Phiwath Jittamas

Elme Communities (NYSE:ELME) provides renters with an affordable multifamily rental option. Its proposition to investors may be a harder sell.

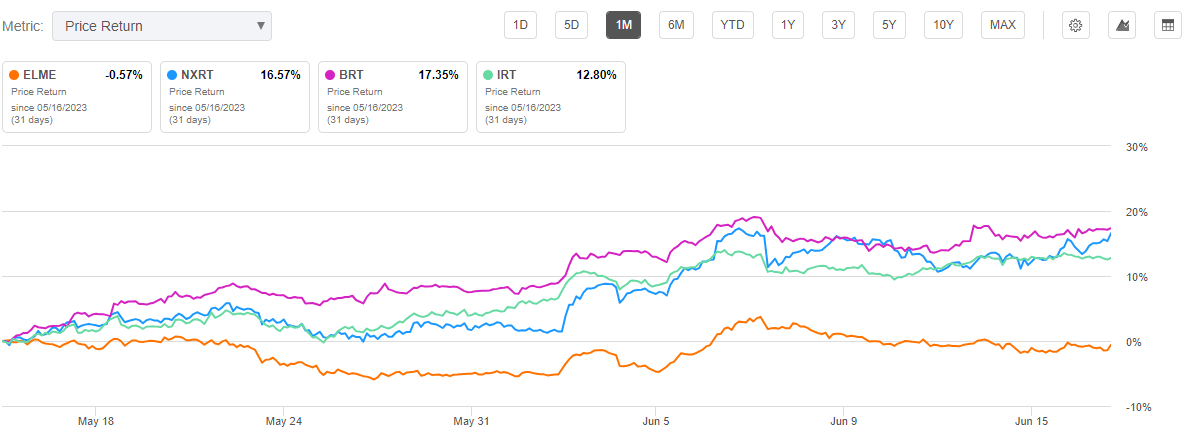

Over the past month, shares are roughly flat compared to double-digit gains by some of their multifamily peers. This follows negative returns over the past year of over 25%.

Seeking Alpha – 1-MTH Returns Of ELME Compared To Peers

Despite the underperformance, shares continue to trade at a premium. This can be attributable in part to a strong presence in more supply-restricted operating regions and a more attractive debt profile. But their operating performance is mixed. Recently announced initiatives pertaining to their transformation efforts are also expected to take time to yield results. With the market likely beyond its peak, this may prove longer than desired. At current trading levels, I view shares best left on hold.

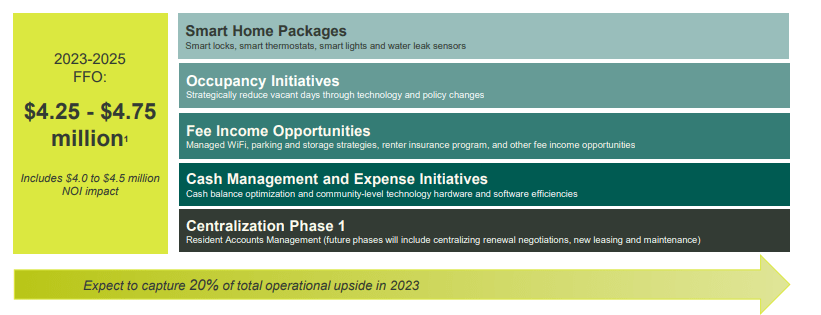

How Does ELME Expect To Grow FFO?

In their Q1 earnings release, CFO, Steven Freishtat, elaborated on a set of initiatives which are expected to generate incremental growth in funds from operations (“FFO”) of +$4.25M to +$4.75M from 2023 to 2025 or approximately $0.05/share.

June 2023 Investor Presentation – Summary Of Growth Initiatives

One of the more promising initiatives is their investment in smart home technologies. This includes smart locks, thermostats, lights, etc. This is viewed to provide the best return for their price point. Past studies support this view.

Do Investments In Smart Home Features Provide Attractive Returns?

In one survey conducted by property solution firm, Entrata, most respondents said they were willing to increase their monthly rent payment to have more technology in their apartments. Furthermore, more than 75% said they would pay more in rent for their top three smart home amenities.

By demographic, more than 55% of millennial renters said they would pay more for additions that increase convenience and add security, such as high-tech door locks. On average, they were willing to pay 20% more for their units with smart home features.

Extended to the population at large and to homebuyers, more than 65% of U.S. homebuyers have said they are willing to pay more for a home with smart features, with 81% saying that smart home features are their most desired feature in new home construction.

While some may counter that most renters aren’t in a position to pay more for features that, arguably, are unnecessary, it’s worth noting that 97% of ELME’s homes are affordable to households earning the area median income (“AMI”). In addition, on average, their residents save approximately $500/month by living in one of their units as opposed to a nearby new Class A community. There is some runway, then, for a bump up in rents.

Installation of these technologies has also been shown to improve tenant turnover. This hasn’t been an issue for ELME. But it can give them an additional leg up in relation to their peers. In Q1, retention averaged about 65%. This is above their historical average in the mid-50% range. Peer, Independence Realty Trust (IRT), on the other hand, reported retention of 48.2% in Q1, with an uptick to 56.7% through the date of their release in Q2. Others, such as BRT Apartments (BRT) have reported similar retention levels in the 50% range.

How Is ELME Performing On Existing Projects?

Though the investments will appear to have topline benefits, could ELME complete them at an attractive going-in cost? On this, it’s less certain. In Q1, ELME reported a YTD average return on investment (“ROI”) on renovations of 13.5%. Both IRT and NexPoint Residential (NXRT) are hauling in 20% ROIs on their jobs. BRT is shining even higher with reported returns of more than 40%. ELME’s performance looks weak in comparison.

ELME also has a smaller overall pipeline of units to be renovated. Most recently, it was about 3K units. IRT’s pipeline is over 6x as large, at 19K. Granted, they have nearly 4x as many overall homes. But ELME’s pipeline still appears underwhelming.

What Is The Upside Potential Of ELME’s Other Initiatives?

The investment in the smart packages figures to result in the most upside. So it warrants extra attention. Their other initiatives pertaining to occupancy, fee income opportunities, and cash management could provide some additional benefit. But it’s not significant enough to get excited about.

Cash management, for example; here, the initiative enables them to access their rent payments earlier, which in-turn facilitates a quicker reallocation of cash to other priorities, such as the paydown of their revolver. But ELME already carries a lower load in relation to peers. The upside resulting from interest savings, then, is seen as limited.

Is ELME Stock A Buy, Sell, Or Hold?

ELME’s recent transformation and current initiatives are viewed by their team to have the potential to provide above-market NOI and FFO growth. The timetable, however, stretches into 2025. That’s too long, in my view. Recent data from Zillow’s observed asking rents and from the monthly CPI report indicate that rental rate growth is past its peak.

Compared to their value-add peers, whose operations are more concentrated in the Sunbelt, ELME benefits from more favorable supply dynamics in the Washington Metro. This is one barrier working in ELME’s favor.

But it’s tough to justify a premium trading valuation for this alone. For the full 2023 fiscal year, ELME is expecting same-store NOI growth of 9.75% at the midpoint. That’s lower than the 11% growth that NXRT is expecting. And NXRT commands a 15.3x forward FFO versus ELME’s 16x. ELME is tracking for double-digit growth in core FFO. That edges out their peer set. But they carry a much lower debt burden, which is a driving factor.

I’d prefer to see the outperformance at the property level. And ELME’s properties haven’t yet displayed that outperformance. ROIs on their projects are lower and occupancy rates run in-line. They have an advantage in retention, which should grow further upon completion of their initiatives pertaining to smart technologies. But whether this comes at attractive returns remains to be seen.

ELME’s properties are an easy sell to renters looking for an affordable multifamily unit. The same, unfortunately, cannot be said of their share price.

Be the first to comment