Eloi_Omella

Introduction

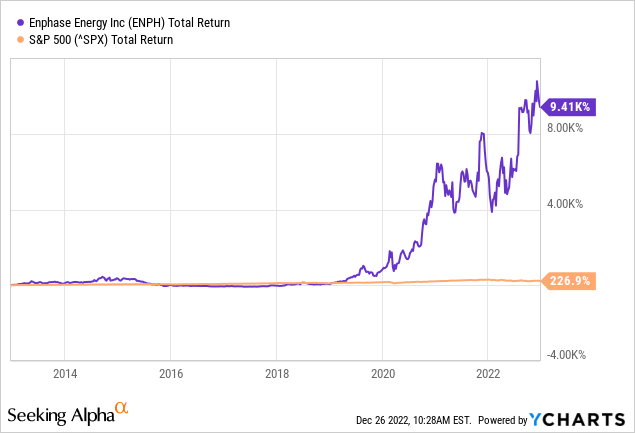

The price of Enphase Energy, Inc. (NASDAQ:ENPH) shares has skyrocketed in recent years. For the past decade, it has returned an annualized 26.4%. The company has been successful because it is active in the solar industry, which is part of a clean energy megatrend.

The company’s quarterly performance was above expectations. The rapid expansion of the business is due to the high quality of the products offered, and its excellent customer service. The business was able to significantly cut its costs, which resulted in a significant increase in its gross margins. When the price of Enphase shares falls, I add many shares to my investment portfolio.

Company Overview

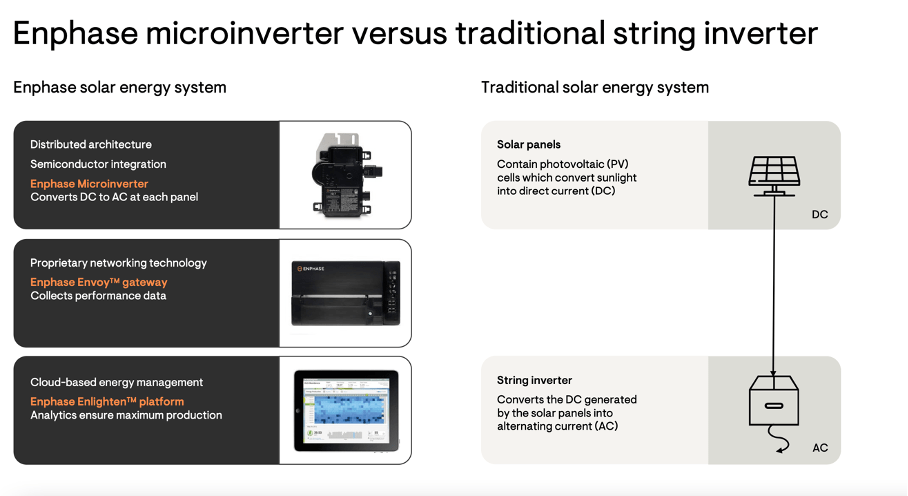

Enphase competitive advantage (Enphase 3Q22 investor relations)

Solar microinverters, designed and manufactured by Enphase Energy, are used to transform DC electricity generated by solar panels into AC electricity suitable for usage in homes and businesses.

Microinverters from Enphase are compatible with a wide range of solar panel systems and are made to be simple to set up and maintain. More than a hundred countries use the company’s technology in solar energy systems for homes, businesses, and utilities. Enphase provides more than just microinverters; they also sell battery storage systems and software to keep tabs on and improve upon energy output and consumption patterns.

Enphase Operates In A Large Total Addressable Market

Enphase SAM (Enphase 3Q22 investor presentation)

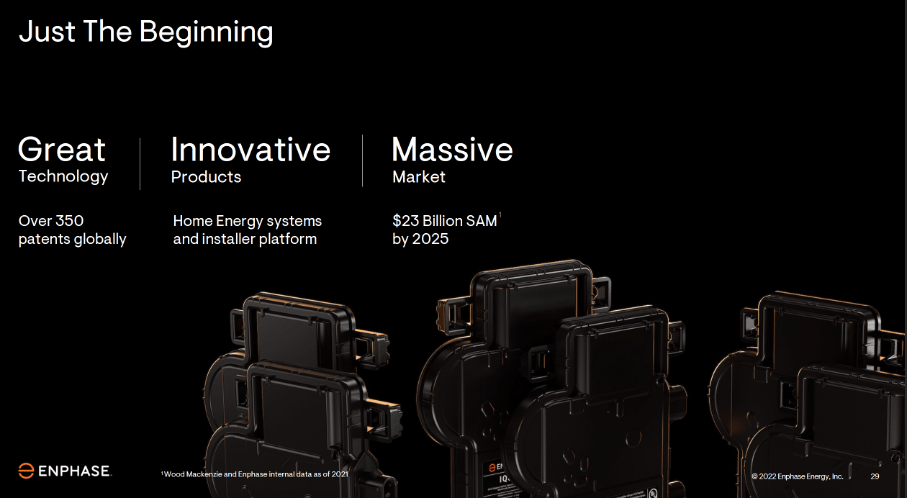

The term “serviceable addressable market” (SAM) refers to the total demand that might be met by the company’s offerings. Due to the fact that the total addressable market (“TAM”) takes into account the demand for all solar energy products and services, not only those offered by Enphase, the size of the SAM may be smaller than the TAM.

Solar energy system demand from residential, commercial, and industrial consumers, as well as demand from utilities and other large-scale energy users, are all accounted for in Enphase’s SAM. According to Enphase, its SAM will reach $23 billion by 2025. In 2025, revenue is projected to be $4.7B, which would put Enphase’s share of the market at 20%. There is still a lot of room for Enphase to grow, as the company is expanding rapidly and acquiring market share.

Enphase Is Well Positioned In The Industry Megatrend

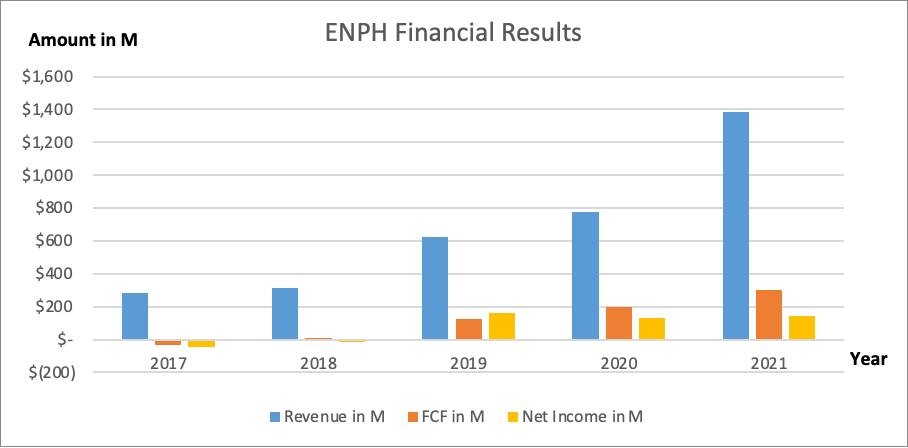

Due to the energy transition, Enphase Energy is able to thrive in a rapidly expanding market. Revenue has increased by 48% per year on average over the last four years. Net income has turned positive, and free cash flow is expected to reach $300 million by 2021. There are strong expectations about the company’s growth: Twenty-three analysts have increased their projections for revenue and earnings per share. They anticipate sales will increase annually by 31%, reaching $3.95B by 2024. Expected average EPS growth from 2022 to 2024 is 25% annually. These are ambitious forecasts, but I have little doubt that Enphase will reap many rewards from the solar industry megatrend.

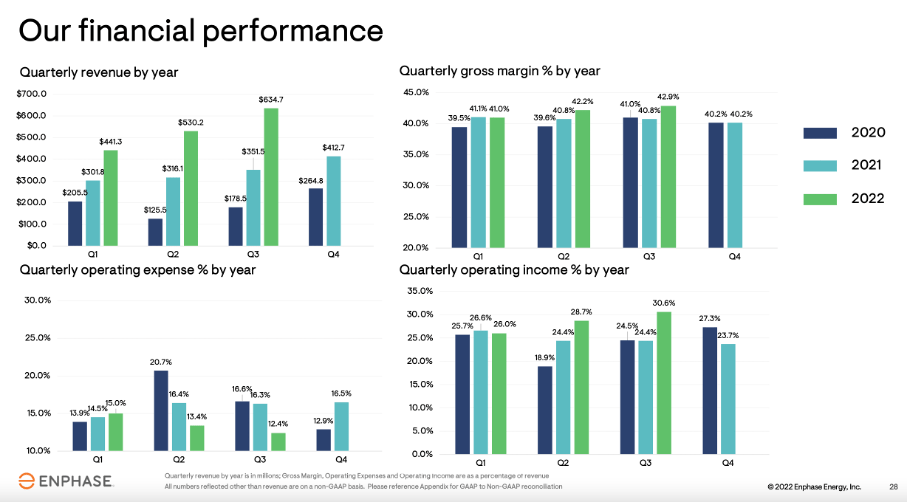

Enphase financial highlights (SEC and author’s own graphical representation)

The financial results for Enphase during the third quarter of 2022 were strong. Quarterly sales hit a new high of $634.7 million, up 80 percent year-over-year. The company’s free cash flow (“FCF”) was $179.1 million, an increase of 79% year-over-year, while the gross margin came in at 42.9%.

Financial performance (Enphase 3Q22 investor presentation)

In the third quarter, over 47% of all microinverter shipments were the brand new IQ8 model.

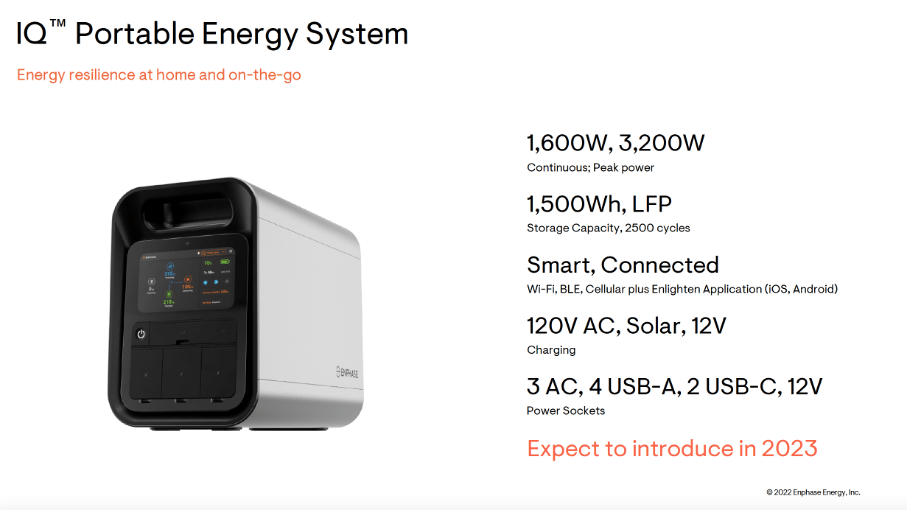

The company is poised for future success in the expanding solar energy market. The IQ Portable Energy System will be added to the company’s offerings alongside its present products and services to boost sales.

IQ Portable Energy System (Enphase’s 3Q22 investor presentation)

Enphase is also expanding its production capacity to meet rising demand. The current quarterly capacity of microinverter production is roughly 5 million. The first quarter of 2023 will see microinverter production in Romania, increasing the company’s quarterly output capacity to 6 million microinverters worldwide.

The Inflation Reduction Act (IRA) has extended the investment tax credit for residential solar to 30% for another 10 years and establishes a standalone storage investment tax credit with the same provisions.

Although there are numerous problems with the chip supply chain. There don’t appear to be any issues with Enphase. Improvements are being made in the distribution of individual components. CEO Badri Kothandaraman is optimistic:

There are still some spots of tightness that keep coming up from time to time and our operations team is doing a nice job closely managing the situation. The logistic situation has also improved a little bit with reduced shipping times.

