William_Potter

I last covered the iShares MSCI Emerging Markets ex China ETF (NASDAQ:EMXC) in late 2021. In that article, I argued that the Chinese market presented some significant, somewhat unique, risks to foreign investors, including stiffening regulations, a tough economic and political environment, and a broadly unfavorable environment for foreign investors.

Since then, conditions have materially worsened, with Chinese economic growth stalling, the U.S. severely restricting U.S. semiconductor business in China, and with Xi winning a third term, ensuring current policies and trends continue. A possible Chinese invasion of Taiwan looms large, which would almost certainly lead to disastrous economic performance for the country, and for its stock market. Due to these issues, Chinese stocks have underperformed since my previous coverage on EMXC, and could continue to underperform moving forward. EMXC avoids the risky Chinese market, provides strong, diversified exposure to emerging market equities, and is a buy.

EMXC – Emerging Markets ex China ETF

Strategy and Holdings Analysis

EMXC is an emerging markets ex China index ETF. It tracks the MSCI Emerging Markets ex China Index, an index of these same securities. It is a simple, self-explanatory index, investing in most emerging market equities, but specifically excluding Chinese stocks and small-caps. As with most indexes, applicable securities must also meet a basic set of trading, liquidity, etc., inclusion criteria.

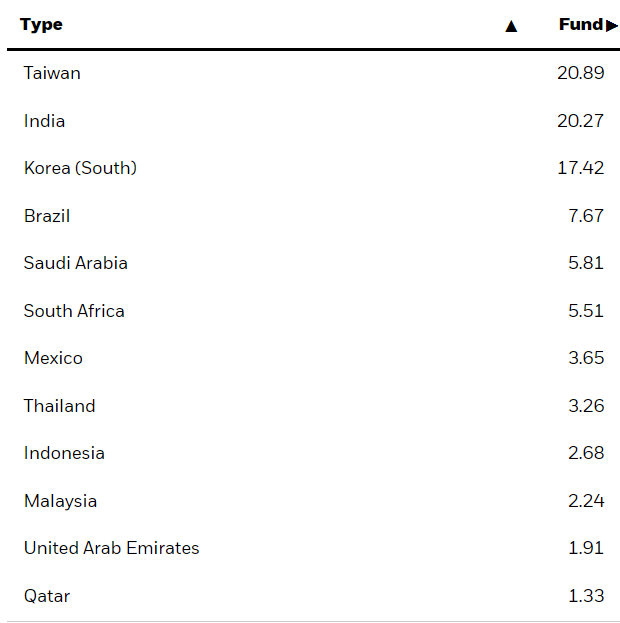

EMXC’s underlying index is quite broad, which results in a well-diversified fund, with investments in over 600 securities from most relevant emerging market countries, sans China. The fund is significantly overweight India, due to the size of the country’s economy, and Taiwan and South Korea, due to the large size of their respective equity markets. Although I would not classify the latter two countries as emerging markets, both are strong economies home to some fantastic companies, including TSM (TSM) and Samsung (OTCPK:SSNLF). As such, their inclusion does not harm the fund or its shareholders in any way, in my opinion at least. Regional allocations are as follows.

EMXC

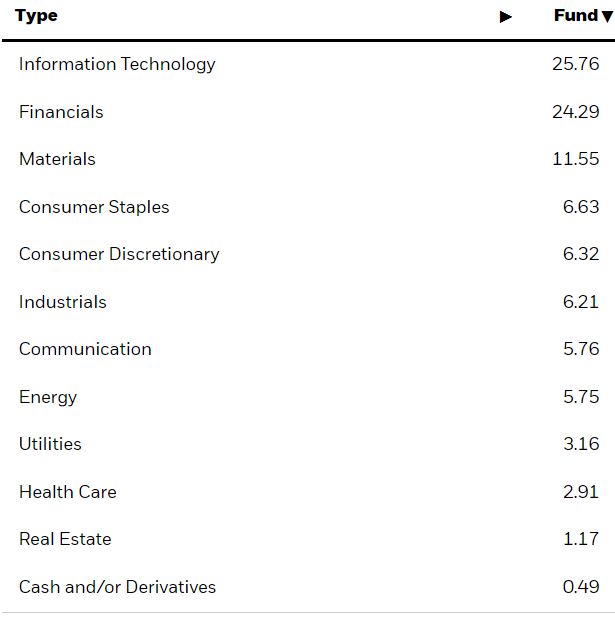

EMXC provides investors with some exposure to all relevant industry segments. Importantly, the fund is not underweight tech, unlike most of its peers, due to significant investments in South Korea and Taiwan, two countries with large, well-developed public tech companies. Industry exposures are as follows.

EMXC

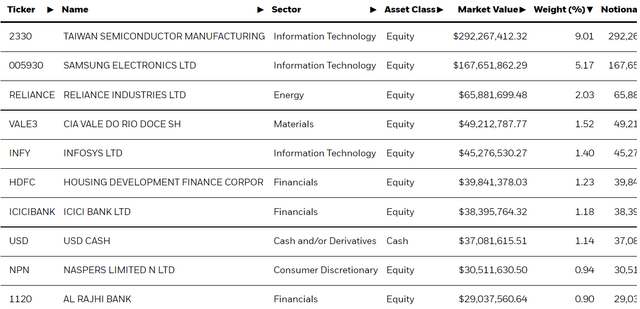

EMXC’s concentration is slightly below-average for an equity index fund, with the fund’s top ten holdings accounting for just 22% of its value. TSM and Samsung are the two largest holdings, by far, accounting for 7.2% and 4.8% of the value of the fund, respectively.

EMXC

EMXC provides investors with diversified exposure to emerging market equities, sans China. These same securities provide investors with several important benefits. Let’s have a look.

Valuation Analysis

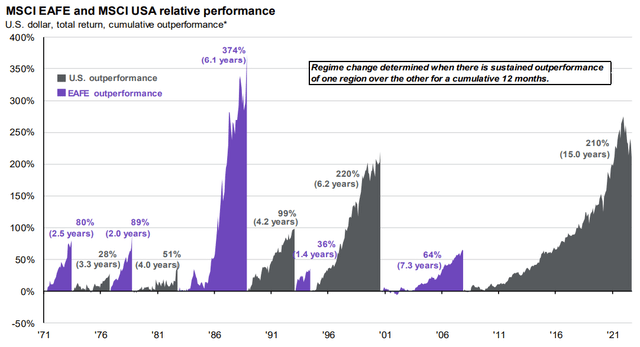

U.S. equities have seen very strong, consistent gains since the aftermath of the financial crisis of 2008-2009. U.S. equity indexes have seen double-digit returns almost every year for more than a decade, with only a few scattered periods of losses, most of which proved short-lived. Strong U.S. equity performance has led these securities to outperform relative to international equities, by over 15 years, and by 210% in total. Outstanding results, but not completely unprecedented.

J.P. Morgan Guide to the Markets

Strong U.S. equity performance has, off course, been a significant benefit for U.S. investors in the past, but is less likely to be beneficial moving forward. Rising U.S. equity share prices have led to higher, more expensive valuations, at least in comparison to international peers. As per J.P. Morgan, international equities sport valuations which are 29% lower than their U.S. counterparties, much lower in absolute terms, and much lower than historically average.

J.P. Morgan Guide to the Markets

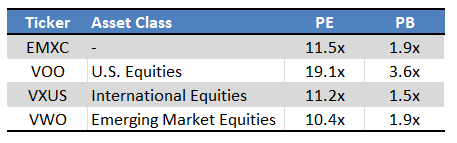

Emerging market equities are a sub-segment of international equities, and are trading with heavily discounted valuations as well. EMXC is no exception, with the fund trading with a relatively low 11.0x PE ratio, and 1.8x PB ratio. Both ratios are significantly lower compared to U.S. equities, but slightly higher than comparable international and emerging market indexes. EMXC trades with a slight premium to these, due to explicitly excluding Chinese equities, which are currently heavily discounted.

Fund Filings – Chart by Author

Cheap valuations sometimes come at the expense of growth, but that is mostly not the case for international equities or EMXC. International countries tend to grow faster than the U.S., and EMXC’s tech holdings, including TSM and Samsung, tend to see strong growth too.

J.P. Morgan Guide to the Markets

EMXC’s cheap valuation could lead to significant capital gains and market-beating returns, contingent on valuations normalizing. Valuations for international equities have refused to budge these past twelve months, even as other disfavored market segments see rising share prices and valuations, including energy and value stocks.

Although EMXC’s cheap valuation could lead to significant gains moving forward, I fail to see a short-term catalyst for the fund, besides economic conditions and market conditions improving.

Dividend Analysis

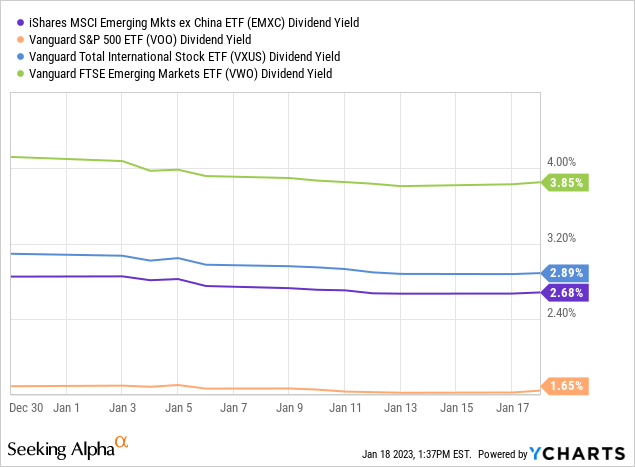

EMXC offers investors a 3.3% dividend yield. It is a relatively low yield on an absolute basis, lower compared to international and emerging market equity yields, but higher relative to U.S. equities.

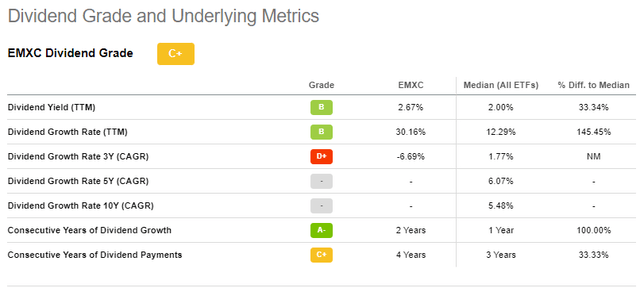

On a more positive note, EMXC’s dividends tend to see very healthy growth year after year, growing at a 13.0% CAGR since inception. Growth is skyrocketing, reaching 30% these past twelve months. As with most ETFs, dividends are fully covered by underlying generation of income, which ensures some degree of dividend sustainability.

SeekingAlpha – Chart by Author

EMXC’s dividend yield is higher than that of comparable U.S. equities, and the fund’s dividends tend to see strong growth. Although these are both benefits for the fund and its shareholders, the fund’s yield remains quite low, making the fund a relatively subpar income vehicle. Valuations and prospective returns are more important, in my opinion at least.

As a final point, EMXC’s dividends are paid in a semi-annual basis, and are quite seasonal: dividends later in the year tend to be higher than earlier ones. Fund dividends mirror emerging market dividend payment trends. EMXC’s seasonal dividends are something of a negative for shareholders, especially those who depend on dividends to make ends meet.

China Risk Analysis

EMXC offers investors diversified exposure to emerging market equities, which currently sport cheap valuations and above-average yields. Although this is a reasonably compelling value proposition, it is also a common one: there are many ETFs with broadly similar holdings and characteristics. These include the Vanguard FTSE Emerging Markets ETF (VWO) and the iShares MSCI Emerging Markets ETF (EEM). What sets EMXC apart from its peers is the fund’s explicit exclusion of Chinese stocks. Said exclusion serves to limit risk for several reasons, centered on economic, political, and regulatory actions and events.

Economy-wise, the Chinese economy is suffering from a deflating housing bubble, and it’s a massive one. Chinese housing construction accounts for between 20% and 30% of the country’s GDP, significantly higher than average, and higher than the U.S., Ireland, and Spain during their respective housing bubbles. The Chinese property sector is deflating, with housing prices seeing slow, but steady, declines, and developers significantly scaling back construction projects. These issues are slowing down the country’s economy, and have led to billions in losses / defaults for foreign investors. Risks remain, making Chinese securities risky investments.

The Chinese government has also embarked on an aggressive, far-reaching set of economic reforms, meant to shift the country’s economy towards self-sufficiency and real assets and industries, and away from software, consumer apps, and international markets. From what I’ve seen, most of these reforms occurred in prior months, but their impact remains. Reforms include restricting online gaming for children and teenagers, stiffening labor protections for gig workers, and making it more difficult for some tech companies to IPO in foreign markets. Which brings me to my next point.

The biggest issue with investing in Chinese stocks as a foreign investor is the fact that it is somewhere between impossible and illegal to do so. In most cases, foreign investors can’t actually invest in mainland Chinese stocks. Foreign investors can invest in offshore shell companies with complicated contractual arrangements, whose sole purpose is to, well, allow foreign investors access to these securities. These offshore companies and arrangements are of questionable legality. Matt Levine has a fantastic, more in-depth explanation of these issues here, but this is the gist of it.

Investing in offshore shell companies is incredibly risky, doubly so when there are very significant regulatory and legal issues in doing so. Investors should expect incredibly flimsy investor protections, putting their investments in significant risk.

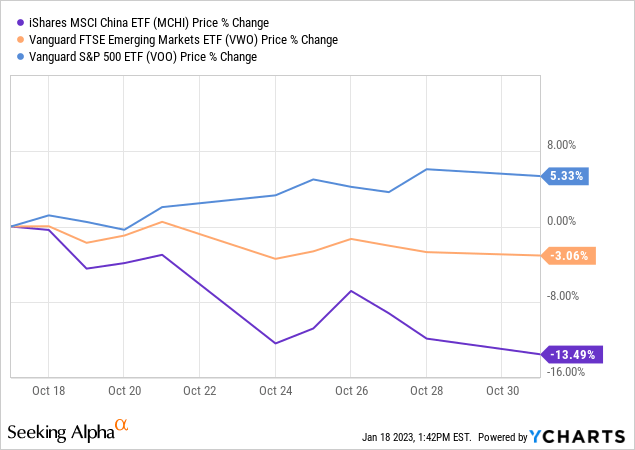

The issues above are compounded by Xi securing a third term. Perhaps another leader would have pivoted from these policies, but Xi was responsible for most, and seems unlikely to change track. The market seems to agree, with Chinese equities plunging after Xi’s third term was a done deal / was announced.

In my opinion, although these risks are not existential, they are very significant, and make Chinese securities unwise investments. Reducing / minimizing Chinese exposure seems wise. Some investors might wish to completely avoid China. EMXC provides these investors a simple way to investing in emerging market equities excluding China, which might be an attractive investment proposition.

Conclusion

EMXC provides investors with diversified exposure to cheap emerging market equities, excluding risky Chinese investments. This is a compelling value proposition, and makes the fund a buy.

Be the first to comment