Pgiam

Innovative Industrial Properties, Inc. (NYSE:IIPR) never should have traded as low as it did in September, at least that is my opinion. The company’s latest results appeared to validate that opinion, as it continued to grow like a weed (pun intended). There is great fear in the air, but the cannabis real estate landlord is showing that fear is just fear – what matters at the end of the day is that this company is generating cash and paying it out to shareholders. While there remains uncertainty with what will happen with the tenant King’s Garden assets in default, the stock remains deeply undervalued considering the stable cash flows with built-in growth. The cannabis opportunity in the United States remains very promising, and IIPR represents an attractive way to invest in that growth.

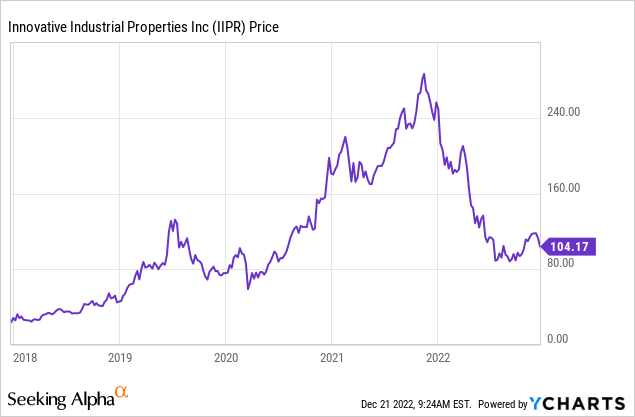

IIPR Stock Price

IIPR has bounced strongly off the lows. The stock had previously dipped to pre-pandemic levels. Consider that funds from operations (“FFO”) per share – an accurate proxy for real estate investment trust (“REIT”) earnings – is up over 150% since 2019.

I last covered IIPR in August, where I rated the stock a buy on account of the 7.6% dividend yield. IIPR has since increased its dividend by 2.9% sequentially and has returned 17% overall. The stock is now yielding around 6.8% – still far too cheap for a name that can sustain rapid growth for years to come.

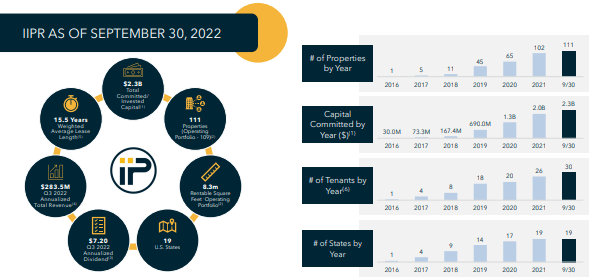

IIPR Stock Key Metrics

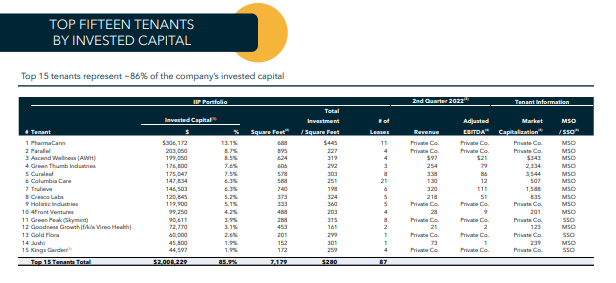

IIPR remains by far the largest publicly traded cannabis REIT in the market today, with a 111 property portfolio.

November Presentation

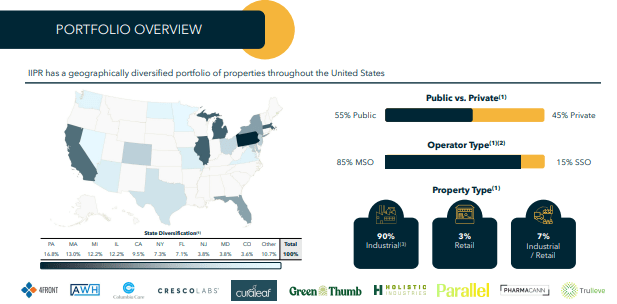

The vast majority of its portfolio are cultivation facilities. 85% of its tenants are multi-state operators (“MSOs”), which is an important distinction because each state has different market dynamics. Many of IIPR’s top tenants are among the most well-known publicly traded MSOs, including Curaleaf (OTCPK:CURLF), Green Thumb Industries (OTCQX:GTBIF), and Trulieve (OTCQX:TCNNF).

