kyletperry

Enterprise Products Partners (NYSE:EPD), after a decade of lackluster performance, is looking like a great bet here. In recent years, the company has taken intentional steps to reduce its reliance on capital markets to fund its distributions and capital expenditure requirements. With free cash flow now fully covering both the distribution and CapEx, EPD has a well-secured distribution that is not being adequately valued by Wall Street. The stock is yielding nearly 8% and may even provide multiple expansion potential if sentiment improves, as investors may begin to appreciate the long term positioning of midstream assets.

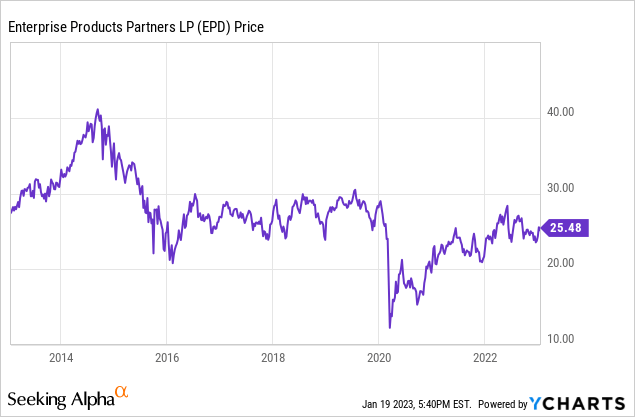

EPD Stock Price

EPD is trading at the same price it did over a decade ago. That underperformance has led the dividend yield to rise from 4.6% in 2012 to 7.8% at present day.

I last covered EPD in October where I rated the stock a buy due to the attractive valuation and potential for improving sentiment. That thesis remains intact and I expect it to be just a matter of time before EPD starts to trade more like an “energy landlord.”

EPD Stock Key Metrics

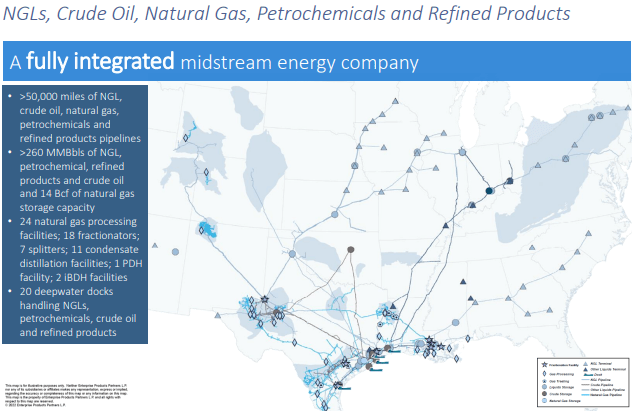

EPD is one of the largest midstream energy companies in the nation with over 50,000 miles of pipelines transporting NGLs, crude oil, natural gas, petrochemicals, and refined products.

November Presentation

EPD has benefited from the rise in commodity prices but not nearly as much as E&Ps, as EPD’s revenues are mostly volume-based and do not fluctuate based on price. Through the first 9 months of 2022, EPD has seen revenue increase 51% YOY to $44.5 billion, driven largely due to 67% growth in NGL revenues. Much of that revenue growth was offset by growth in cost of revenues as these were mostly driven by the rise in commodity prices. Gross operating margin, an arguably better financial metric to track, has risen by “only” 7.2% (again through the first 9 months of 2022).

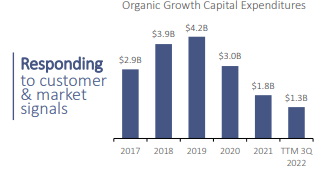

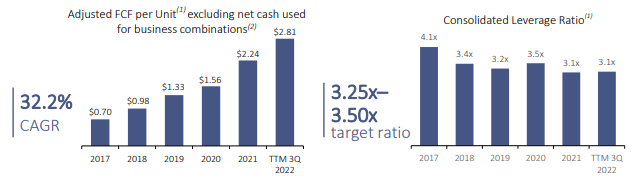

That solid growth comes even as EPD reduced its growth capital expenditure program significantly from prior years. Whereas EPD spent $4.2 billion on growth capital in 2019, the company has only spent $1.3 billion thus far in 2022.

