paparazzit/E+ via Getty Images

Overview:

Energy Transfer (ET) is the largest pipeline/midstream company in the US with over 100,000 miles of pipelines.

Energy Transfer

With operations spanning North America, ET generates large amounts of revenue and cash flow and pays out significant distributions.

Plains All American Pipeline (NASDAQ:PAA) is a smaller midstream company that has had very good results lately. Its operations are mainly in the central part of the USA, including the Permian Basin, and Canada.

PAA

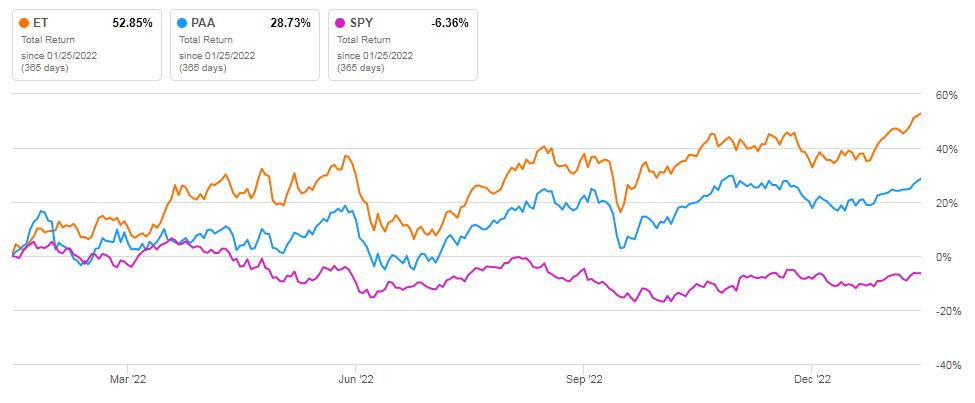

Over the last year, ET has outperformed PAA by 53% to 29% on a Total Return basis (Including dividends) and both have easily outperformed the S&P 500 (SPY) which came in at a negative 6% over the same period.

Seeking Alpha

Both management teams have made some questionable decisions and both have lowered their distributions within the last three years. Just in September Plains agreed to pay a $230 million fine for a California oil spill. In August, ET paid a $10 million fine for problems with its Mariner East Pipeline expansion project.

In this article, I will compare Energy Transfer LP and Plains All American Pipeline LP’s future potential based on several different metrics to determine which midstream company would be the best investment choice at this time.

Note: I use the words distribution and dividend interchangeably.

Financial metrics

When we look at the financial metrics comparing the two companies on a TTM (Trailing Twelve Month) basis, several metrics jump out including the fact that PAA looks very good in comparison to ET.

Seeking Alpha and author

Looking at the orange outlined items, we can see that ET’s price-to-sales ratio (line 3) is more than twice PAA’s. ET’s gross margin (GM) is much higher than PAA’s (line 5) but GM based upon Market Value and Enterprise Value (Lines 8 and 9) are lower than PAA’s and could indicate that either PAA is underpriced or ET is overpriced relative to each other.

Debt/EBITDA (Line 14), Price to FCF (line 16), and the Dividend/distribution rate (line 18) are all in favor of PAA.

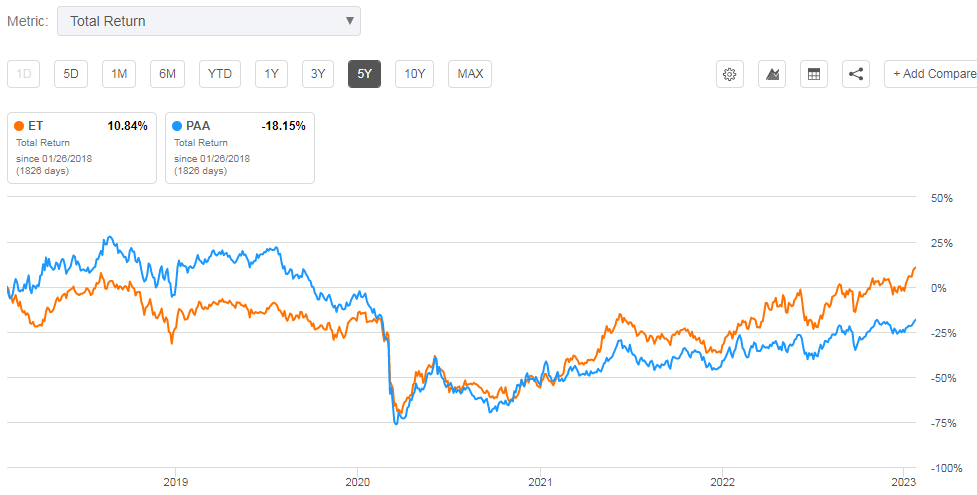

Comparing PAA and ET Total Return over the last five years shows ET has outperformed PAA with a return of 11% compared to minus -18% for PAA.

Seeking Alpha

Overall, on a Financial Metrics basis, PAA looks much more promising than ET which was surprising to me since I have been touting the undervaluation of ET for years.

Analysts’ ratings show both companies are well-liked by the investment community

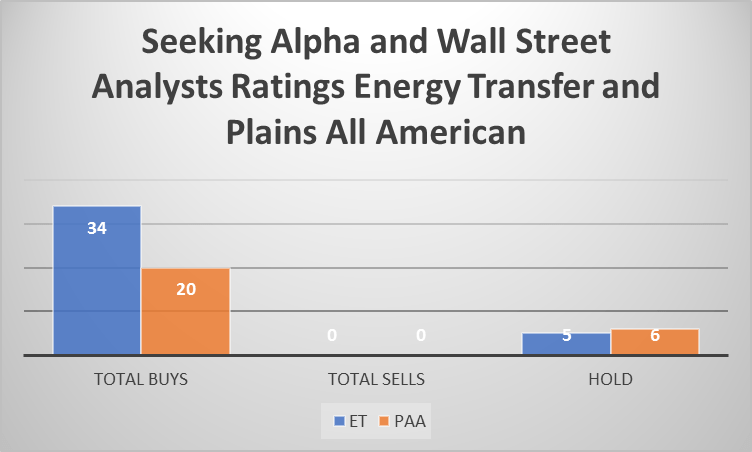

Both Seeking Alpha writers and Wall Street analysts appear to really like these two stocks. The total of 54 Buy recommendations and zero Sells indicate that most analysts think these two stocks have a bright future ahead of them.

Seeking Alpha and author

Interestingly enough, quants are not nearly as excited as the analysts, with a very modest “Hold” call for both stocks although quants did have a Buy rating on ET from May until August 2022.

Seeking Alpha

Seeking Alpha

Do the quants know something that the analysts don’t?

Historical price trends continue to be negative for both companies

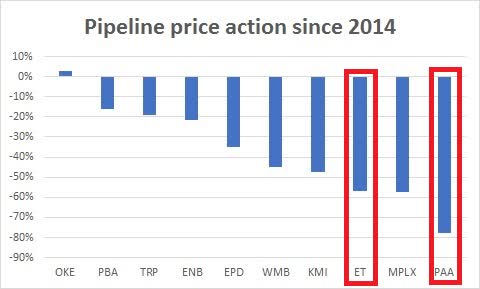

If we look at the prices for major midstream companies from 2014 to the present, we can see a decidedly downward trend.

Author

The carnage is universal, and even a conservative stalwart like ET has seen a crushing decrease in the share price of 57%. But the worst of the bunch is PAA down a breathtaking 78% since 2014.

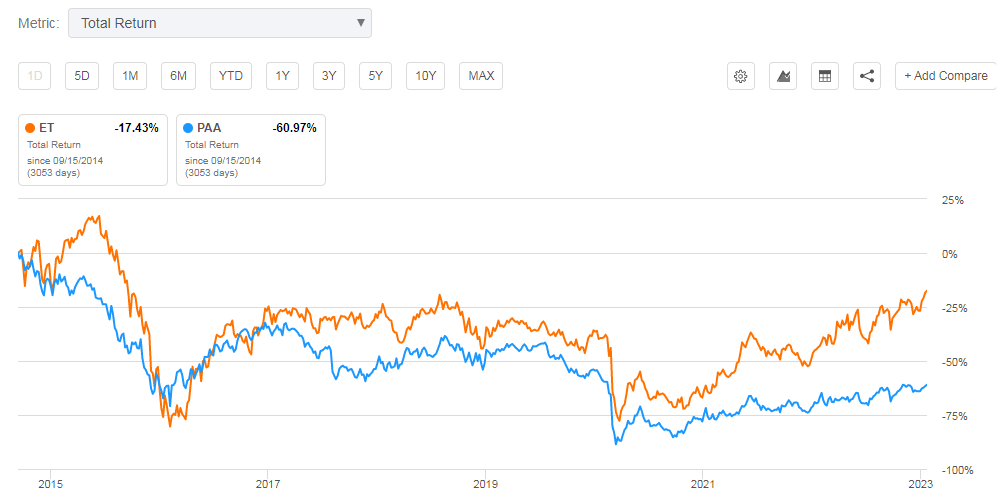

The following chart compares the total return which includes distributions for ET versus PAA since September 15, 2014. It shows that over that extended time period when both stock’s share prices dropped significantly, ET lost 17% while PAA showed a loss of more than 60% for the 8-year period.

Seeking Alpha

Midstream companies in general have struggled to maintain their share price over the last eight years.