November Presentation

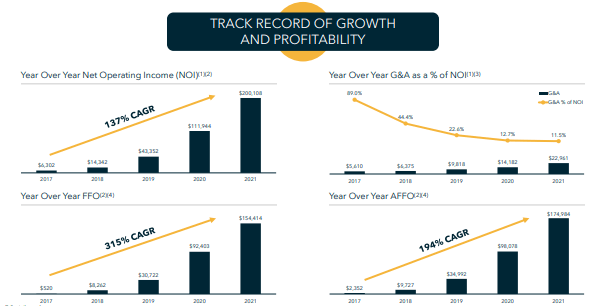

IIPR has rapidly grown cash flows over the past several years, which may surprise some considering that IIPR is a net lease REIT (“NNN REIT”). NNN REITs typically grow in the low single-digit range, yet IIPR has managed to increase FFO at exponential rates.

November Presentation

There are structural reasons behind that above-market growth. IIPR has previously traded at obscene valuations, enabling it to issue equity to acquire properties at highly accretive rates. Because cannabis is illegal on the federal level, cannabis operators have limited access to capital. Whereas Realty Income Corporation (O) is acquiring properties at around a 6% cap rate, IIPR has acquired properties at a 13% cap rate or higher. Whereas O might aim for 1% annual lease escalators, IIPR gets 3% or higher. The elevated yield reflects the higher risk – in particular, cannabis operators may generate weaker cash flows due to the presence of 280e taxes which prevents the write-off of operating expenses from taxable income. Yet in spite of that elevated yield and risk, rent collection has remained very close to 100% over the past many years.

November Presentation

IIPR’s tenant roster is not nearly as diversified as that of traditional NNN REITs, largely because many states employ limited license models which inherently reduces the number of cannabis operators.

November Presentation

On the conference call, management noted that the vast majority of the 3% uncollected rent in the latest quarter was due to their troubled California tenant King’s Garden, which is in default. IIPR had run up heading into earnings due to a settlement with King’s Garden – management noted that pursuant to the settlement agreement they regained possession of two properties that were under development. IIPR has already signed an LOI for one of those properties though the lease is not yet finalized. The other San Bernardino property remains on the market – management notes that it is also exploring non-cannabis uses.

One very positive development was that IIPR sold a Pennsylvania property that it had previously acquired in 2019 for $23.5 million – higher than their cost basis. Pennsylvania has been seeing some pricing pressures – the fact that IIPR was able to dispose of that property at such attractive prices is a clear positive and helps counteract the notion that the company has been overpaying for its assets (a typical bearish claim).

Experienced REIT investors know that rising interest rates tend to hurt REITs due to the potential for cost of capital to rise factor than growth in income. But IIPR has minimal debt on its balance sheet, with the $300 million in outstanding debt representing only 1.1x EBITDA (in contrast, O has debt to EBITDA of above 5x). The minimal leverage means that IIPR faces minimal direct negative impact from rising interest rates but on the contrary benefits from rising acquisition cap rates. Management did note that they have generally “seen an uptick commensurate with the rest of the environment.”

Is IIPR Stock A Buy, Sell, or Hold?

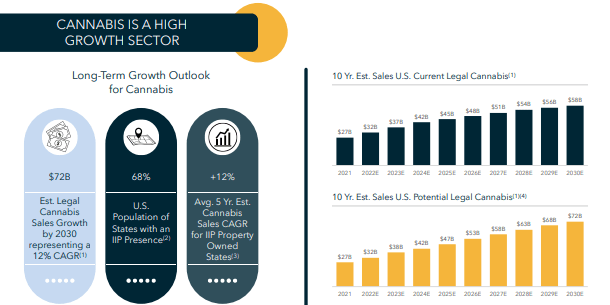

IIPR has grown very rapidly in the past, but I expect it to continue growing rapidly moving forward. Cannabis is one of the fastest-growing sectors in the United States and is expected to grow at a 12% CAGR through 2030.

November Presentation

Those who do not use cannabis might be surprised by that outlook. I personally use cannabis medicinally to treat occasional anxiety and insomnia. I expect cannabis to eventually be embraced like Tylenol or alcohol is in most households. Even in my home state of California, which has legalized adult-use cannabis sales for many years, I often still see a negative stigma associated with the plant. That disconnect represents the significant growth opportunity.

