Delmaine Donson

Elastic (NYSE:ESTC) is a $5.5bn market cap enterprise search, security and observability software provider. The company has recently attracted my attention as a potential acquisition target given a number of interesting aspects. Among them are M&A dynamics in the technology sector, the company’s depressed share price (-53% since Jan’22) and a rather undervalued business. Moreover, ESTC’s management might be incentivized to facilitate/support a potential takeover. While the investment thesis is quite speculative, these points have led me to believe that Elastic might be an attractive takeover target and potentially acquired at a premium to current prices.

First of all, a potential acquisition by a financial buyer might be likely given M&A trends in the technology space. Impacted by the macroeconomic slowdown and tightening monetary policy, the entire technology sector company valuations have shrunk materially, with a 30% drop in 2022 (compared to 20% for the general market). For reference, technology companies from the S&P 500 have shed $3.8T in value over the last 12 months. Not surprisingly, in light of rapidly declining valuations in the sector, PE firms have been opportunistically scooping up beaten-down tech companies. Given increasing piles of dry powder that PE companies have been sitting on, private equity player involvement in the technology, media and telecommunications space has grown markedly compared to pre-pandemic levels (see chart below). This trend has been particularly visible in the software sector given the target companies’ predictable/recurring revenues, high margins and strong cash conversion.

Global M&A Trends in Technology, Media and Telecommunications: 2023 Outlook (PWC)

For instance, PE giant Thoma Bravo has been one of the most active acquirers, buying a number of software companies, including Coupa Software (COUP, $8bn transaction), ForgeRock (FORG, $2.3bn), Ping Identity ($2.8bn) and Anaplan ($10.4bn). Meanwhile, another large PE firm Vista Equity Partners acquired KnowBe4 (KNBE, $4.6bn), Avalara ($8.4bn) and Duck Creek (DCT, $2.6bn). In this context, Elastic fits the PE playbook quite nicely. The company’s share price is down 53% since January ’22 and 69% since November ’21 highs. Meanwhile, over 90% of ESTC’s revenues are recurring while the company boasts 70%+ gross margins and has a solid balance sheet ($292m in net cash). Moreover, there is zero possibility of strategic players – which EY and Norton Rose Fulbright expect to be more active acquirers this year – showing their interest in a transaction involving ESTC.

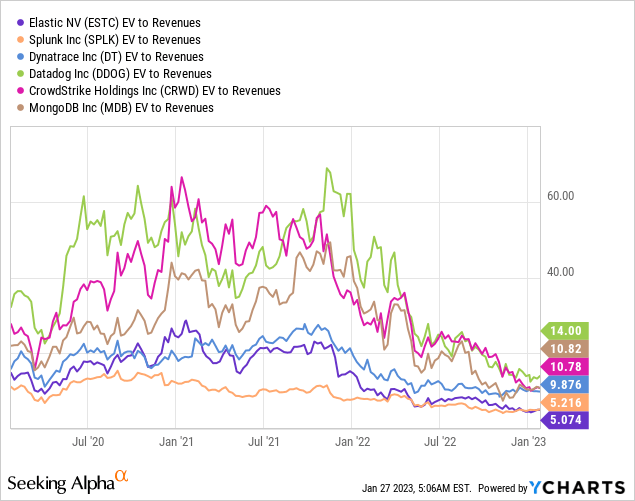

Valuation suggests there might be substantial upside here in case of a company sale. Elastic is currently valued at the historically low 5.1x EV/Revenues multiple. This compares to 8x-26x multiple fetched during 2019-2021. Likewise, the company seems cheap on a relative valuation basis. Similar gross margin and growth peers – which Elastic explicitly mentions as its main competitors – are currently trading at noticeably higher multiples, including Dynatrace (DT) (10x), Datadog (DDOG) (14x), CrowdStrike (CRWD) (11x), and MongoDB (MDB) (11x). Another competitor Splunk (SPLK) currently fetches a similar multiple to ESTC (5.2x), however, the peer has in recent years been growing at a significantly lower clip. Worth noting that direct comparison to peers is somewhat complicated given that each of these competitors operates across different software segments – enterprise search, security and observability. Having said that, at least directionally, Elastic seems to be undervalued and might thus warrant a sizable premium in a transaction.