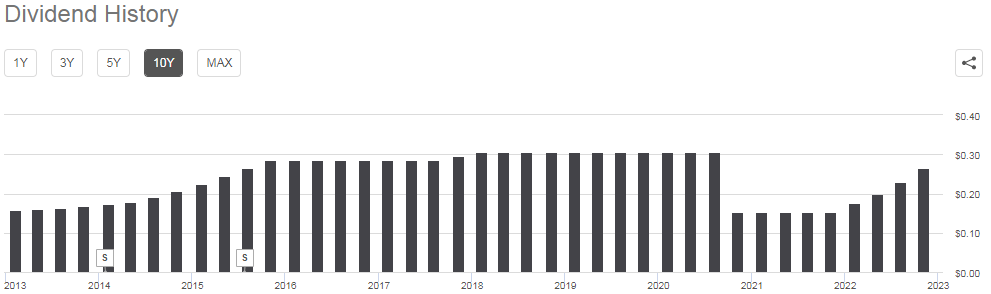

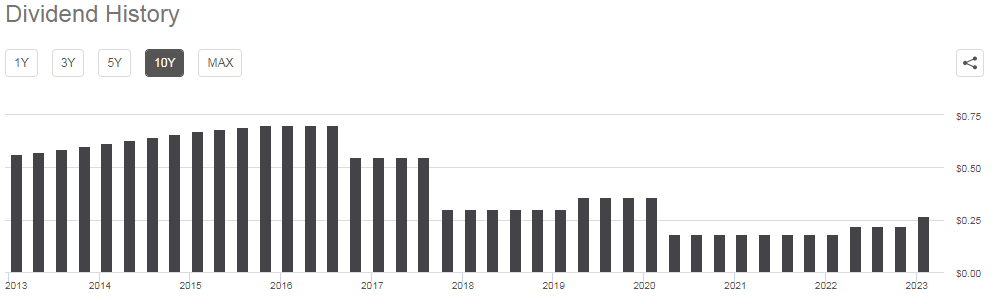

Neither ET’s nor PAA’s dividend distribution record looks good over the last 10 years.

ET cut its distribution in half in 2020, but recently has started to raise it once again with the stated goal to get the distribution back to the 2020 level.

As I write this article, ET has announced another distribution increase to 0.305 per quarter returning the annual amount to $1.22. This restores the distribution/dividend to the same level it was before ET cut it in November 2020.

Seeking Alpha

PAA’s dividend/distribution record has been even worse than ET’s with a series of severe cuts beginning in 2017. However, it has started to raise the distribution once again similar to ET.

Seeking Alpha

So if you are looking for a steady, consistent dividend, neither of these stocks fits the bill.

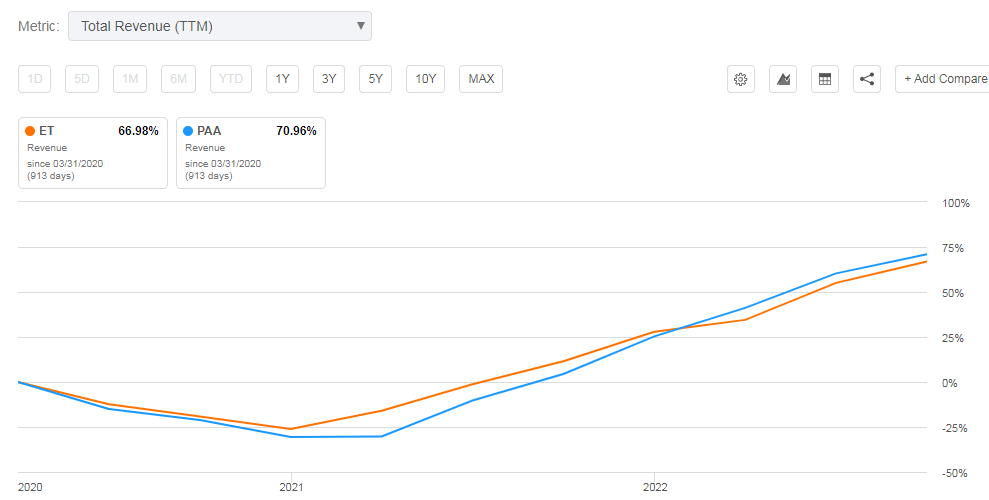

Revenue since the Covid outbreak has increased for both companies

Both companies have benefited from the end of Covid restrictions and from the increase in oil and gas production since the Covid lows of 2020.

Seeking Alpha

Conclusion

Midstream and pipeline companies are not the market’s favorite pick right now and likely won’t be in the future either. ESG and negative political headwinds could plague the market for the foreseeable future.

But that doesn’t mean that there is no potential in any MLPs. In PAA’s case, the steep drop in price over the last eight years gives it a chance for nice capital returns if it just returns to the median price of the midstream/pipeline sector.

PAA has aided that cause by beginning a substantial share buyback program that has reduced its share count by more than 14% over the last three years. ET, on the other hand, has increased its share count as it has used new shares to expand its operations.

Seeking Alpha

ET has been a favorite of mine going back to at least 2020 when I wrote this:

“ET will be a triple if it returns to the previous price of just 18 months agoIn March of last year, ET was at $15.74 just about exactly 3 times 11/03/20 price of $5.21. That shows how much the market has punished the company for its legal imbroglios, including DAPL and others.”

With a current price over $13, ET is rapidly approaching that $15.74 number I quoted more than two years ago. I think that PAA may be in a similar position now in 2023 with a large upside possible.

Based upon the above analysis, PAA is a Strong Buy and ET is a Buy.

Be the first to comment