Petmal/iStock via Getty Images

Introduction

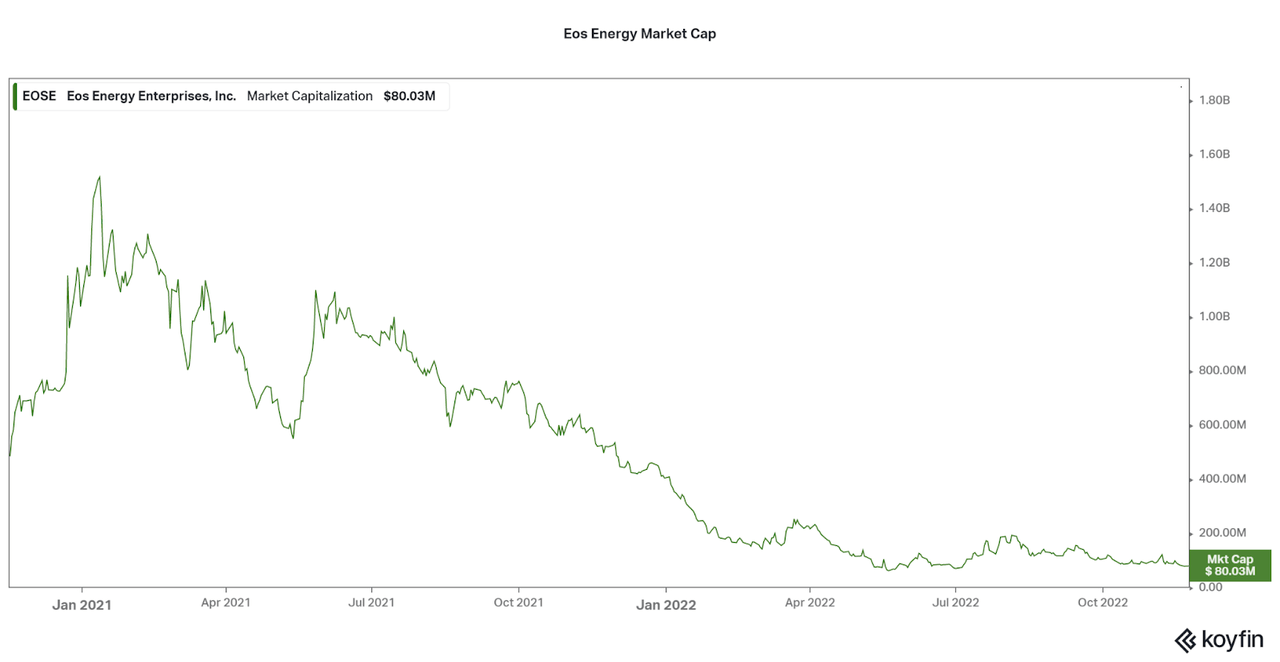

I have covered Zinc-ion grid-scale energy storage battery producer Eos Energy (NASDAQ:EOSE) twice before, and both times I was skeptical. A year or so ago, the issue was the high valuation and limited revenues. Then, liquidity risk as operational losses ate away at all cash on hand. Now, the company is wringing out all the financing they can to establish enough revenues to become viable. Due to the risks, the company is now trading around $1.00 per share, or a $80 million market cap.

While accepting the continued risk profile, I believe there are a few positive indicators that support a viable investment beginning at this low level. However, the bet continues to be speculative so investors must take precaution. This article will focus on the few new details that have arisen and revisit the opportunity. If you would like to learn more about Eos Energy’s financial issues and battery platform, please read my prior coverage, here (liquidity issues) and here (fair value estimates).

Hanging On Despite Risks

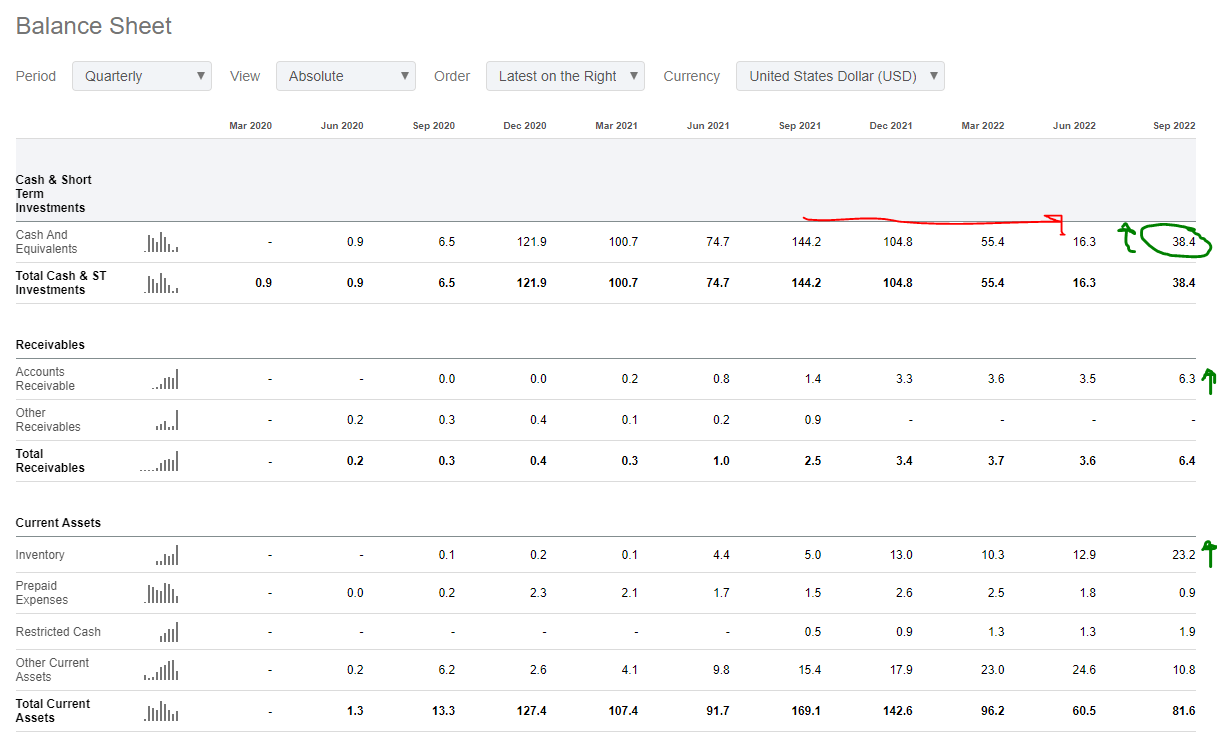

Eos’ cash balance has had a roller coaster ride over the past three years. From less than a million bucks in 2020, the IPO during a highly-stimulated economy allowed cash to reach over $120 million. However, operating losses caused cash on hand to fall rapidly each quarter. By the report of Jan 2021, cash had fallen back to $75 million. Then, Koch provided a much needed $100 million investment that boosted cash back to almost $150 million. Despite this, cash on hand fell to $16 million just a year later in June 2022.

The liquidity scare of 2022 helped bring the market cap down from highs of over $1.5 billion all the way down to $80 million in about two years. While investors are certainly hurting if they got in early, the company was able to gain plenty of publicity and capital to invest in operations. The problem is that the operations are expensive and the company is often pushing their capital to the limit. Lack of transparency and a cloudy capital raising outlook is certainly a major reason for the sell off. Higher interest rates, economic woes, and supply chain issues certainly don’t help.

Koyfin

Some Positive Financial Indicators

Thankfully, there are a few details investors can look at that increase the probability of success despite the lack of funds. First, the company has established a credit line and this has allowed cash to move positively as of the last quarter. This is off the back of the swift decline in cash on hand from $150 million to $16 million.

While current losses remain high, the close to $1 billion operational spend over the past two-three years may be reigned in soon as customer revenues pick up the slack. This can be seen in rising accounts receivable and inventory levels that have risen as of the last quarter. If the trend holds, then I feel comfortable that revenues coming in can offset the lack of liquidity, at least for the time being.

Seeking Alpha

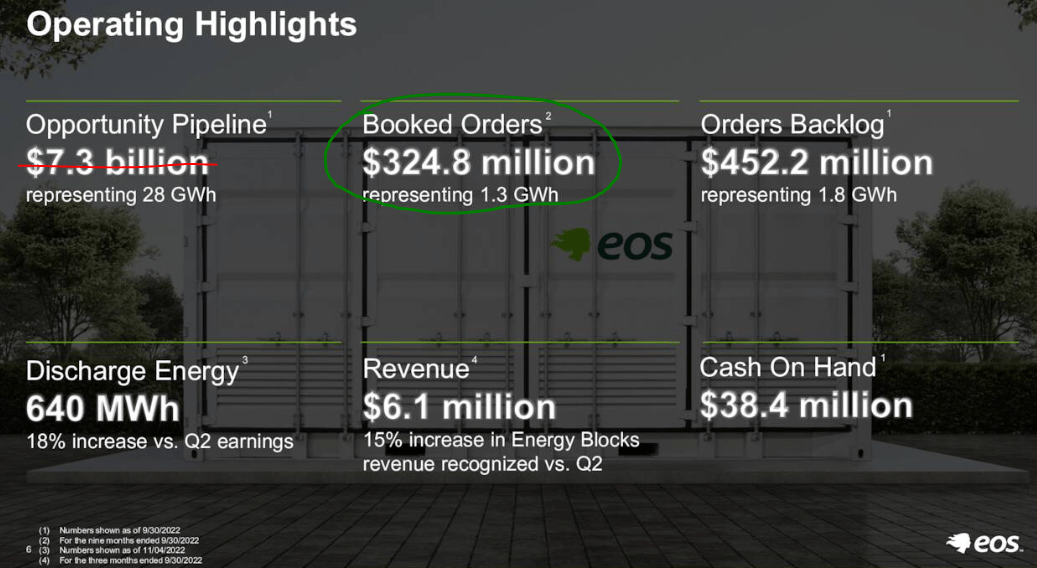

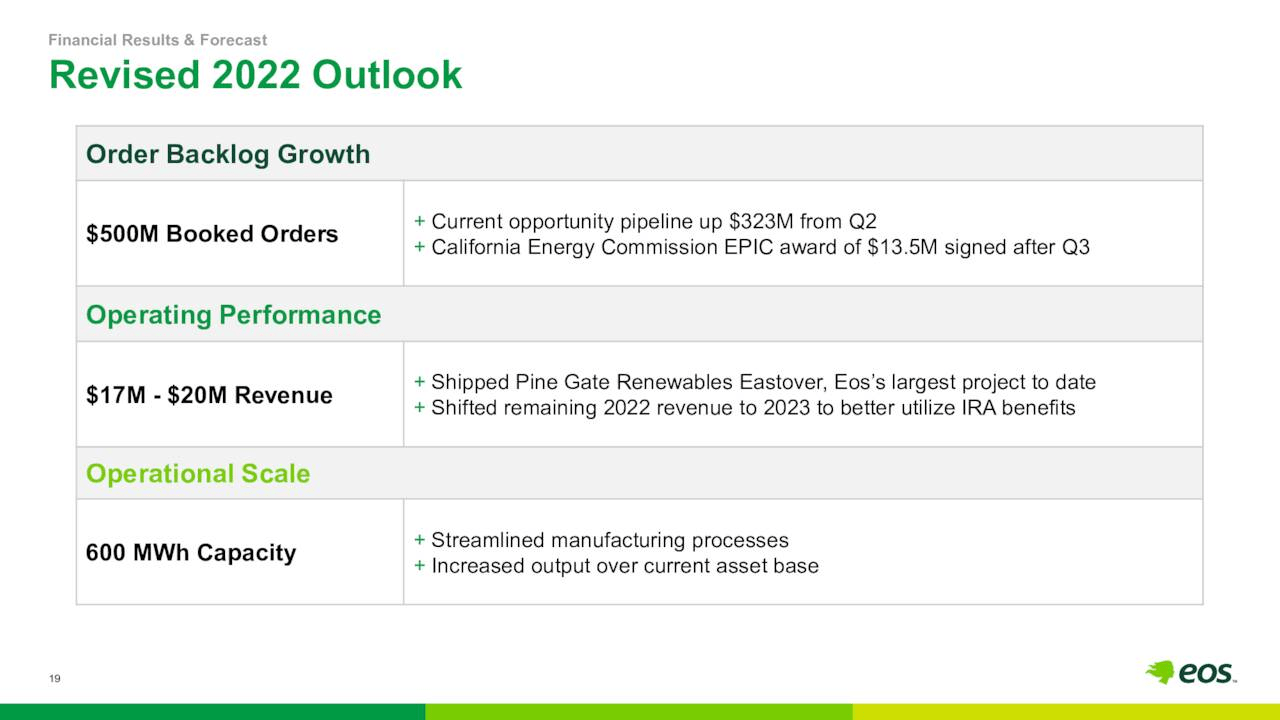

The total amount of revenues the company can earn based on guaranteed contracts is likely around $300 million as highlighted by the company’s booked orders data. However, the timeline for realizing these revenues could be beyond a year. The $450 million backlog and $7 billion pipeline are fickle and not guaranteed, so investors are not pricing in the long-term opportunity at the moment. The focus is on what can be earned on a quarterly basis.

While the inventory and accounts data is positive, there is still plenty of risk inherent in the investment. The current balancing act is the rate of revenue growth along with changes to the cash on hand each quarter. Also, due to finalization of IRA law and regulations, the current contracted orders may continue to be postponed until after the next few quarters. While I believe the IRA will be generally stimulative for the energy storage industry, the short-term hesitation as the law unfolds does not help Eos.

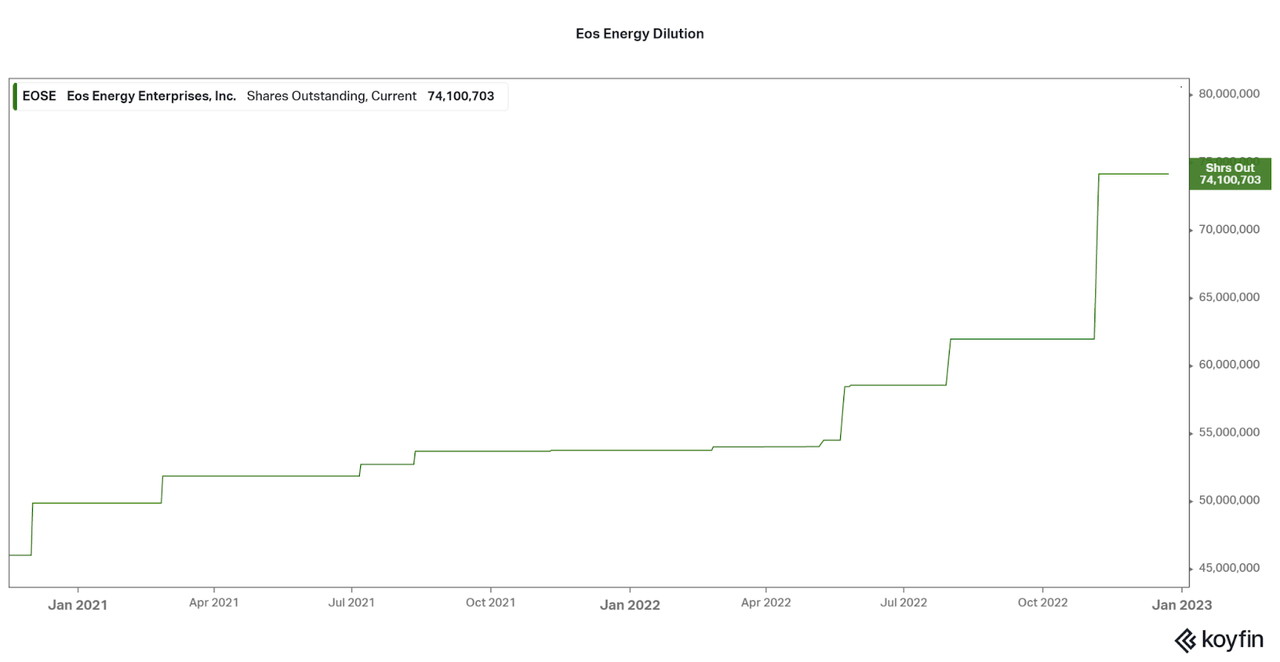

While debt has been raised the past few quarters thanks to investors and private equity, the amount available to tap is drying up. As per SEC filings, the amount of capital provided by Eos’ main credit line gets smaller each time they file for funds. In fact, the last raise was only or $5 million, far from the $200 million in net income loss Eos had over the past twelve months. As such, dilution is the crux of every investor at the moment. Can any investor tolerate a 26% annualized increase in shares outstanding? Especially when newly listed shares are worth far less than just a year ago. Well, investors getting in now will likely face a little less dilution than those over the past two years, but more is sure to come.

Eos Investor Presentation Koyfin

Outlook And Expectations

That brings us to the current outlook. Will current managerial expectations of revenue growth be enough to satiate the high cost of operations? First of all, due to the wording of the IRA, many renewable projects have been pushed to 2023 for tax purposes. This reduces revenues for the last quarter of the year. I expect that investors have priced this into a degree, but poor results may cause a drop. However, these projects may be reflected in accounts payable and/or inventory data, adding to the transparency of the year to come. The current expected booked orders data for $500 million certainly is positive, but we need some of that to come in Q4.

The problem is that management has not discussed earnings for the last quarter, and so the question of liquidity remains for now. Will the losses for next quarter remain above the ~$25 million per quarter level? Current cash on hand of $34 million barely covers that amount, but the next quarter will be hanging on by a thread-hence more dilution may be possible. However, some issues with supply chain, operational capex, and R&D costs may be resolved. In fact, management has already discussed this was the case for high costs last quarter, but some improvements may improve profitability for the last quarter of the year:

Yeah, so Chris, with regards to the cost-of-goods sold, so you know I think the breakdown of the increase was volume and then an inefficiency aspect of the challenging environment we faced in Q3. And so, you know I would say that you know of the – you know I think it was $9 million increase as a result of the inefficiencies.

So you know we also talked about other big cost reduction aspects. You know not just the automation cycle time, etc., but with regards to alternative materials. And so going from titanium to conductive polymer, so all those factors are you know what lead to the much reduced cost profile and being able to reduce the cost by 50% at launch from where we are now on the Gen 2.3.

Eos Investor Presentation

Conclusion

So, as we revisit the current narrative for Eos, the question is whether the doubts, debt, and dilution issues of the past remain. While doubts are beginning to be resolved, debt and dilution remain. However, debt and dilution are the reasons why the company can succeed through the tough transition to commercialization. There are always difficulties when crossing the valley of death. Thankfully, the company has lasted this long despite the liquidity risks and I believe they are now turning the quarter. Now that the share price has fallen 70% from my first article, and have held up flat since my second article, I believe the time to begin accumulating is here (around $1.10-15). For risk tolerant investors of course.

There are plenty of fully mature, profitable companies within the realm of sustainable technologies there are plenty of ways to gain exposure to the industry (and I cover many of them). However, to be on the leading edge, one must take risks. Therefore, I have now begun to allocate a small portion of my portfolio to an investment in Eos, despite my neutral or bearish commentary in the past. As many commented on prior articles, if Eos are successful, then the opportunity is immense.

While I believe we may have to wait a few quarters before we can be more confident about the long-term opportunity, I do feel the probability of success is skewed more positive at this time, and market cap. Also, don’t forget that a DOE loan is still on the table and may arrive soon and will be an incredibly positive catalyst.

For those interested in the investment, I would recommend adding on a recurring basis to reduce the risk of short-term volatility, particularly between now and the next earnings. If the next quarter is positive and causes the share price to increase rapidly, I would hold off from adding more. Although, if the next quarter is negative (liquidity scare, low revenues, high losses, etc) and the share price falls, I would continue to add at the lower prices.

I would abandon my bullish stance under two particular scenarios. First, if the valuation rises too fast, too soon. At that point, I’d suggest investors enjoy the short-term trade and take profits. Return back to my first article on fair value estimations for price points that I feel may be supported. Then, if the liquidity issues remain, such as if the DOE loan does not arrive or losses remain excessive, then I believe the company will be unlikely to perform well at any point in the future. Remember, debt and dilution will continue and the total upside potential will continue to shrink, particularly if cash on hand falls below $25 million (unless supported by increased revenues/receivables/inventory).

As always, I will revise my thesis based on the data at hand. Let us hope Eos has the luck and ability to succeed in developing their sustainable technology.

Thanks for reading. Feel free to leave a comment below.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment