bkindler/E+ via Getty Images

Introduction

Enterprise Financial Services (NASDAQ:EFSC) is the holding company of the Enterprise Bank & Trust, a Missouri-based bank with activities in several other states as well. The bank caught my attention as it has a series of preferred shares outstanding.

A robust earnings profile

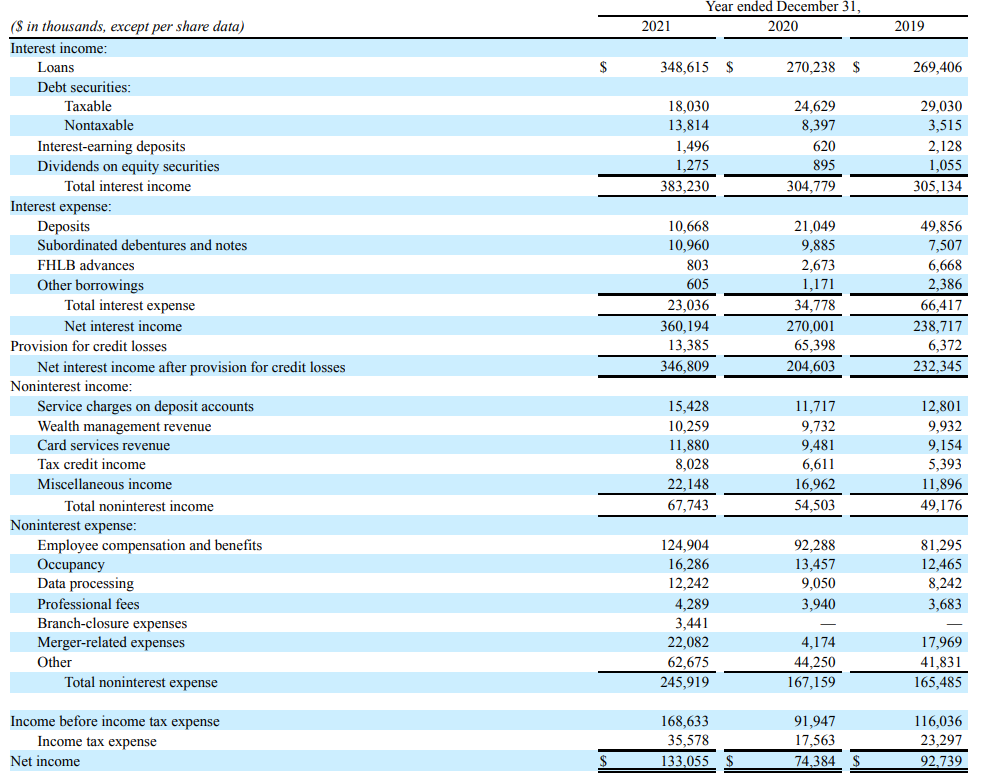

Enterprise’s balance sheet expanded by about 50% as the bank completed the acquisition of the First choice bank, which operated eight branches in Southern California with total assets of $2.3B. There also was some organic growth at Enterprise Financial and this resulted in a substantial increase of the interest income. After seeing some stagnation in 2020, the interest income increased to in excess of $383M while the interest expenses fell by almost a third. The combination of an increasing interest income and decreasing interest expense resulted in a very impressive 33% increase in the net interest income, which reached $360.2M.

EFSC Investor Relations

The bank also saw its net non-interest expenses increase from $113M to $178M, but if you would exclude the merger-related expenses in both financial years, the increase was more benign ($156M coming from $109M) and the higher net interest expenses made up for the higher underlying operating expenses.

The bank also recorded a $13.4M provision for loan losses bringing the pre-tax income to $168.6M whereas the net income was $133M or $3.86 per share. Keep in mind the EPS is based on the average share count. Applying the year-end share count of 39.8M shares would have reduced the EPS to $3.34. And on top of that, as the bank only issued its preferred shares toward the end of the year, the financial results don’t include any preferred dividends yet. With $75M of preferred shares outstanding with a 5% preferred dividend, the net income attributable to the common shareholders of Enterprise Financial would be roughly $3.75M lower. But of course, if you’d assume the merger-related expenses will disappear, the bottom line will increase by about 10% anyway.

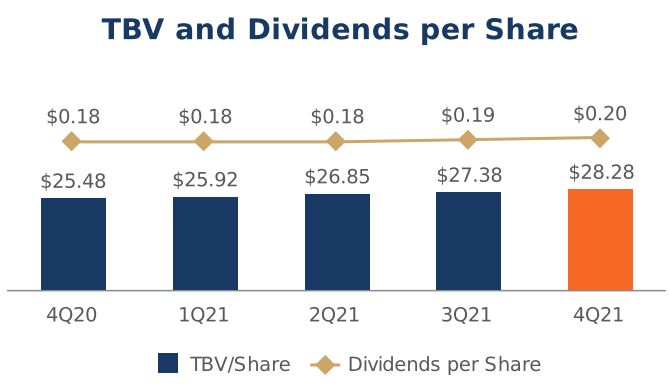

The bank is currently paying a quarterly dividend of $0.21 per share (for an annualized dividend yield of approximately 1.75% at the current share price) and the majority of the bank’s earnings are retained on the balance sheet. This results in a gradually and continuously increasing book value but the current P/TBV of around 1.7 is a little bit too rich for me. Note, the image below still shows a quarterly dividend of $0.20 as the presentation predates the recent dividend hike.

