Mongkol Onnuan

Article Thesis

Enterprise Products Partners (NYSE:EPD) has offered another dividend increase this January. The dividend growth track record improves further, while the dividend increase also lifted EPD’s dividend yield further — from an already attractive level. With an economic slowdown being expected by many, resilient Enterprise Products is a safe high-yield pick for those seeking a sleep-well-at-night investment in the current environment.

Enterprise Products: Strong During A Recession

Many investors, analysts, and company executives are forecasting a recession this year. This includes, among others, the likes of Elon Musk (CEO of Tesla (TSLA)) and Jamie Dimon (CEO of JPMorgan Chase (JPM)). And they have good reasons to expect a recession:

– High inflation results in real wage losses for many consumers, which is why they are scaling back their spending. With many consumers being forced to spend more on food, energy, gasoline, etc. they are even less likely to spend heavily on discretionary items such as apparel, electronics, and so on.

– High and rising interest rates pose a major headwind for home construction, which hurts homebuilders and their employees.

– High and rising interest rates also make it more costly to finance a new vehicle, new machinery, and so on, which is why spending on big-ticket items by both consumers and businesses will slow down.

Add uncertainties due to the ongoing war in Ukraine, and there is a perfect storm for an economic downturn in both the US and many other parts of the world, such as Europe, which is also hit by an energy crisis.

In an uncertain environment, stocks that perform well during all kinds of macro pictures are particularly valuable. This holds true for Enterprise Products. Since energy commodities are still trading expensively, EPD is even better positioned during the current/upcoming economic downturn, relative to the “average recession”.

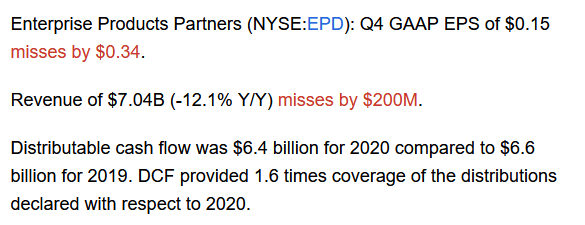

Looking back at Enterprise Products’ recession performance in 2020, we see the following:

Seeking Alpha

Revenue was down year over year, but that does not translate into an earnings and cash flow decline of a similar magnitude. For some of EPD’s business units, commodity prices are both a revenue driver and an expense. When commodity prices rise, both its revenue and expenses climb, while both fall when commodity prices pull back. Overall, profits and cash flow are thus not really dependent on commodity prices, especially since there are many fee-based contracts in place anyways. That is why Enterprise Products was remarkably able to generate distributable cash flows that were down only 2% from 2019’s level in 2020, despite a massive shock to global oil markets. While oil prices were even negative for a short period of time, and while many energy companies ran into major trouble, EPD generated 98% of its pre-crisis cash flows. Not surprisingly, its dividend coverage remained very healthy, as the company managed to cover its payout at a ratio of 1.6, which pencils out to a 63% payout ratio, even during a period when the broad energy industry was running into considerable problems and when many energy companies cut their dividends.

Enterprise Products thus has proven to operate with a recession-resilient business model that can withstand external shocks, such as lower oil demand, lower refinery utilization, declining commodity prices, and so on.

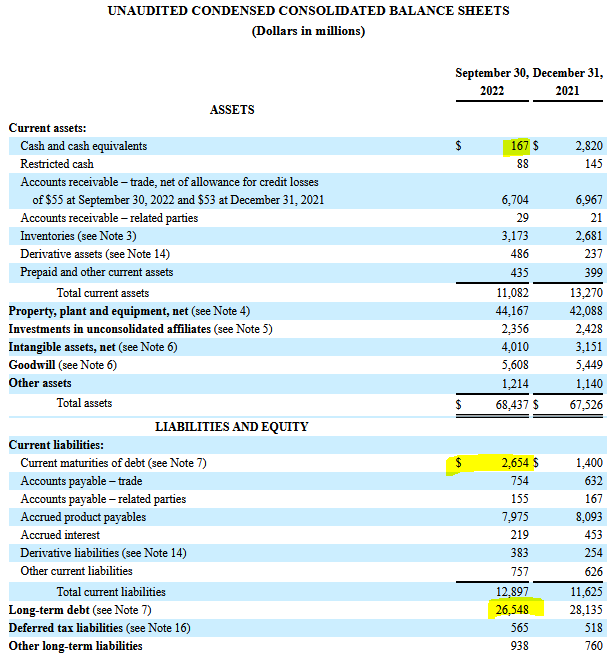

Even better, Enterprise Products also offers other reasons to see it as a sleep-well-at-night stock. First, its balance sheet is tremendously strong for an energy midstream company. Enterprise Products’ balance sheet looked like this at the end of the most recent quarter:

