Sakorn Sukkasemsakorn

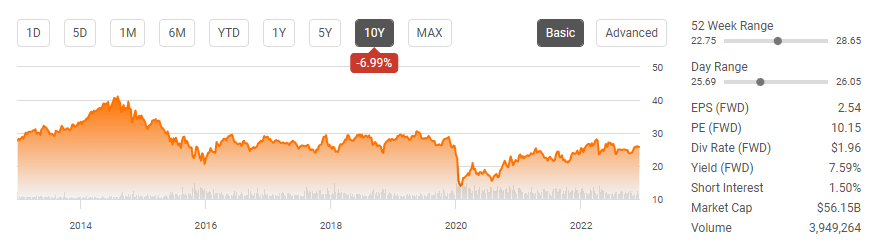

If I had to speculate, I would assume that Enterprise Products Partners (NYSE:EPD) attracts more income investors than those seeking capital appreciation. While I believe energy infrastructure companies are undervalued, especially midstream operators, the large reliable distribution has been the focal point for EPD. Over the past decade, EPD has declined by -6.99% and more recently declined by -3.37% over the previous 5 years. EPD’s chart is nothing exciting, but the forward distribution yield of 7.59% is. Income investors like myself love a company that will just trade sideways and generates a large consistent yield that can be compounded into much larger distributions. In 2023 EPD will deliver its 25th consecutive year of distributions increases and deliver a significant financial milestone. Dividend Aristocrat status is the pinnacle of dividend investing as it symbolizes a company’s financial stability and ability to plan to allocate capital back to shareholders years in advance. EPD is not a member of the S&P 500, so it won’t officially become a Dividend Aristocrat, but its track record cannot be discounted, and in 2023 EPD will become an unofficial member of this prestigious group. From an income investor perspective, EPD is delivering across the board and should continue generating larger annual distributions for years to come.

Seeking Alpha

EPD’s distribution is hard to replicate and should be at the top of every income investors list

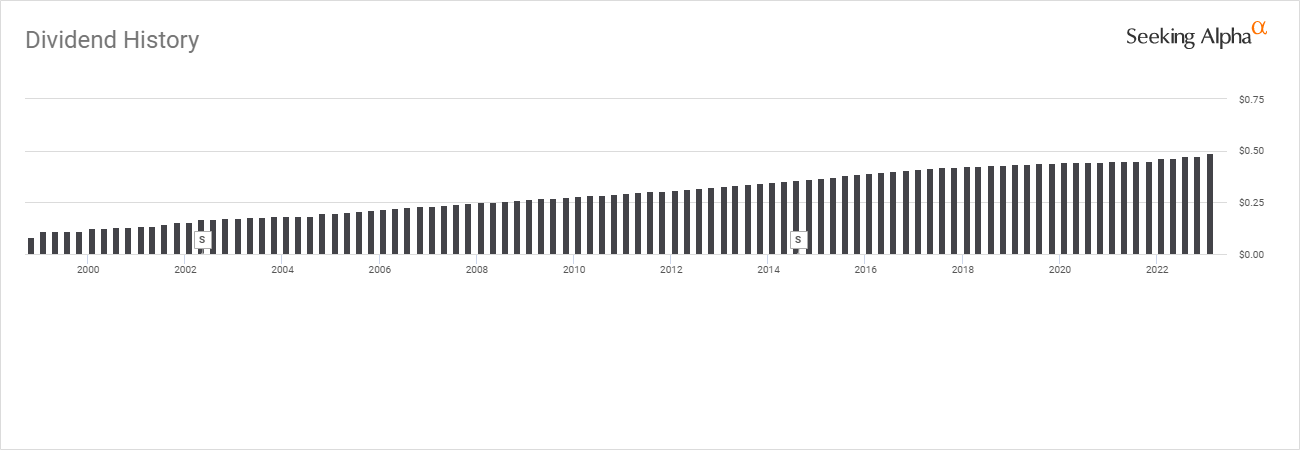

Is there anything to dislike regarding EPD’s distribution? I can’t find a single negative attribute. EPD declared a $0.49 distribution in Q4 2022, which was a 5.4% YoY increase. This marked the 24th year of consecutive distribution increases, and EPD has also provided investors with quarterly increases to amplify the powers of compounding. On the Q4 2022 conference call, Randy Fowler (EPD Co-Chief Executive Officer) indicated that EPD would evaluate its next distribution midyear 2023. In 2022, EPD paid approximately $4 billion in distributions. When the total return of capital, which includes unit repurchases, is accounted for, EPD’s payout ratio of adjusted cash flow from operations was 54%, and the payout ratio from adjusted free cash flow was 71%.

In 2022, EPD generated $9.3 billion in Adjusted EBITDA and $7.75 billion of Distributable Cash Flow (DCF). The Adjusted EBITDA placed EPD’s leverage ratio at 2.9 times on a net basis after adjusting debt for the partial equity treatment of its hybrid debt and also reducing by the partnership’s unrestricted cash on hand. In recent years, EPD had slowed its distribution growth to focus on its financial leverage, and over the past 18 months, EPD has brought its distribution growth back up to the 5% range.

EPD is returning 51.61% of its DCF to unitholders through the distribution ($4B / $7.75B). EPD currently pays an annualized distribution of $1.96 per unit. At an average annualized distribution increase of 5%, EPD’s annual distribution would increase to $2.06 in 2024, $2.16 in 2025, $2.27 in 2026, $2.38 in 2027, and $2.50 in 2028. This would be an overall distribution increase of 27.63% over the next 5 years. Hypothetically, if EPD continued trading sideways and remained around $26 in 2028, the distribution yield from a $2.50 annualized distribution would be 9.62%.

Seeking Alpha

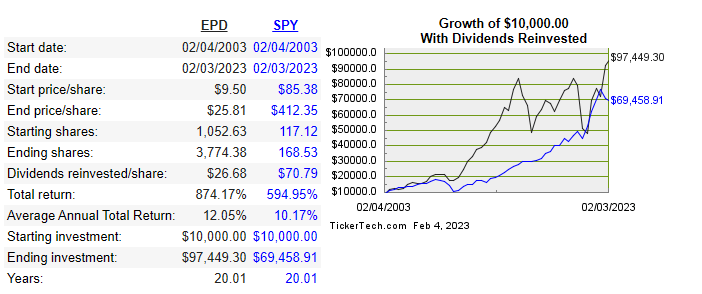

EPD hasn’t always traded sideways, and if I go back 2 decades instead of 1, the unit price has appreciated by 172% (split adjusted) from $9.50 to $25.81. If that appreciation is replicated in the future is anyone’s guess. What’s interesting is the details from the results. In 2003, EPD was $9.50 and paid $0.72 per unit in distributions. An investment of $10,000 would have purchased 1,052.63 units of EPD, generating $757.89 in income. By reinvesting the distributions over the next 2 decades, the share base would increase to 3,774.38. Your annualized income based on the current distribution of $1.96 would be $7,397.78. When compared to investing in the SODR S&P 500 Trust (SPY), EPD would have outperformed SPY by 279.22% since 2/4/03, when the distributions/dividends were reinvested. The power of compounding is real, as shares of SPY appreciated by 382.96% compared to 172% for EPD, but due to the large distributions that were reinvested over the years, the total return from EPD ended up outperforming SPY. There is no indication that past performance will dictate future returns, but it is something to consider as this example, shown below, is a prime example of how compounding income investments overtime can pay large dividends down the road.

Dividend Channel

EPD reported a record 2022 and with its growth projects coming online, we could see increased DCF in the future

EPD had a great year as it generated $58.19 billion in revenue and $5.5 billion in net income attributable to common unitholders. EPD’s DCF increased by 17% YoY from $6.6 billion to $7.8 billion, which provided a 1.9x distribution coverage ratio. EPD was able to retain roughly $3.6 billion of DCF in 2022, allowing it to reinvest in itself, repurchase units, and reduce debt. EPD’s adjusted cash flow provided by operating activities increased 13% YoY from $7.1 billion to $8.1 billion. In Q4, EPD allocated $763 million to capital investments which included approximately 580 miles of pipeline purchases. EPD’s total capital investments in 2022 amounted to $5.2 billion, setting the stage for significant future growth. In 2022, EPD acquired Navitus Midstream for $3.2 billion, allocated $1.4 billion to growth projects, spent $160 million on pipeline purchases, and deployed $372 million toward CapEx.

EPD’s ability to invest in itself and deliver on organic growth projects is a main contributor to these results. A critical component to EPD’s success is its ability to increase capacity and facilitate increased volumes as the global energy demand increases. 2022 was a pivotal year that demonstrated EPD’s ability to capitalize on the increasing demand for traditional energy sources. EPD’s Natural Gas Liquids (NGLs), crude oil, refined products & petrochemical pipelines saw a 4.69% YoY increase in volume to 6.7 million BPD. EPD’s marine terminal volumes increased 13.33% to 1.7 million BPD. Its natural gas pipeline volume increased 20.42% to 17.1 TBtus/d. EPD’s NGL fractionation volumes increased 6.86% to 1.34 MBPD. Their Propylene plant production volumes increased 2.02% to 101 MBPD. EPD’s fee-based natural gas processing volume increased 26.83% to 5.2 Bcf/d. Lastly, EPD’s equity NGL-equivalent production volumes increased 8.98% to 182 MBPD.

EPD

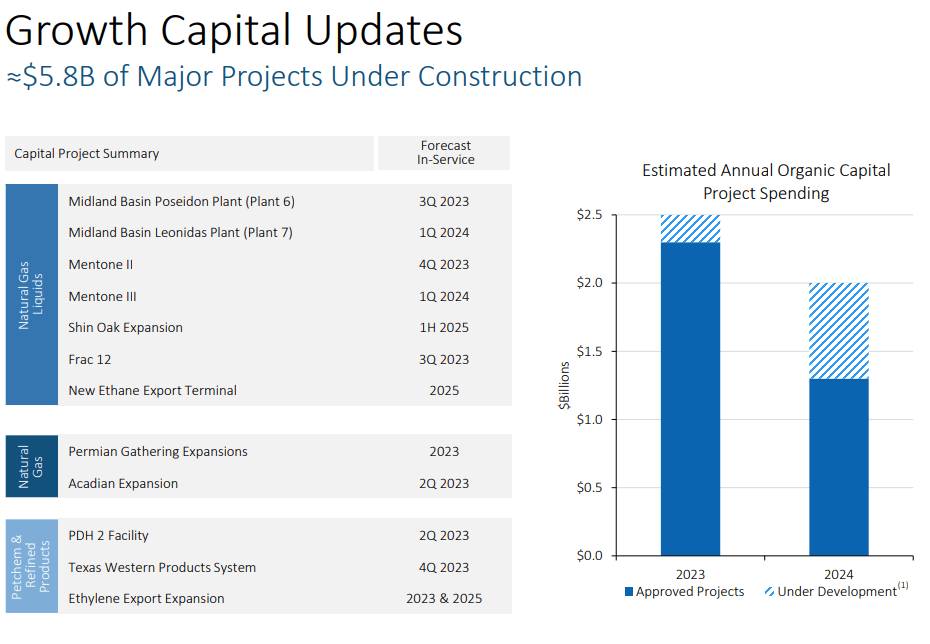

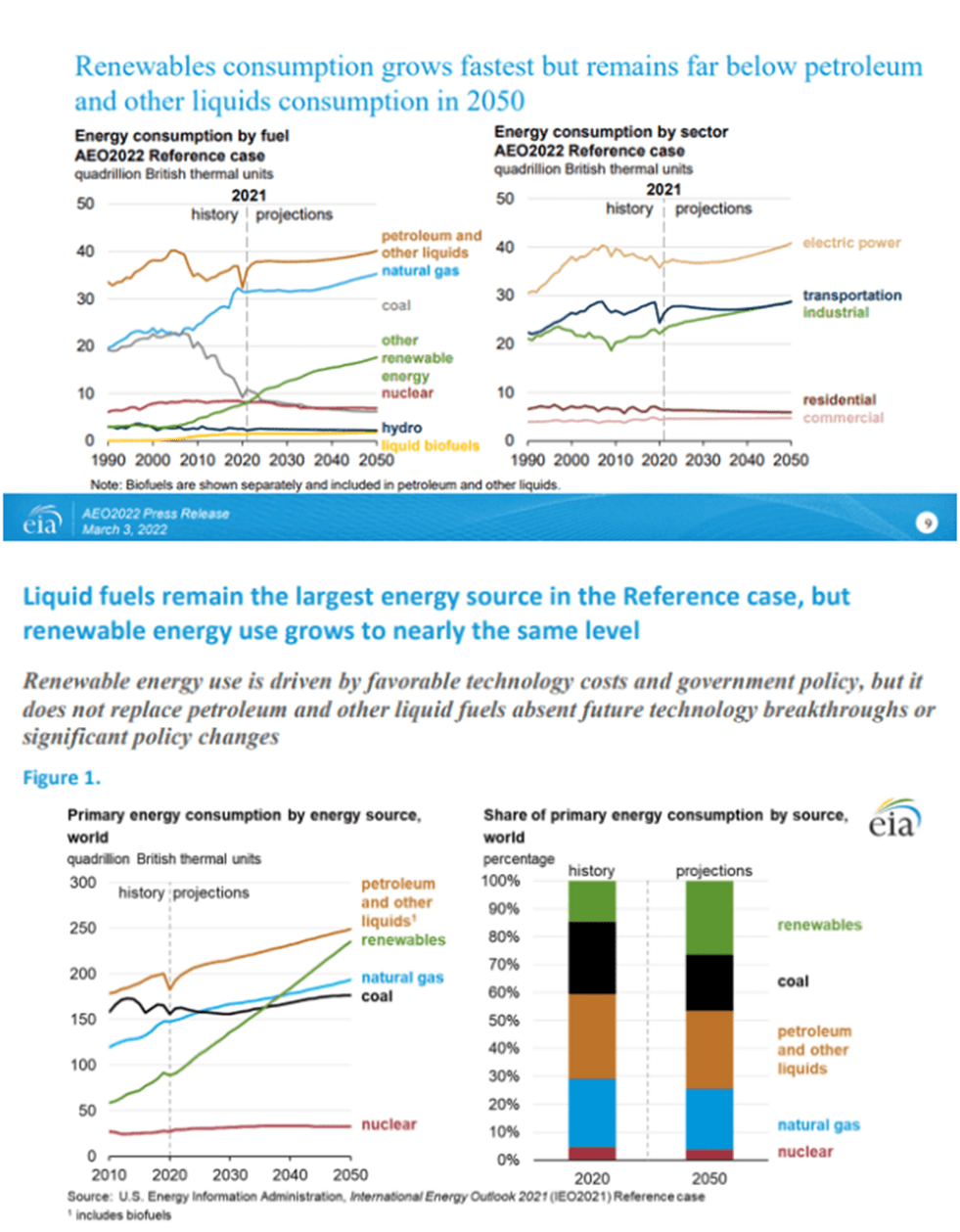

EPD has 12 major projects under construction. 7 of these projects will come online throughout 2023, then another 2 projects in 2024, and the final 3 in 2025. As these projects come online, EPD is projected to reduce the amount it allocates toward organic growth projects, which could increase the amount of DCF allocated to distributions and buybacks. The current projects under construction will provide additional capacity to EPDs network to support the future global energy demand. 2022 was a clear indication of how additional volume drives revenue, net income, adjusted EBITDA, and DCF for EPD. On 3/3/22, the EIA released its 2022 Annual Energy Outlook and concluded that petroleum and natural gas remain the most consumed sources of energy in the United States through 2050 (1st slide below). The EIA publishes its international energy outlook every 2 years, and the last one was published prior to the war in Ukraine. In 2021, on a global scale, traditional energy sources will also increase (2nd slide) due to the EIA’s predictions through 2050. As traditional sources of energy increase, more fuel will need to move through EPF’s network, which will correlate to additional fee-based services, more revenue, and hopefully, additional levels of DCF.

EIA

Conclusion

2022 was a strong year for EPD, even though its units weren’t greatly rewarded. I believe that EPD is positioned for another strong year in 2023 and will become an unofficial Dividend Aristocrat after its 25th consecutive annual distribution increase. As an income investor, I am looking at the potential for future distribution increases, and EPD has the ability to continue its current trend for years to come. EPD is paying 51.61% of its DCF to unitholders in distributions, and the DCF could continue to grow as additional projects come online and increase the capacity through EPD’s system. I think EPD is undervalued as its system is next to impossible to replicate, and the barriers to entry are almost unattainable for new competitors. EPD has everything that an income investor could want and is worth conducting further research on to see if it fits your investment framework.

Be the first to comment