Mikhail Mishunin

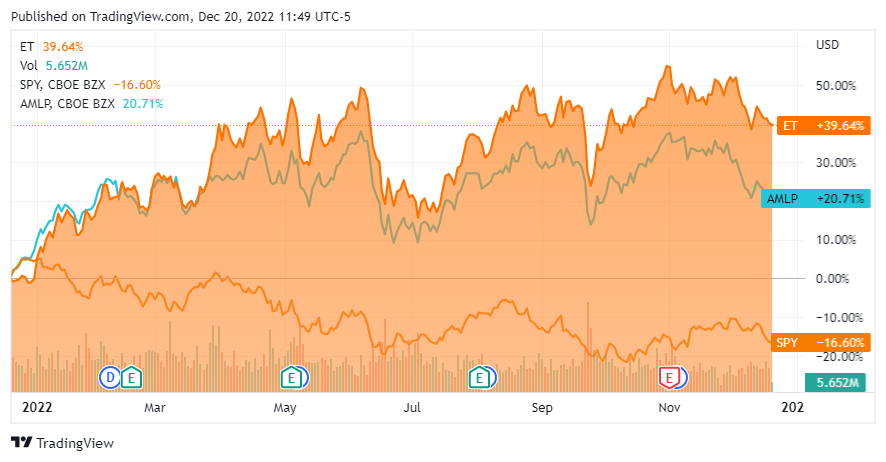

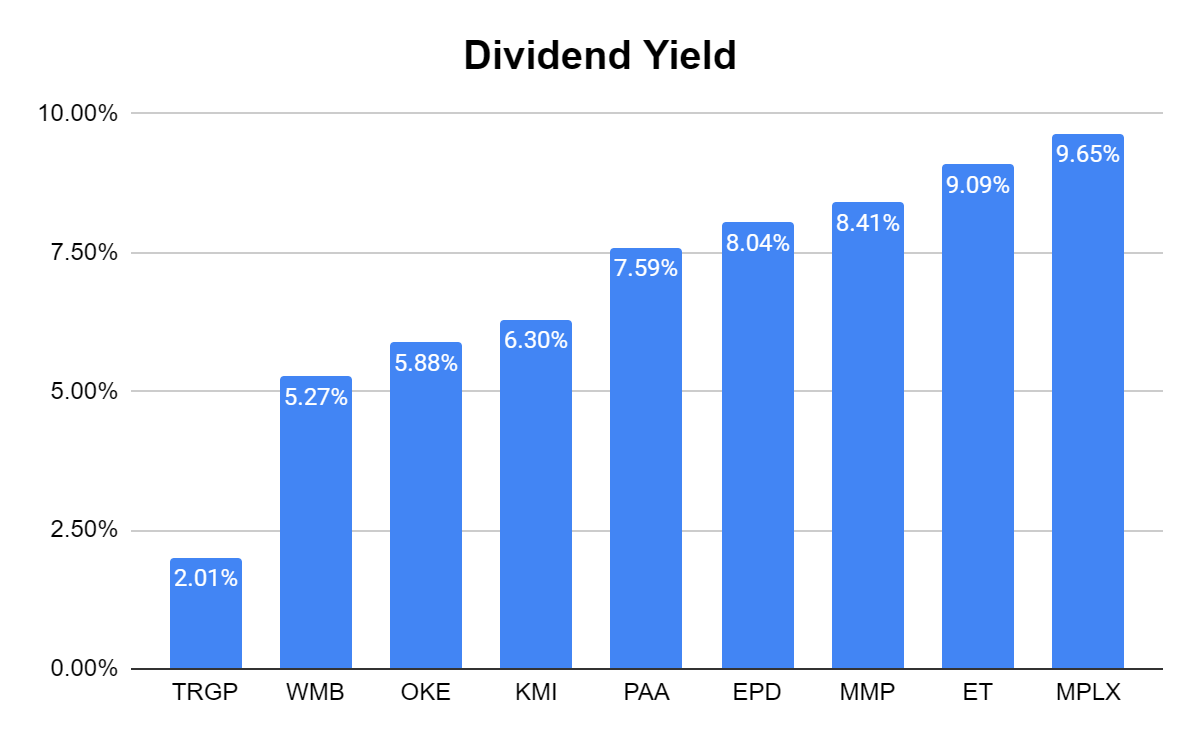

Units of Energy Transfer (NYSE:ET) have outperformed the market in 2022, and I believe there is further capital appreciation to be captured in 2023. YTD, ET has appreciated by 39.64%, the SPDR S&P 500 Trust ETF has declined by -16.60%, and the ALPS Alerian MLP ETF has appreciated by 20.71%. ET is AMLP’s top holding, representing 11.15% of the fund. ET is a stronger company operationally than in the past, and the world realizes that a transition to 100% renewables isn’t realistic in a short time frame. More LNG import capacity is being built in Europe and will come online over the next two years, indicating that the narrative around fossil fuels is changing. ET is in a prime position to capitalize on the exporting boom which will take place, in addition to the surge in energy demand over the next several decades. ET has the largest pipeline infrastructure in the U.S. and exporting facilities on both the gulf and east coast. Operationally, ET has strengthened its balance sheet while providing 4 consecutive distribution increases, bringing the distribution much closer to its previous levels. If you’re an investor in the energy infrastructure space, ET is yielding over 9% and could be best positioned for capital appreciation in 2023.

Seeking Alpha

In a world where energy demand is increasing, fuels will need to be transported to their final destinations

It’s interesting how perceptions and narratives change. In 2020 and 2021, the narrative focused on renewables and eliminating fossil fuels. After the horrific war in Ukraine started, the world realized how important consistent, reliable energy is and that the idea of eliminating fossil fuels isn’t practical. I am pro-renewable energy, but I am a realist, and the world is not in a position to eliminate fossil fuels over the next 2-3 decades. This premise has been solidified by Europe as billions upon billions are being allocated to increasing capacity for LNG imports in 2023 and 2024. The United States Energy Information Administration is projecting that liquified natural