The Indian Flag flying high on top of a flag pole paresh3d/iStock via Getty Images

Introduction

Recently, I shared why I believe oil prices are set to go down and how this leads to investment idea themes such as bullishness on oil importers such as India. One instrument to play the theme is via the WisdomTree India Earnings ETF (NYSEARCA:EPI). My analysis reveals absolute upside on EPI, although a relative read of the technicals does not give clear signs of alpha potential vs the S&P 500 Index (SP500).

EPI ETF Exposure Mix

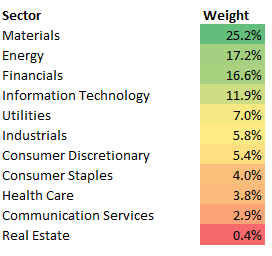

Sector Mix

EPI ETF Sector Exposure (EPI ETF Website, Author’s Analysis)

EPI is an asset-heavy exchange-traded fund (“ETF”) with materials, energy, and financials making up 59% of the overall weight. These top 3 sectors are also quite cyclical in nature, giving EPI strong indexation to business cycles.

FactSet and Refinitiv Lipper data suggests that roughly 25% of the overall exposure is tied to export revenues. Information Technology (IT) businesses in this index includes companies such as Infosys, TCS, HCL Technologies.

I have covered the Indian market for many years, and I think I know the nuances well. Based on my industry experience, Indian IT companies are mostly export oriented; they utilize cheaper Indian labor to provide technology services to global markets such as the United States, which makes up roughly 70% of revenues in the sector. I also know that roughly half of the revenues generated by the metals sector – Tata Steel, JSW Steel, Hindalco, Vedanta and Jindal Steel – would be driven by exports.

Thus, as a crude estimate, I can estimate that almost all of the information technology exposure and almost half of the total materials exposure would be driven by export revenues. That amounts to roughly 25%.

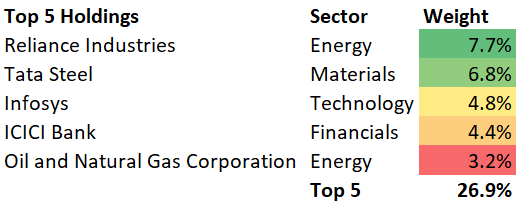

Top 5 Holdings Mix

EPI ETF Top 5 Holdings (EPI ETF Website, Author’s Analysis)

EPI’s top 5 holdings include Reliance Industries, Tata Steel (OTC:TATLY) Infosys Ltd (INFY), ICICI Bank Ltd (IBN), and Oil & Natural Gas Corp Ltd.

2 counterbalancing points driving EPI

- A slowing global economy is a headwind for EPI’s export revenues

- EPI benefits from domestic credit growth, construction activity uptick and capex expansion.

A slowing global economy is a headwind for EPI’s export revenues

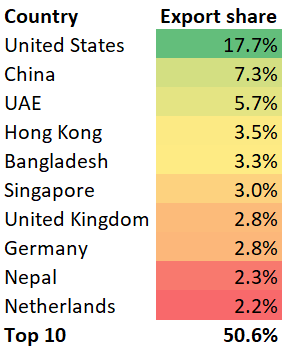

As noted before, roughly 25% of the Indian stock market and EPI’s exposure is linked to exports. According to India government filings, the top 3 export destinations for India include the United States, China and the UAE, which collectively make up 30.7% of total exports:

India export mix (India Department of Commerce, Author’s Analysis)

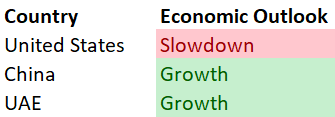

Thus, the economic growth of these key countries are important drivers of EPI’s 25% export mix. This table below summarizes my outlook on the US, China (MCHI), and the UAE (UAE) based on my previous analysis:

Economic Outlook Assessment (Author’s Analysis)

Overall there is an overall 17.7% indexation to the slowing economy of the United States, offset only partially by a 13.0% exposure to my growth outlook on China the UAE. Hence, I believe EPI’s ~25% export exposure is a net headwind for the ETF’s performance.

EPI benefits from domestic credit growth, construction activity uptick and capex expansion

India posted strong credit (loan) growth of 13% in November 2022, driven by a 19.6% boost to credit to the micro, small and medium enterprises (MSME) sector. This is significant because MSMEs make up almost a third of India’s gross value added (GVA).

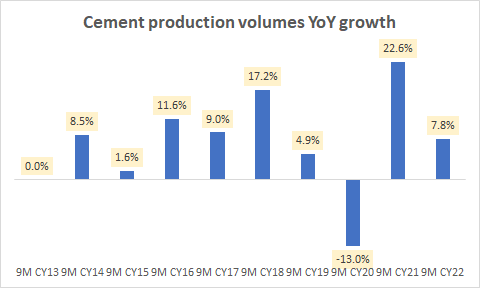

There are signs strong construction activity in the country too, supporting the domestic materials industry, where EPI has the highest weight. For instance, 9-month cement volumes are growing at a 7.8% YoY rate, which corresponds to a strong 2-year CAGR of 15%:

India cement production volumes YoY growth (Company Filings, Author’s Analysis)

To complement this, earnings call commentary of key companies suggests a buoyant capex outlook:

Construction activities has restarted, and [the] consumer durable market is vibrant now.