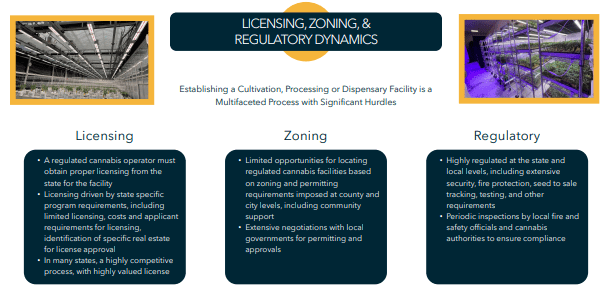

One could make an argument that, over time, pricing pressures and the dilutive effects of 280e taxes make it difficult to invest in the stocks of cannabis operators like the MSOs. IIPR offers an alternative way to invest in the growth opportunity. MSOs need capital to grow – they need to build out cultivation facilities and dispensaries. The equity of MSOs trade very cheaply – and many now have highly leveraged balance sheets. Add on top of that the aforementioned reality that MSOs have limited access to capital, and it is clear that IIPR should see great demand for sale and leaseback transactions. That is evidenced by the fact that IIPR has deployed $370 million to new acquisitions and investments year to date. As a reminder, these net lease properties are secured to the corporate – the tenant cannot just give up the property and walk away. What’s more, perhaps due to the negative stigma of cannabis, even the cultivation facilities are highly regulated – meaning that cultivation facilities often are subject to licensing, zoning, and regulatory restrictions. It is not so simple or feasible for a tenant to simply find a competing cultivation facility elsewhere – this means that upon tenant default, these properties may retain significant value.

November Presentation

Those factors might not be so important for the California King’s Garden assets in default, as California is an unlimited license state. But consider that even if the company were unable to realize any recovery on the King’s Garden assets, those rents made up 8% of overall revenues. Worst case, adjusted funds from operations (“AFFO”) might decline by 9.4% to $7.70 per share annualized. IIPR would still trade at 13.5x AFFO and crucially, the $7.20 annualized dividend payout would still be covered. In reality, I would be shocked if IIPR did not realize at least a 50% recovery on those assets.

Meanwhile, IIPR would still benefit from the 3% annual lease escalators and can continue acquiring new assets at high cap rates. Considering that acquisition cap rates are likely in excess of 13% at this point courtesy of the rising interest rate environment, IIPR could likely continue its acquisition pipeline in spite of depressed equity valuations. I mention that because traditional NNN REITs like O often see minimal growth rates when their stocks trade cheaply. One could make an argument that IIPR should trade at comparable if not higher valuations than O due to the stronger internal and external growth potential. O is currently trading at a 4.7% yield. If IIPR traded at a 5% dividend yield, then the stock would trade at $144 per share – reflecting 38% upside from multiple expansion (45% inclusive of dividends). If IIPR traded at a more reasonable 4% yield, then the stock would trade at $180 per share, reflecting 73% upside from multiple expansion (80% inclusive of dividends).

The main catalyst in my view is continued execution on AFFO and dividend growth, which in turn would also gradually minimize any negative impact from King’s Garden. IIPR would also benefit from a “kitchen sink” event in which it fully resolves the King’s Garden situation – even a full write-down of the asset may be enough to cause investors to move on from fear to focusing on the actual financial impact.

What are the key risks? The most important risk is that of tenant credit quality. Even some of the strongest cannabis operators like CURLF are not generating positive GAAP net income. This is in part due to the presence of 280e taxes, high interest rates on debt, as well as potentially over-stretched footprints. I expect the top MSOs to sustain healthy access to capital – in my bear case the common stockholders of the MSOs may face considerable dilution whereas IIPR continues to collect rent. If the cannabis sector loses favor with investors, then it is possible that there are widespread bankruptcies (it is unclear how that will look like, as technically U.S. cannabis operators do not have bankruptcy under their disposal). IIPR may have to reduce rent payments or write off asset values in such a scenario.

There is also regulatory risk. IIPR is currently able to both list its stock on major exchanges as well as avoid paying 280e taxes due to not directly touching the cannabis plant. But government authorities might change their view on this, leading to IIPR having to trade over the counter (“OTC”) and start paying 280e taxes. The actual impact of these might not be so much – I estimate that 280e taxes might reduce AFFO by 26% – but the stock would undoubtedly get hit in the near term upon such news.

I can see Innovative Industrial Properties, Inc. growing rapidly over the coming years as it meets intense demand for cannabis financing. I rate IIPR a strong buy even after it has bounced strongly off the lows.

Be the first to comment