gas (or LNG) terminals across the European Union will expand their capacity by 5.3 billion cubic feet per day (Bcf/d) by the end of 2023. In 2024, this capacity will expand by another 1.5 Bcf/d for a total of 6.8 Bcf/d of new LNG regasification capacity added in the region (34% expansion) compared with 2021. Between January and November 2022, an estimated 1.7 Bcf/d of new and expanded LNG regasification capacity was added in Poland, Italy, the Netherlands, Finland, and Germany. By the end of 2023, LNG regasification terminals that are currently under construction in Germany, Poland, France, Finland, Estonia, Italy, and Greece will add 3.5 Bcf/d of new capacity. If renewables had the ability to replace the use cases for natural gas, Europe wouldn’t be expanding its LNG import capacity so drastically.

EIA

In the 3/3/22 Annual Energy Outlook 2022 report, the EIA projected that in 2050 the USA would be dominated by fossil fuels. The United States is projected to remain a net exporter of total liquids, and a net importer of crude as natural gas and LNG trade reaches 8 trillion cubic feet in 2050.

These are not my projections; they come directly from the U.S. Energy Information Administration. I think the most critical aspect is that the Annual Energy Outlook was released at the bipartisan policy center at a time when all three branches were held by the democratic party, which had been very vocal about their support for renewables over traditional fossil fuels. Putting personal feelings or commentary based on opinions aside, I want to make investment decisions based on the best information. The U.S. government is telling us that their projection is that energy demand will increase and renewables won’t displace oil and gas by 2050. While investing in the oil patch has become unpopular in some circles, the ESG initiatives by others don’t impact my investment thesis. We are being told that the U.S. will be a net exporter of natural gas and LNG, and that the demand for traditional fossil fuels will increase over the next several decades. I want to be invested in midstream operators that can capitalize on growth in this area.