– Q2 FY23 earnings call of Hindalco (OTCPK:HNDNF), which has a 2.5% weight in EPI.

…we have seen a robust order inflow again in all the segments…

– Q2 FY23 earnings call of engineering services conglomerate Larsen & Toubro (OTC:LTOUF), which has a 1.4% weight in EPI.

…order inflows from commercial buildings, factories, data center and infrastructure such as metro railway, water distribution and power distribution sectors picked up…

– Q2 FY23 earnings call of electro-mechanical products company BlueStar.

The mix of healthy credit growth, momentum in construction activity and an upbeat outlook on capex spends make me bullish on the domestic drivers of EPI.

Valuation

Comparing the Indian market ETF EPI with a broader emerging markets ETF such as the iShares Core MSCI Emerging Markets ETF (IEMG):

EPI Valuation vs Emerging Markets ETF (Company Filings, EPI ETF Holdings, IEMG ETF Holdings)

I note that although EPI is trading at a 2.8% premium to IEMG on a market-cap weighted P/B basis, it is trading a meaningful discount of 26.4% on a market-cap weighted P/CF multiple basis.

I believe cash flow based valuations, when done right, capture economic realities better. Hence, I am inclined to believe that EPI is still trading at a discount relative to other emerging market ETFs.

Technical Analysis

If this is your first time reading a Hunting Alpha article using technical analysis, you may want to read this post, which explains how and why I read the charts the way I do, utilizing the principles of Flow, Location, and Trap.

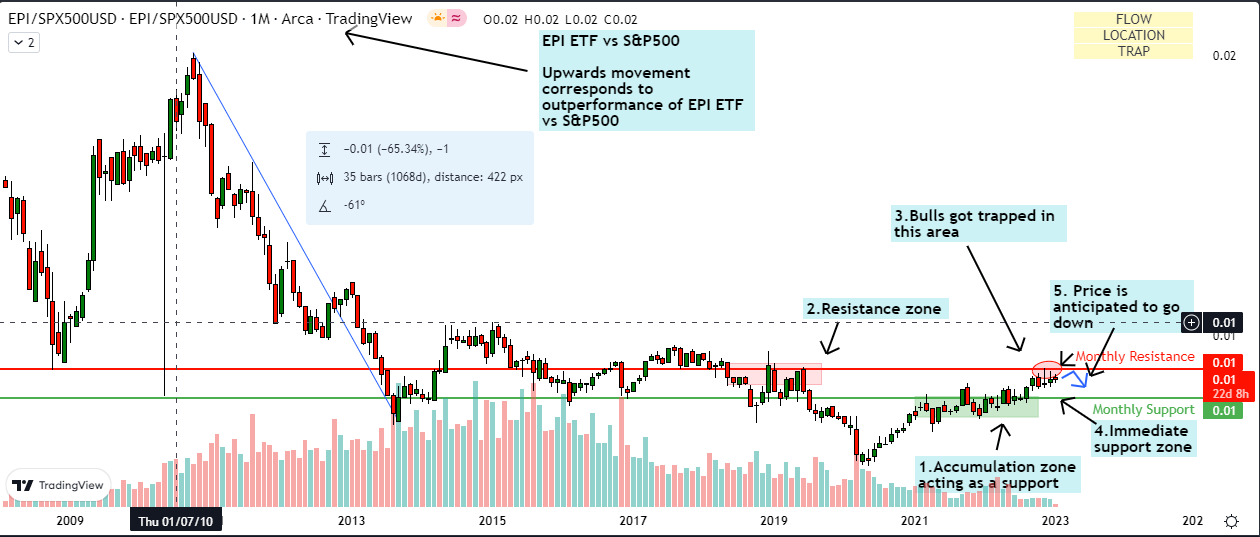

Relative Read of EPI vs S&P500

EPI vs SPX500 Technical Analysis (TradingView, Author’s Analysis)

The relative chart of EPI/SPX500 above shows the price facing resistance from a supply zone created in 2019. There is a possibility of a bull trap in this region and I anticipate a downward movement from this level. I believe the accumulation zone created in 2021-22 will act as a key support zone to halt a further decline.

Standalone Read of EPI

EPI Technical Analysis (TradingView, Author’s Analysis)

On a standalone basis, I am anticipating a bullish move for EPI toward the $36 key resistance area zone. I expect the $29 monthly support zone to hold as there has been a sharp buyer reaction from this level.

Summary

EPI may be dragged down by a weak US-focused export environment, but the majority of the exposure is toward domestic Indian activity, where credit growth, construction activity and the capex outlook is looking robust. Furthermore, EPI is trading at a discount to other emerging market ETFs such as IEMG on a cash-flow valuation multiple basis.

On the technicals side, I see absolute upside in WisdomTree India Earnings ETF, but I am less certain on whether it will outperform the S&P500. All in all, I rate WisdomTree India Earnings ETF a buy, although I personally will not be buying at this stage as I am not confident on alpha generation potential just yet.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment