Darren415

Introduction

I’ve written two bullish articles about re-commerce retailer Envela Corporation (NYSE:ELA), the latest of which was in October when I said that the challenging macroeconomic environment was boosting demand for refurbished electronics.

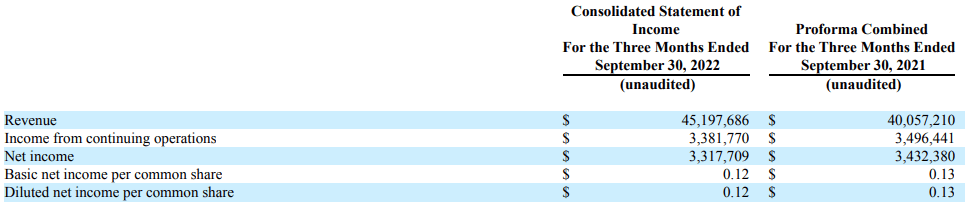

It seems that there are strong headwinds for the company as it booked EBITDA of $4.1 million in Q3 2022, which represents an increase of just over 42% year on year. Sales, in turn, rose by almost 20% but I’m concerned that the reason behind this includes the opening of a new store as well as inorganic growth. In addition, I have concerns about growth in the future and the inventory levels of the electronics business remain low. This is why I continue to rate Envela as a speculative buy. Let’s review.

Overview of the Q3 2022 financials

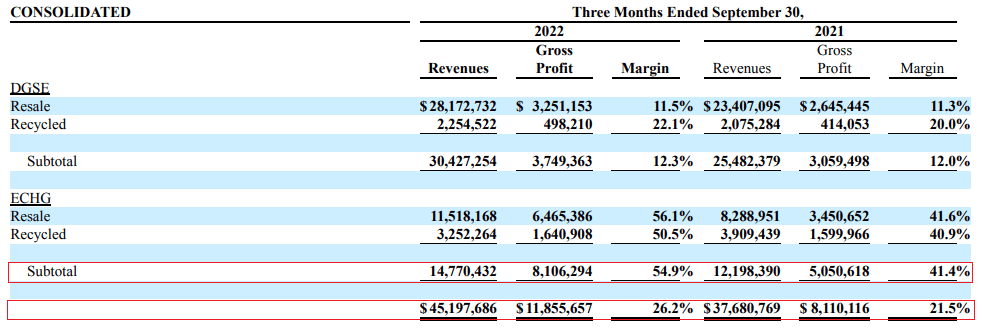

In case you haven’t read any of my previous articles about Envela, here’s a short description of the business. The company is involved in the purchase and sale of jewelry and bullion products to individual consumers, dealers, and institutions through DGSE, whose brands include Dallas Gold & Silver Exchange, Charleston Gold & Diamond Exchange, and Bullion Express. This segment operates a total of 7 jewelry and bullion stores in Texas and South Carolina and Envela used to be named DGSE Companies until December 2019. The company was struggling to stay profitable a few years ago and it changed its name to Envela to reflect the $6.9 million purchase of Echo Environmental and ITAD USA to form a new operating segment named ECHG focused on processing, recycling and reselling electronic waste. Echo Environmental and ITAD USA were owned by John Loftus, who’s been Envela’s Chairman and CEO since 2016. ECHG focuses on the purchase and recycling or refurbishment of consumer electronics and IT equipment and its main source of inventory is school districts and its creation marked the beginning of a turnaround for Envela as its margins have overshadowed DGSE over the past several years. Turning out attention to the Q3 2022 financial results, we can see that while most of the revenue growth is coming from DGSE, ECHG accounts for the vast majority of the gross profit growth.

Envela

The revenues of DGSE increased mainly due to the opening of an additional retail store and I find it disappointing that the economies of scale seem inconsequential. The increase of ECHG’s revenues, in turn, can be attributed to the acquisition of IT asset disposition services provider Avail in October 2021. Looking at the pro-forma results, this company had sales of $2.4 million in Q3 2021.

Envela

Back in October, I was optimistic that high inflation rates and constrained consumer spending were having a positive effect on demand for refurbished electronics but it seems that ECHG has a low organic growth rate at the moment. According to Envela’s Q3 2022 financial report, expected capital expenditures over the next 12 months are just $1.5 million (see page 37 here) and I’m concerned that the revenue growth rate could decline significantly due to the lack of acquisitions or new jewelry and bullion store openings. Envela claims that many of its clients have made commitments of going carbon neutral over the next few years (page 30). While this could potentially further expand key relationships, but it’s impossible to tell what impact it could have on revenues. Also, there is no timeline given. In my view, relying on this sales growth factor could be dangerous. However, I’m pleasantly surprised that ECHG’s margins improved in Q3 2022 considering the reason behind this doesn’t seem to be Avail as the latter was unprofitable a year earlier. According to Envela, the ECHG has been benefiting from an improved product mix with higher pricing power (page 33).

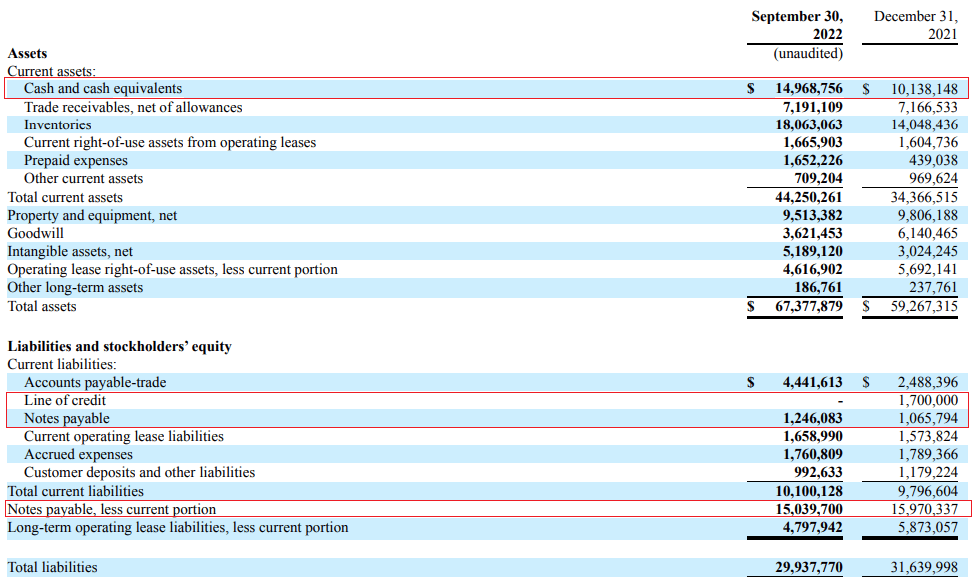

Turning our attention to the balance sheet, I think the situation looks good as $7.7 million of net cash provided by operations during the first 9 months of 2022 allowed the company to finish September with almost $15 million in cash and cash equivalents. Net debt is down to just $1.3 million and Envela has an enterprise value of only $142.9 million as of the time of writing.

Envela

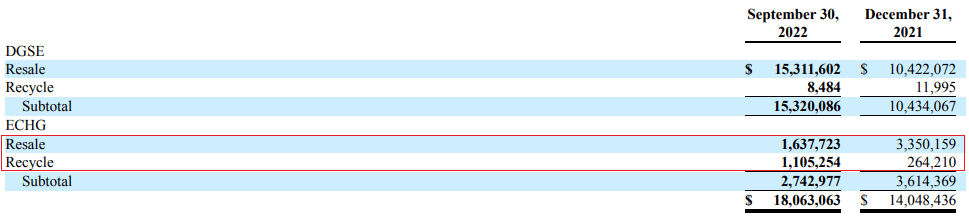

The company has an asset-light business model and its EV/EBITDA on an annualized basis is 8.7x which I consider low but I’m concerned that inventory levels at ECHG are at alarming levels. As of September, the inventories of this segment stood at just $2.7 million. Although this represents an improvement from the $1.8 million level from June, I’m concerned that any unforeseen issues with securing electronics for resale could lead to a significant decrease of profitability.

Envela

Looking at other risks for the bull case, I continue to be concerned that Envela doesn’t seem to have a discernible moat which means that the margins of ECHG could compress significantly if competition in the sector increases in the future.

Investor takeaway

Envela booked strong financial results for Q3 2022 and is trading below 9x EV/EBITDA on an annualized basis. However, I’m concerned that the opening of a new store by DGSE barely moved margins while almost all of the revenue growth at ECHG came from the purchase of Avail. The margins of ECHG rose thanks to an improved product mix but it’s unclear if this can be sustained in Q4 2022.

Overall, I think that Envela is cheap but low planned CAPEX suggests that revenue growth could slow significantly and there are several things that can go wrong, with the lack of sufficient levels of inventory perhaps being the most serious one. In my view, it could be best for risk-averse investors to avoid this stock.

Be the first to comment