Mumemories/iStock via Getty Images

Although the global print market continues to shrink in volume, COVID-19 sped up the rate for businesses to take their communication methods online. The demand will only reach zero after a while and surviving print businesses can gain market share as more of their competitors disappear. One company that has been benefiting from a diminishing market is Ennis, Inc. (NYSE:EBF), with a market cap of $536.36 million. It is considered one of the largest US private-label printed business product suppliers. Over the last year, investors have been rewarded with 10.66% returns.

One year stock trend (Seeking Alpha)

While volume decreases, print value continues to grow, driven by packaging, labels, and digital printing. EBF is a long-term and established business that has reported upward trending top and bottom-line results for the last seven quarters. It maintains a healthy balance sheet with positive free cash flow, continues to grow through opportunistic acquisitions in new markets and niches, and provides a consistent quarterly dividend. Its customers are distributors, which gives the company the ability for a local service while benefiting from its many facilities’ economies of scale and price negotiating power. Due to its slow growth, dividend and strong fundamentals, I recommend holding on to the stock.

Company overview

EBF is an over 100 years old manufacturer and supplier of print products for wholesale. Its customers are distributors, although it also sells to competitors and a small number of direct customers. Although the company is providing a service that is diminishing as the world becomes more paperless, it remains a compelling company in the industry with significant demand due to its wide variety of products, its portfolio of forty brands and its immense network of over 40,000 distributors, mainly within the USA. It employs around 2,500 workers across 55 facilities in 21 states. If you go onto their website, the layout feels outdated. Its employees are also older, and many have retired over the last years, however, it shows a traditional, and trusted business with strong network connections and brand value that remains a strength in this competitive environment.

Company at a glance (ennis.com)

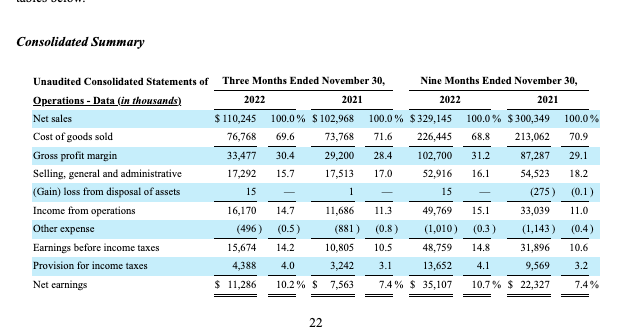

Revenue comes from the sale of commercial printing products, shipping and handling fees. The business has been experiencing increased demand, is cutting costs, and is quick to adjust pricing according to industry trends in paper, import demand, and operating costs. We can see that over the last three and nine months, the business has increased sales, and gross profit margin decreased the costs of goods and increased its earnings.

Q3 2022 versus Q3 2021 (sec.gov)

The business has grown through acquisitions of businesses in new markets and niches that strengthen fundamentals. Most recently in November 2022, EBF acquired School Photo Marketing (SPM) for a value of $8.8 million. The acquisition adds a customer base of over 1,400 school and sports photographers across the USA. In 2021, the company acquired AmeriPrint Corporation for $3.9 million in cash. AmeriPrint reported $6.5 million in sales for FY2020 and brings expertise in barcoding and variable imaging. Future acquisitions are to be expected, although nothing concrete has been mentioned.