EIA EIA

Why I believe Energy Transfer is going to benefit from the future energy predictions

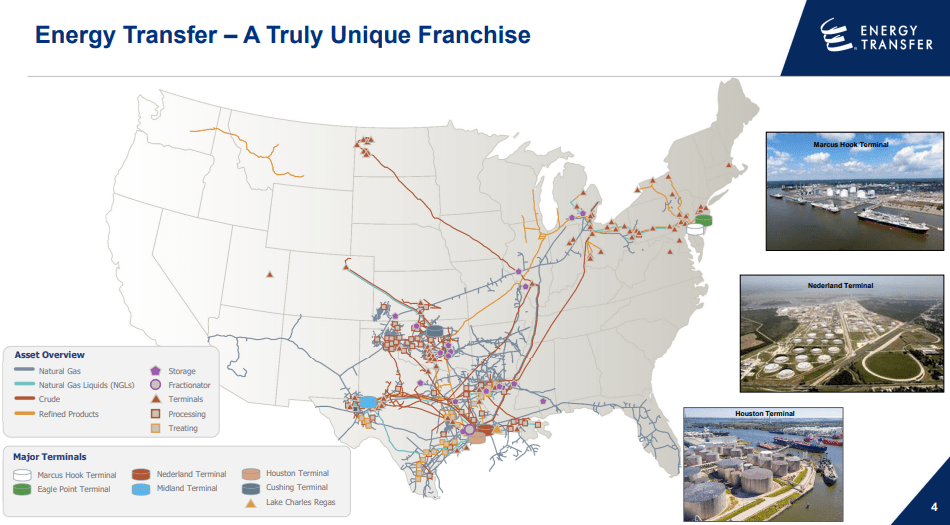

ET is a fully integrated energy infrastructure company from wellhead to water services. ET has the ability to transport 29 million Mmtu/d of natural gas through inter and intrastate pipelines and 4.6 million Bbls/d of crude. ET has the current capacity to export 1.1 million Bbls/d of crude and 1.1 million Bbls/d of NGLs. ET is also positioned to gather 19.1 million Mmbtu/d of gas and 814,000 Bbls/d of NGLs while having the capacity of fractionating 940,000 Bbls/d of NGLs. ET is one of North America’s largest and most diversified energy infrastructure companies, with roughly 120,000 miles of pipeline and associated energy infrastructure across 41 states. ET plays a vital role in transporting 30% of the natural gas and crude moved throughout the U.S. annually. Within its footprint, ET has 11,300 miles of crude trunk and gathering lines, 3,600 miles of refined products pipelines, 53,500 miles of midstream gathering pipelines, 26,900 miles of interstate natural gas pipelines, and 11,600 miles of intrastate pipelines. At the end of the day, it’s next to impossible to replicate ET’s footprint, and the barriers of entry are so immense that external competition, excluding other current midstream operators, is non-existent.

Energy Transfer

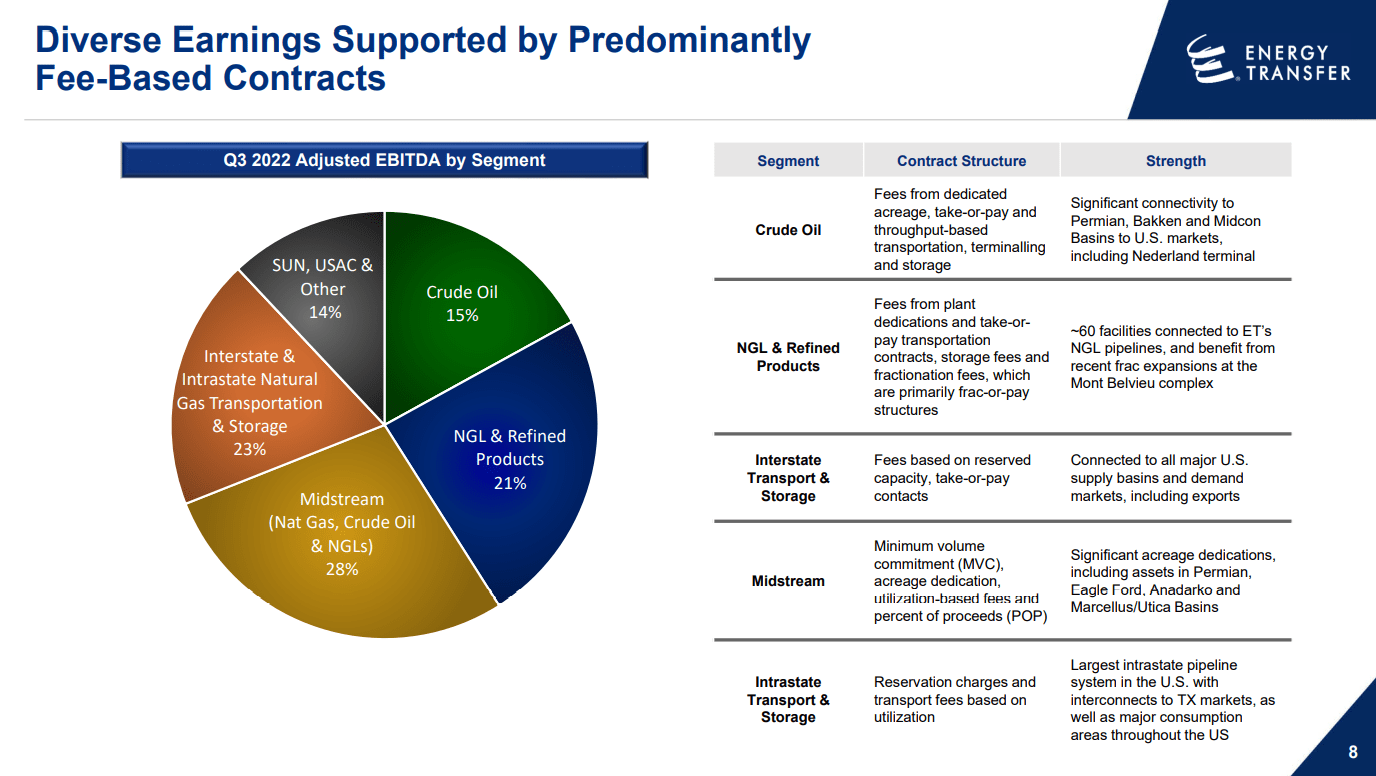

By the end of 2022, ET will have brought 37 different growth projects online. These projects have been a critical component of ET’s $5.5 – $5.7 billion Adjusted EBITDA growth over the previous 5 years. In 2022, ET will have completed Mariner East 2, Ted Collins Link, Cushing South Phase 2, Permian Bridge Phase 2, Grey Wolf Processing Plant, Gulf Run Pipeline, and the Bear Processing Plant. In Q3 of 2022, ET achieved record intrastate natural gas transportation volumes, midstream gathering volumes, ethane exports from Netherlands and Marcus Hook Terminals, and NGL fractionation levels. ET’s diversification also mitigates downside risk as they have exposure throughout the value chain in transporting traditional energy. ET’s is protected by fee-based contracts as 85-90% of its Adjusted EBITDA is generated from transport and storage fees.

Energy Transfer

ET operates a fee-based volume driven company that will benefit from growing transportation needs. As the demand for energy increases it will directly correlate to an increase of production from upstream companies. ET will benefit from additional capacity being contracted throughout its infrastructure as the fuels will need to be transported to their final destinations. There are several interesting midstream operators that I am invested in, but I think ET has the largest opportunity ahead of them. ET has executed 6 long-term LNG SPAs to supply 7.9 million tonnes of LNG per annum and continues to expand its footprint in the major basins domestically. As long as the demand for energy increases, more fuel will travel through ET’s creating additional revenue for ET.

ET still looks undervalued compared to its peer group going into 2023 which could be an opportunity for investors

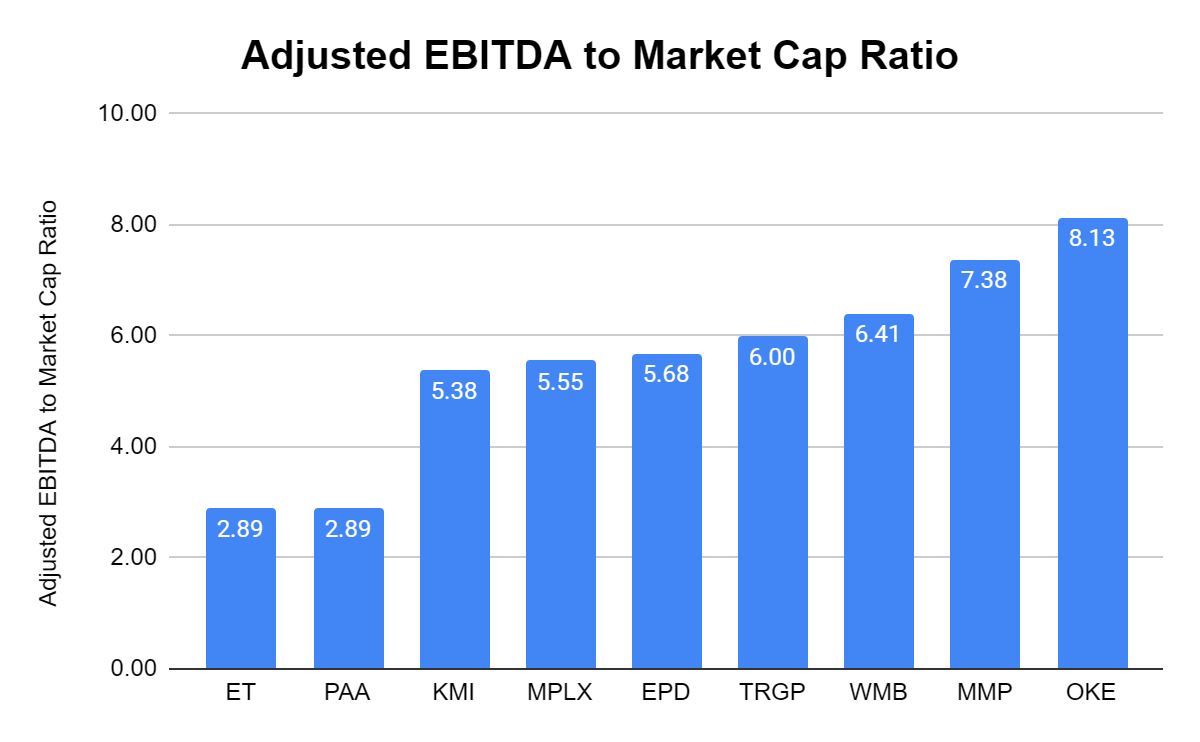

I track the market cap, enterprise value, revenue, Adjusted EBITDA, distributable cash flow ((or DCF)), and total debt so I can compare the following ratios, Adjusted EBITDA to market cap, EV to Adjusted EBITDA, DCF to Market Cap, Debt to Adjusted EBITDA, and Price to Sales. The midstream operators I track are:

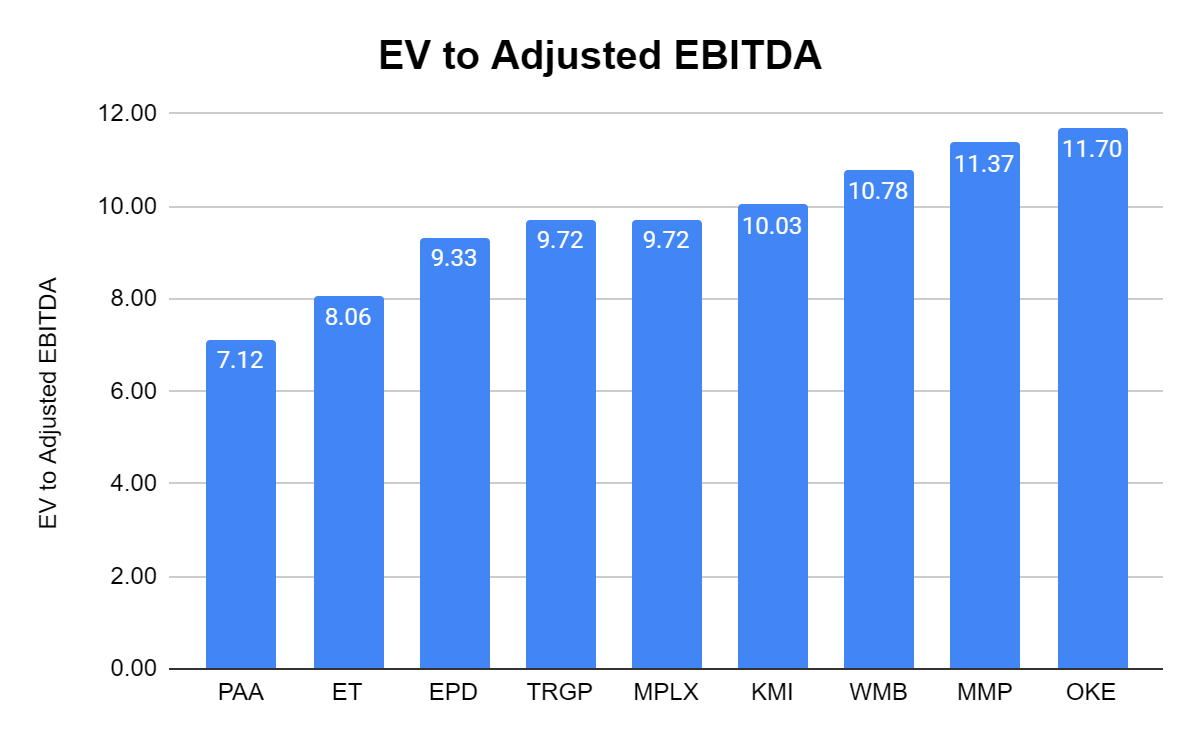

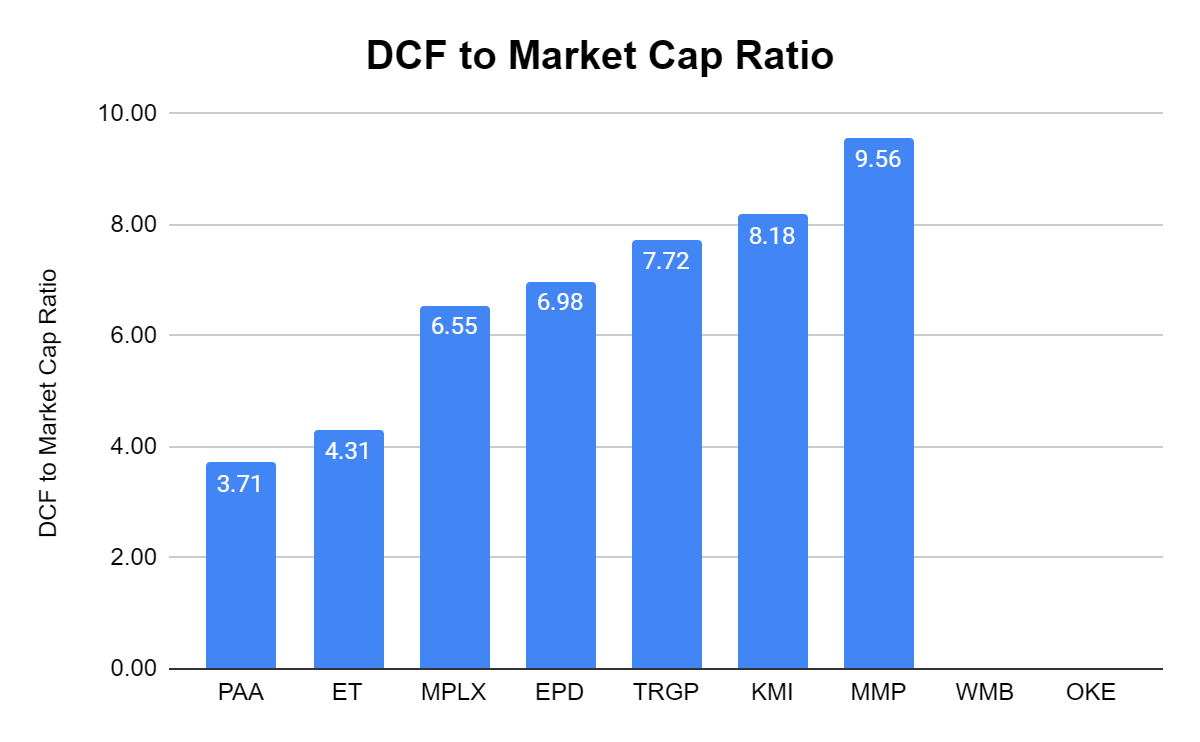

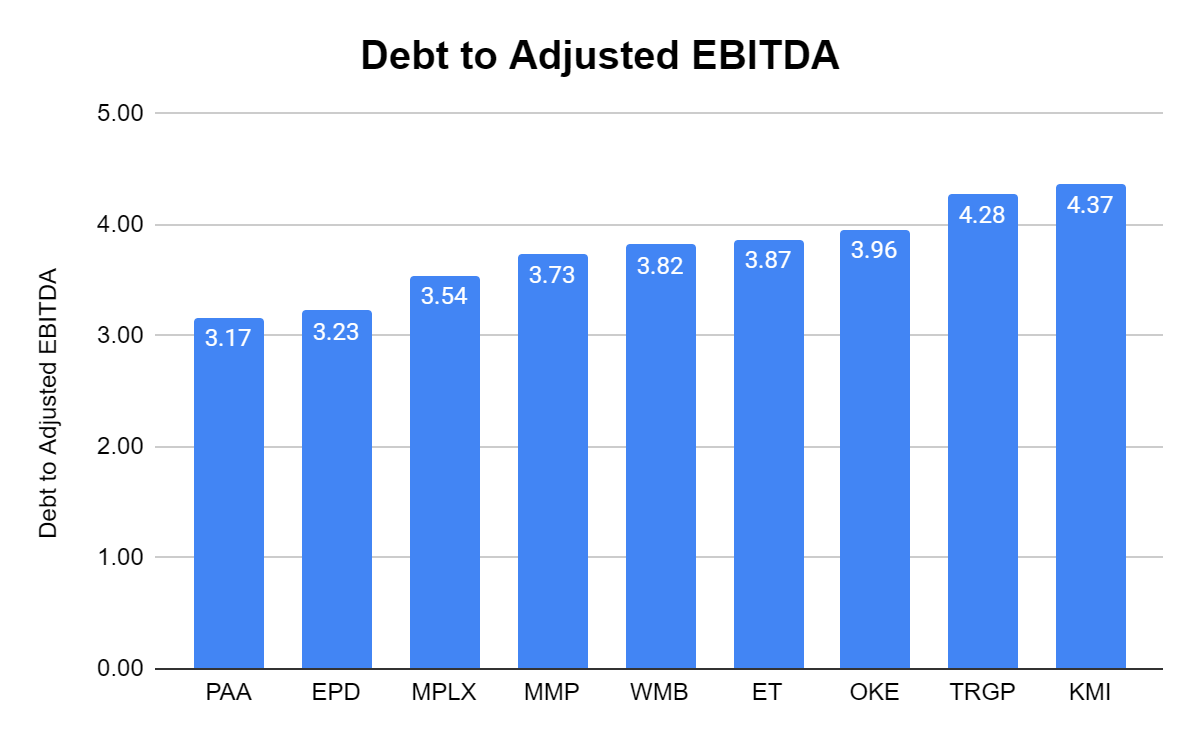

ET trades at an Adjusted EBITDA to Market Cap ratio of 2.89x, which is the 2nd lowest valuation from its peers and significantly lower than the 5.59x peer group average. ET also trades at the 2nd lowest EV to Adjusted EBITDA ratio at 8.06x compared to a 9.76x peer group average. Only 7 of the 9 companies report distributable cash flow, and ET is trading at a 4.31x ratio compared to 6.72x for the peer group average. ET is trading slightly above the debt to Adjusted EBITDA peer group average of 3.77x with a ratio of 3.87x. ET 0.41x for a P/S ratio and is drastically under the peer group average of 1.67x. ET also has the 2nd largest dividend yield at 9.09%. After comparing ET to its peers, it still seems Mr. Market is undervaluing ET.

Steven Fiorillo, Seeking Alpha Steven Fiorillo, Seeking Alpha Steven Fiorillo, Seeking Alpha Steven Fiorillo, Seeking Alpha Steven Fiorillo, Seeking Alpha Steven Fiorillo, Seeking Alpha

Conclusion

Energy led the way in 2022 as it outperformed the market. The EIA is projecting that energy demand will continue to grow and that renewables won’t displace oil and gas. As Europe brings on LNG import capacity in 2023 and 2024, there will be increased pressure for U.S.-based companies to supply our allies with American energy. I am basing my investment premises around the fact that the EIA is telling us that fossil fuel consumption, production, and exports will increase going forward. ET is a likely candidate to benefit as it adds capacity to facilitate the increased volume of fuel being transported and exported throughout the U.S. ET looks to be undervalued compared to its peers. With a dividend yield exceeding 9%, there isn’t much to dislike. I think we will see ET grind higher throughout 2023.

Be the first to comment