The company’s rapid expansion in the sector’s mega-trend shows no signs of slowing down. The company’s recent boost from the European energy problem due to Russia’s gas boycott has made the energy transition a more urgent issue. I believe that thanks to its excellent market position, Enphase will continue to grow rapidly in the coming years.

Stock Is Expensively Valued

While the company’s growth prospects are bright, investors should also consider the current share price.

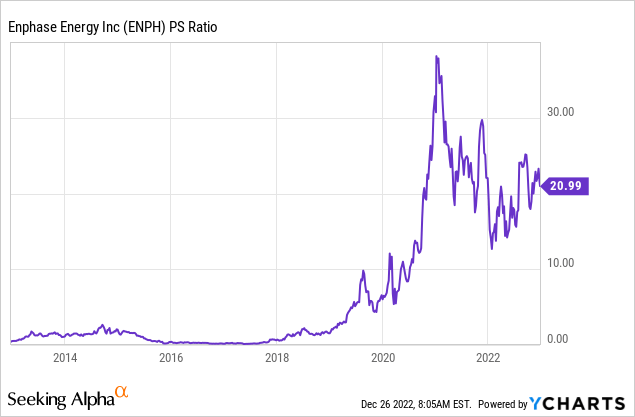

For a growth company, I normally prefer the price to sales ratio. With growing gross margins, as is the case with Enphase, this ratio is not preferred. Gross margin is 42% (GAAP), up from 20% in 2017.

Over the years, the company has grown significantly. With a Price To Sales ratio of 21, the company is highly valued. The P/S ratio has risen at an alarming rate, as the chart shows.

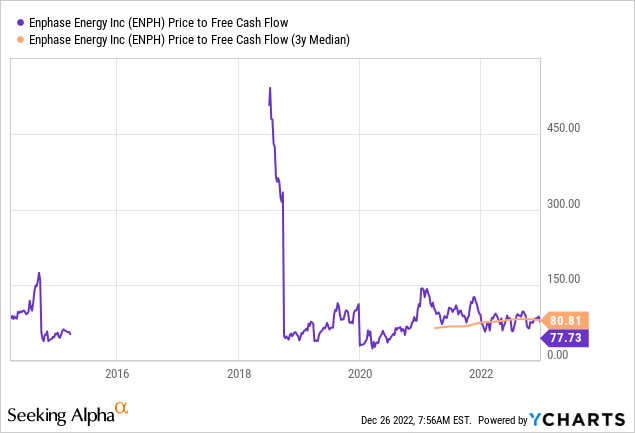

As a result of consistent growth in gross margin, a somewhat higher P/S ratio is expected. The P/FCF (free cash flow) ratio appears to be the preferable option for gaining insight into the company’s valuation. As can be seen in the graph below, the current P/FCF ratio of 78 is lower than the three-year average of 81.

With a 53% year-over-year rise from 2021, free cash flow is showing continued rapid expansion. At the current stock price, the price to free cash flow will be 23 at the end of 2025 if this rapid expansion is maintained over the next three years. Taking into account that the Federal Reserve raises interest rates to combat excessive inflation, I think the company’s current valuation to be somewhat pricey.

Conclusion

Solar microinverters are used to transform DC electricity generated by solar panels into AC electricity suitable for usage in homes and businesses. More than a hundred countries use the company’s technology in solar energy systems for homes, businesses, and utilities. Enphase is expanding rapidly and acquiring market share fast. Revenue has increased by 48% per year on average over the last four years.

Enphase Energy, Inc. showed strong quarterly results as sales increased 80% year-on-year. Analysts expect sales will increase annually by 31%, reaching $3.95B by 2024.

Enphase Energy, Inc.’s rapid expansion in the solar mega-trend shows no signs of slowing down. Costs are down and gross margin is increased to 42%, up from 20% in 2017. With a 53% year-over-year rise from 2021, free cash flow is showing continued rapid expansion. Enphase Energy, Inc. stock’s valuation is an important component for making an investment decision. I think the company’s current valuation to be somewhat pricey. When the price of Enphase shares falls, I add many shares to my investment portfolio.

Be the first to comment