Oil Pumps And Rig At Sunset By The Sea imaginima

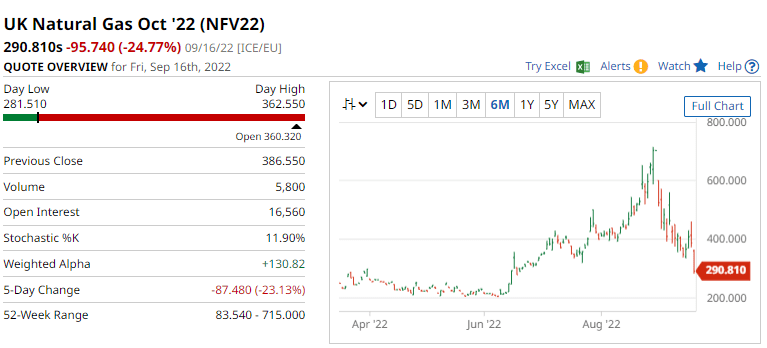

The news feed is full of alarm bells as United Kingdom and European countries begin to feel the impact of their own climate policies manifesting themselves in acute shortages of oil & natural gas. In the United Kingdom, natural gas prices have reached a level equivalent to $500 a barrel oil (the prices in the chart below are pence per therm, one therm is 10.7 Mcf and 6.1 Mcf are the BTU equivalent of 1 barrel of oil).

UK Natural Gas price (ICE/EU)

The Ukraine war has exacerbated the problem for Europe as Russia constrains gas supply in response to sanctions for its invasion of Ukraine. But the Ukraine war is a convenient excuse when the real problem is underinvestment in fossil fuels.

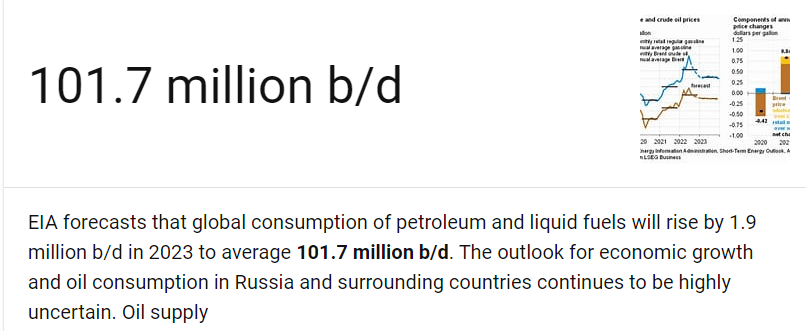

Shortages in Europe have created strong demand for LNG and oil from United States, increasing demand for both oil & gas in that market. Partly as a result, North American oil & gas prices have also risen sharply and oil companies are showing high levels of free cash flow, but after decades of ESG-related attacks on oil companies, those companies have preferred to use their cash flow to pay dividends and buy back stocks. The EIA projects oil demand increasing to 101.7 million barrels a day in 2023.

EIA projection (Energy Information Administration)

In the absence of new supplies, the current shortage can only deepen, and the source of any new supplies comes down to United States and Canada, neither of which show any signs of expanding output. When German Chancellor Scholz asked Canada to expand LNG to supply Europe, Prime Minister Trudeau told him there was no business case to do so. Canadian failure to build pipelines or LNG terminals (beyond one under construction in Kitimat) leaves Canada incapable of providing Europe with LNG, and the Biden Administration continues to promote “clean energy” and withdraw oil from the SPR rather than encourage more domestic production. OPEC has little spare capacity and that source is dry.

Winter is now only three months away and demand for heating oil and natural gas is sure to rise. With natural gas in short supply, oil will be used as a substitute for power generation where that is possible and coal is making a comeback.

For investors, positions in oil & gas stocks should pay off. Debt-free companies with high free cash flow yields offer the lowest risk and likely highest rewards. Birchcliff (OTCPK:BIREF) expects to be debt free by year-end and has announced an intention to pay a CAD$0.80 dividend beginning in 2023. Spartan Delta (OTCPK:DALXF) is fast approaching a debt-free state and is expected to pay dividends once it reaches that goal. Peyto Exploration (OTCPK:PEYUF) has modest debt compared to cash flow and already pays a dividend of CAD$0.05 per month. Whitecap (OTCPK:SPGYF) pays a regular dividend and sports a strong balance sheet.

Of these four, Spartan Delta is the best bet in my opinion. The company acquired the assets of insolvent Bellatrix out of the failure of that company giving it large holdings in the prolific Deep Basin and related infrastructure for pennies on the dollar and completed a subsequent acquisition of privately-held Velvet Energy for a reasonable price. I value Spartan Delta at CAD$35 to CAD$45 a share based on CAD$100 oil (WTI US$75) and $8 natural gas (US$6 Henry Hub), both of which are within the bounds of reason. Clearly, lower commodity prices will hurt but the growing shortage of oil & gas worldwide provides some support for current price levels enduring even with a recession, in my opinion.

These are just four names I think merit investor attention. There are plenty of others and all boats rise in the same tides. This is a good time to hold energy names and the winter should be constructive for many of them.

Be the first to comment