EFSC Investor Relations

An even more robust balance sheet – but be mindful of the commercial and CRE focused loan book

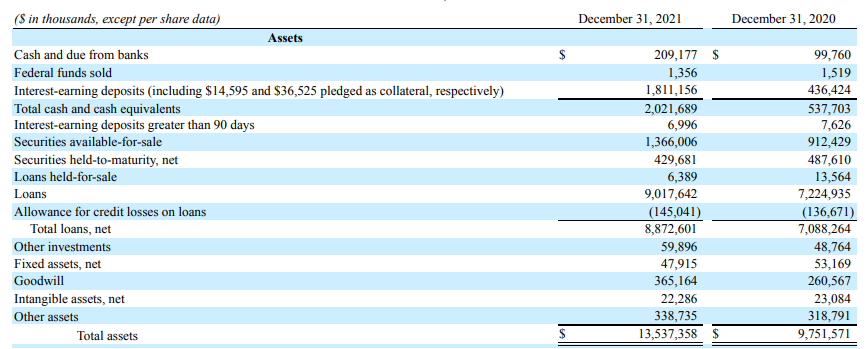

The combined entity now has a balance sheet size of just over $13.5B, an increase of $3.8B compared to the situation as of the end of 2020. I was positively surprised to see a disproportionably high percentage of these new funds was invested in what should be very safe investments. The cash position increased by $1.5B while the net investment in securities (both on an available-for-sale as well as a held-to-maturity basis) increased by $400M. So about 50% of the balance sheet expansion was actually invested in rather safe issues.

The total position in cash and securities thus increased to in excess of $3.8B, which is approximately 28% of the balance sheet.

EFSC Investor Relations

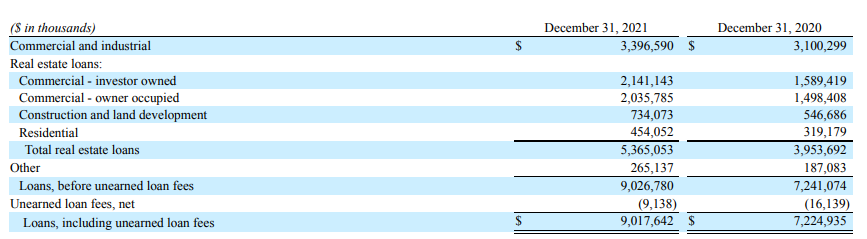

I’m obviously quite interested in the $9B loan book and that loan book seems to be heavily focusing on commercial loans and commercial real estate as those make up over 80% of the total loan book. This likely also explains why Enterprise Financial wants to offset these higher risk loans with a very strong position in liquid securities.

EFSC Investor Relations

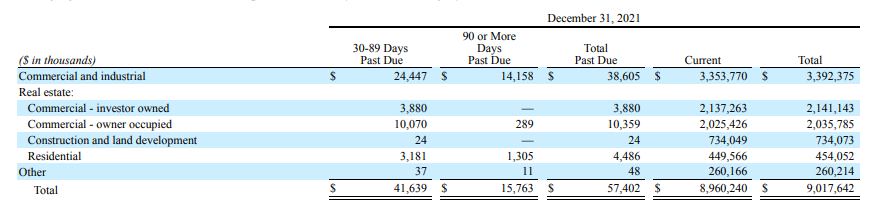

That being said, the total amount of loans past due is pretty low, at just over 0.6% of the loan book. And within excess of $145M in allowances for loan losses, the risk appears to be pretty well covered.

EFSC Investor Relations

Investment thesis

I’m getting interested in the bank’s preferred shares. Not only is Enterprise’s balance sheet quite robust with almost $4B of its assets invested in cash or very liquid securities, I’m also quite happy to see the size of the preferred issue was rather small at just $75M. This represents just 5% of the total equity value of the bank while the preferred dividend of $3.75M is covered by the $130M+ in net income (which will likely increase given the increasing interest rates and the lack of merger-related expenses this year).

Trading at less than $22/share, the preferred shares, trading as (NASDAQ:EFSCP) seem to be offering good value here. The 5.72% (non-cumulative) yield isn’t high. But the risk/reward ratio is still quite appealing from an income perspective. Of course, an investor with exposure to preferred shares only is basically giving up the potential for capital gains as the preferred securities will trade depend on the market interest rates. And with an anticipated EPS which I think will be close to $4.75 this year, one shouldn’t give up on the common shares just yet. But I’m mainly keeping an eye on Enterprise for the preferred shares.

Be the first to comment