Financials and valuation

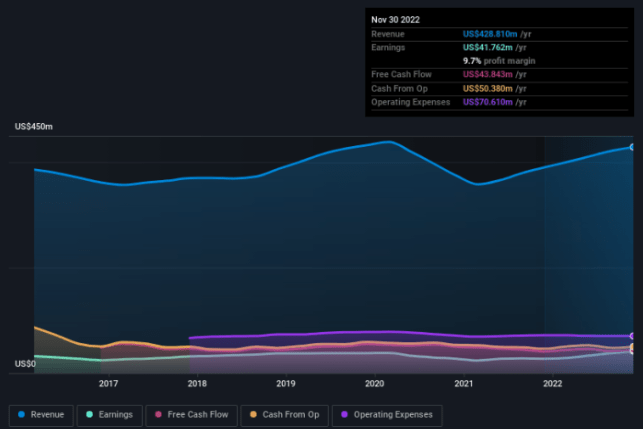

EBF has been delivering very stable financial performance. If we look at the last few years, there has been little revenue growth, however over the last seven quarters the company has been improving its net income and profit margins. In the last quarter of Q3 2022 we saw a revenue increase of 7.1% to reach $110.2 million, the net income increased YoY from the prior quarter by 49% to reach $11.3 million and the profit margin increased to 10% from 7.3% in Q3 2022, this was largely due to higher revenue. Earnings per share were $0.44 for Q3 2022 compared to $0.29 for Q3 2021. EBF has been benefiting from strong customer demand, cost-cutting and increasing its pricing to adjust for inflation.

Financial overview (simplywall.st)

One of the company’s strengths is its consistently healthy balance sheet, with little debt and sufficient cash flow to invest in acquisitions, pay out a dividend and cover operating expenses. If we look at the liquidity, we see a solid current ratio of 4.7 and a quick ratio of 3.37. The company’s TTM levered free cash flow was positive at $35.99 million, and cash from operations was $50.38 million. If we look at the annual trend, although cash flow isn’t increasing, it has remained consistent for years.

Levered free cash flow (Seeking Alpha)

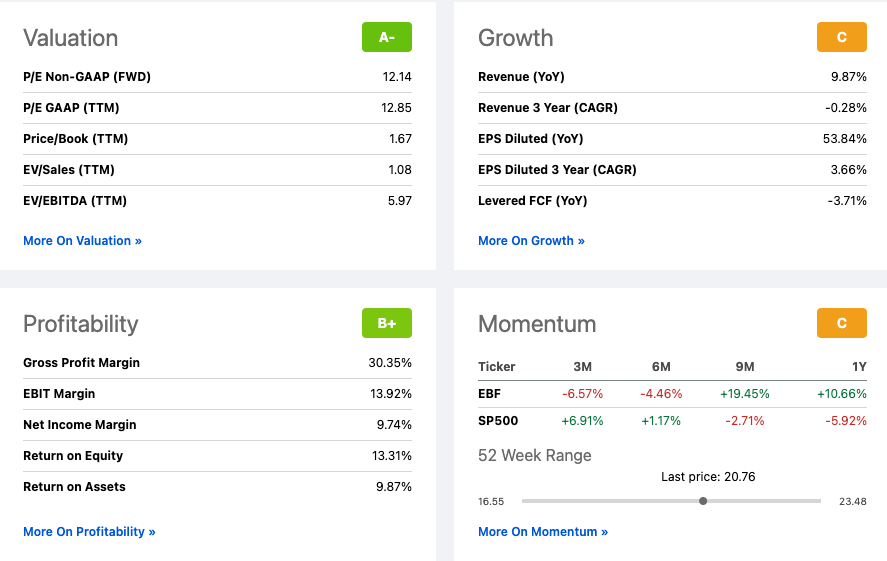

EBF is a dividend stock with a yield of 4.7% that has remained consistent, along with its stable cash flow and lack of debt. If we have a look at Seeking Alpha’s Quant ratings, we can see that EBF has a valuation of an A- grade rating, a price-to-earnings ratio of 12.14, a YoY growth of 9.87% and a gross profit margin of 30.35%

Seeking Alpha Quant Ranking and Grading (Seeking Alpha)

Final thoughts

The printing industry is going through product obsolescence through technological advancements, paper capacity changes, the market consolidation of its traditional supply chains, and increased global competition. At the same time, we are not expecting significant growth from this stock. EBF has proven itself a strong business through its consistent performance history while maintaining a healthy balance sheet and the ability to succeed in a diminishing market. It has recently acquired new capacities and channels, which will continue to benefit the company’s profitable and robust financials. Therefore I recommend holding onto the stock.

Be the first to comment