EPD 10-Q

The company’s net debt position totaled $29.0 billion at the end of the quarter. At the same time, Enterprise Products managed to generate EBITDA of $8.5 billion over the last four quarters, which means that Enterprise Products’ net debt to EBITDA ratio is just 3.4. When we look at adjusted EBITDA as calculated by Enterprise Products, the leverage ratio is even lower, at just 3.1. That is significantly below the company’s target range of around 3.5. Enterprise Products could thus add around $4 billion to its net debt and it would operate with a net leverage ratio that would be perfectly in line with what management sees as ideal. In other words, one could call Enterprise Products “underleveraged” today.

Rating agencies generally deem leverage ratios up to 4.5 reasonably strong for energy midstream companies. By that logic, Enterprise Products could add around $13 billion in net debt without trashing its balance sheet, even if that added net debt does not at all result in any additional EBITDA — which would be the case if EPD used the cash proceeds for organic growth projects and/or for acquisitions. No matter what, it is pretty clear that EPD has a strong balance sheet, which reduces risks for investors, as the company is well-positioned to stomach any unexpected issues. The fact that Enterprise Products has more than $3 billion of undrawn credit capacity means that liquidity isn’t an issue, either.

For anyone worrying about the outlook for the US economy (or the global economy), Enterprise Products could thus be a worthy choice. The company has proven its resilience versus recessions in the past and is going into this downturn with a fortress balance sheet with massive surplus liquidity. In fact, if a major downturn were to occur, Enterprise Products might benefit from that: Its strong balance sheet and available resources could allow EPD to consolidate the industry by taking over weaker peers or by acquiring assets at attractive prices from weaker companies that need immediate cash inflows.

EPD’s Dividend Keeps Growing

Enterprise Products has a strong track record of growing its dividend. According to Seeking Alpha’s data, the company has increased its payout for 23 years in a row:

Seeking Alpha

That’s immense, relative to what the broader industry has managed to deliver in terms of consistent dividend growth. Not surprisingly, EPD receives an A+ rating for its dividend growth. The dividend growth rate is pretty compelling, as Enterprise Products has increased its payout by 4% annually over the last decade. While that wouldn’t be attractive for a low-yielding stock, where a high dividend growth rate is needed, EPD with its dividend yield of 7.8% is pretty attractive if that dividend continues to grow by 4% a year. All else equal, one could guesstimate EPD’s future total returns in the 12% range under those conditions. Even better, EPD’s dividend growth has actually accelerated in the recent past.

Over the last year, EPD has increased its payout twice. Once during the summer of 2022, when the company increased its payout from $0.465 to $0.475. And this January, Enterprise Products increased its dividend again, lifting it by $0.015 to $0.49 per share per quarter. Overall, that makes for a 5.4% dividend increase relative to where the dividend stood one year ago.

There is no guarantee that dividend growth will remain at this level forever, but even if it were to fall to just 2% — which would be half the dividend growth rate EPD has achieved over the last decade — Enterprise Products would be a very solid dividend pick, I believe. In this (rather bearish) scenario, the dividend yield on cost would grow to 8.6% over the next five years, and to 9.5% over the next decade. If dividends aren’t consumed along the way, but reinvested for additional shares instead, investors could receive a yield on cost of 12.5% five years from now, or 20.2% a decade from now.

There are no guarantees that the dividend will grow in the future, but based on EPD’s past track record, the far-from-high payout ratio, and due to the fact that EPD continues to benefit from rate increases on existing pipes and from the building of new assets, I believe a 2% annual dividend growth rate is far from an aggressive target. And even though the 2% annual dividend growth example is rather bearish versus EPD’s historic growth rate, the results are quite compelling.

Takeaway

In terms of recession resilience, balance sheet strength, consistency of business growth and dividend growth, management quality, etc. EPD is one of the best energy midstream companies investors can pick from.

Today, shares offer a pretty high dividend yield of 7.8%, the dividend has just been raised, and shares are not expensive, trading for just 10x this year’s net profit — despite the fact that net profits are generally artificially low for midstream companies due to high non-cash depreciation charges.

With shares trading well below the 52-week high and at an attractive yield & valuation, I deem Enterprise Products attractive at current prices.

Be the first to comment