November Presentation

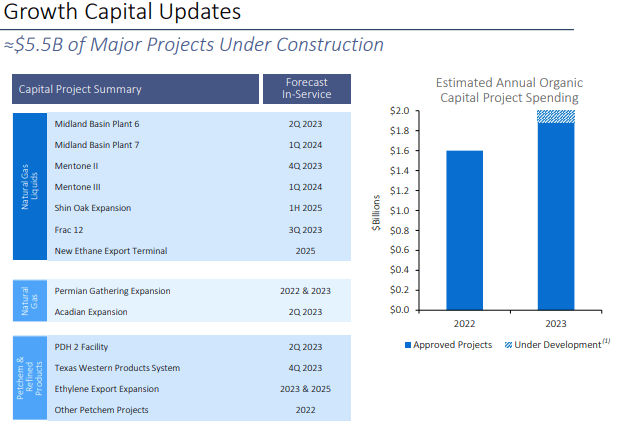

On the conference call, management stated expectations for around $1.6 billion in growth capital spend in 2022 and around $2 billion in 2023. In contrast with prior quarters, management sounded more confident in that 2023 number, stating that “it’s hard to see that moving materially higher.”

November Presentation

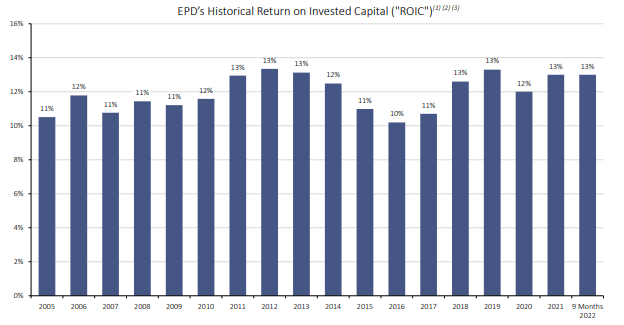

The subject of growth capital is a bit complicated for EPD. On the one hand, EPD has a long track record of executing on growth projects, as evidenced by its high historic return on invested capital (‘ROIC’).

November Presentation

On the other hand, I expect many investors would prefer for EPD to more resemble typical cash generating stocks through greater free cash flow generation and unit repurchases. EPD management appears to be listening to its investors, as its investor slides are showing greater focus on free cash flow per unit. EPD repurchased 3.9 million units at a cost of $95 million in the most recent quarter, bringing its year-to-date total to $130 million.

November Presentation

EPD ended the quarter with 3.1x debt to EBITDA. That is lower than its target 3.25x to 3.5x range, but management stated that they intend to stay near the lower end of that range due to the rising interest rate environment and risk of recession. I previously had hoped that the company can utilize its balance sheet for aggressive buybacks – those hopes have vanished.

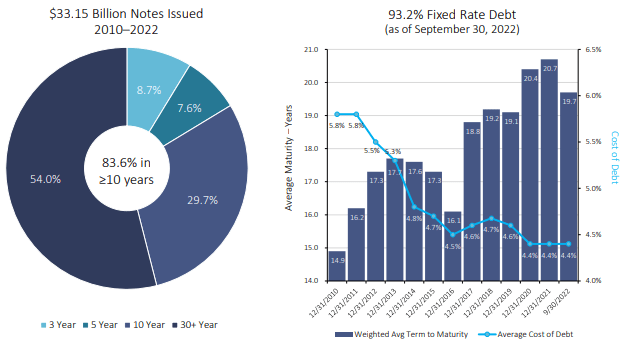

EPD maintains a strong balance sheet with 93.2% fixed rate and 83.6% of its debt maturing in 10 years or greater. The overall low leverage and carefully managed balance sheet are a key factor in why this company is often considered to be one of the lowest risk in the sector.

November Presentation

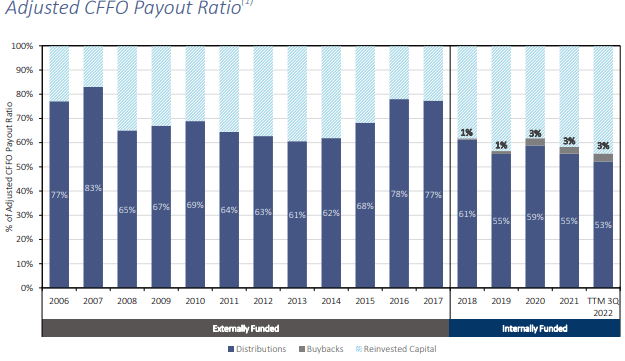

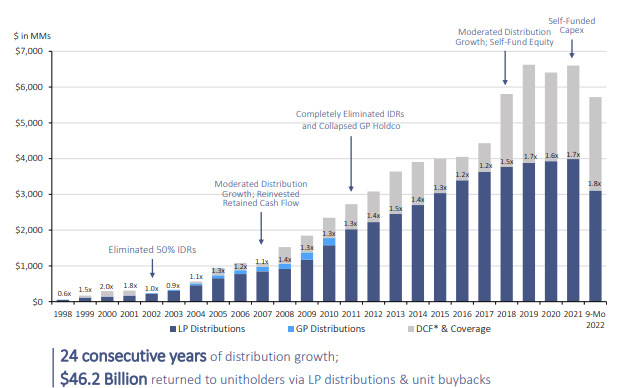

Not only that, but EPD has successfully been able to internally fund distributions, buybacks, and growth capital expenditures over the last several years.

November Presentation

EPD has differentiated itself in the midstream sector, which has resulted in slower distribution growth in previous years but has now set up the company for potentially faster growth in the coming years.

Is EPD Stock A Buy, Sell, Or Hold?

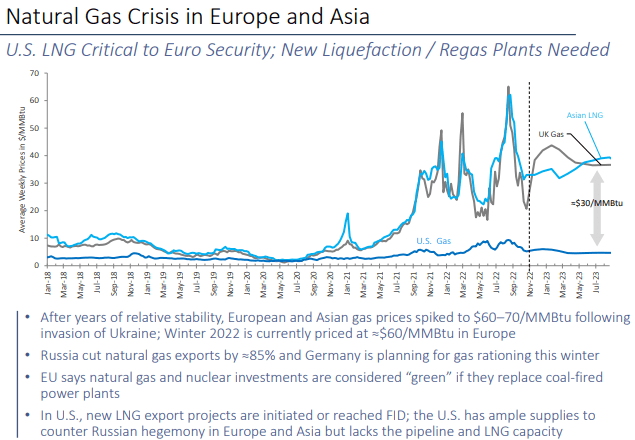

At recent prices, EPD was trading at a 7.8% distribution yield and at around 9X free cash flow. At first glance, that valuation may seem just-OK for an energy stock, but one must remember two factors. First EPD is a midstream company and thus deserves a premium valuation within the energy sector due to the greater consistency of its revenues. Second, Wall Street may be underestimating the potential for a sentiment shift for midstream operators. I see increasing potential for the United States to become a greater exporter of oil and natural gas, especially as a result of the Russian – Ukraine war.

November Presentation

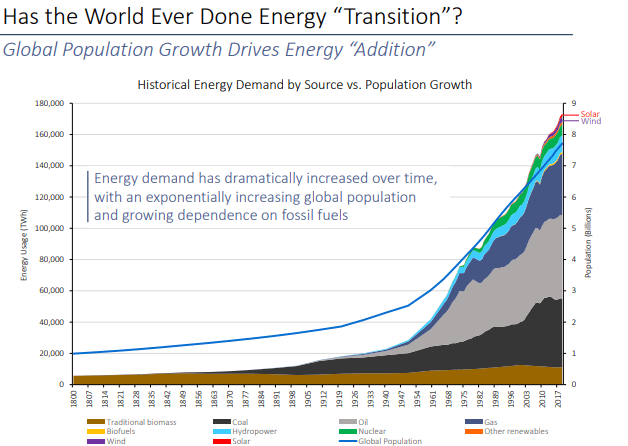

Investors, including yours truly, may have underestimated the time it will take for a renewable transition to take place. The reality is that much of the world continues to see growing energy demand, something that simply cannot be addressed so quickly through renewable energy sources.

November Presentation

Perhaps commodity prices may see some volatility in the near term due to recessionary risks. However, I will not be surprised if over the coming years, it becomes clear that commodity demand remains strong, and financials remain ever so resilient at EPD. That may lead to multiple expansion at the stock – perhaps EPD may be able to trade more like more like a utility or REIT, with its distribution yield compressing to around 5%.

It is also important to note that not only has EPD greatly increased the safety of its distribution, it also is about to become a dividend aristocrat this year as it will likely be the 25th consecutive year of distribution increases.

November Presentation

That might not lead to inclusion in dividend aristocrat ETFs, unfortunately, due to the K-1 tax form. Nonetheless, it would be yet another validation of management’s strong track record of execution.

Based on management’s guidance for around $2 billion in growth capital expenditures next year, perhaps around $400 million of sustaining capital expenditures, EPD should generate at least $5 billion of free cash flow this year. Unit distributions should total around $4 billion, meaning that there is an additional $1 billion of excess free cash flow that could be put towards unit repurchases, debt paydown, accelerated distribution growth, or M&A. With leverage as conservative as it is, I do not see any need to pay down debt. If EPD can put that excess cash towards unit repurchases and more accelerated distribution growth, then I can see the multiple expanding meaningfully.

What are the key risks? While the past two years have clearly shown the importance of the energy sector, it is possible that commodity prices crash anyways. That may lead to near-term financial instability at EPD’s counterparties, and the stock may take a hit as a result. Further, there’s no guarantee that management will continue to prioritize free cash flow generation over investing in growth projects. While I expect the company to deliver solid execution on growth capital spending, I view a balanced approach between growth projects and unit repurchases as being critical for further multiple expansion. I continue to find EPD to be highly buyable here for both investors looking for consistent distribution growth, as well as those looking for multiple expansion potential.

Be the first to comment