first to comment