YCharts

Interestingly enough, it seems that ESC’s management might potentially be willing sellers here. The company’s leadership has a sizable stake in the business of 19%. Another interesting aspect is that, a couple of months ago, ESTC amended its Change in Control and Severance Agreement. Most notably, the company has modified the definition of the “good reason”. This would allow easier accelerated vesting of the CEO, CFO and General Counsel’s equity grants in a potential company sale. Currently, ESTC has granted 627k equity incentive award units to these insiders. This would translate to $36m in total equity awards at the current share price, assuming full vesting. While it is not clear how much of these RSUs and option grants would vest in a potential merger, a potential buyout would nevertheless allow these insiders to pocket sizable bonuses.

Elastic

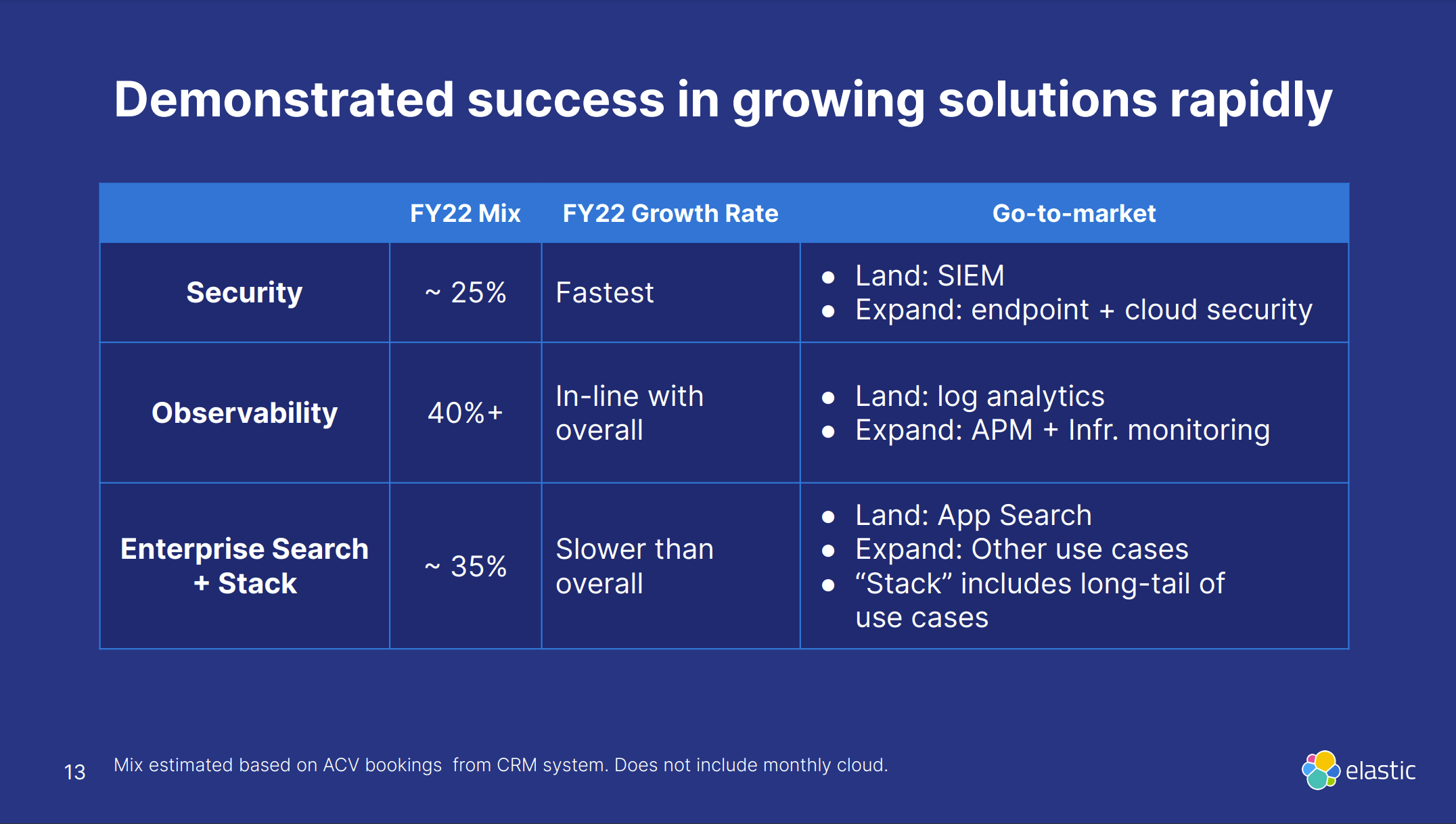

Elastic provides enterprise software with a focus on enterprise search (35% of revenues), security (25%) and observability (40%) software. The company’s core product Elasticsearch provides search software to enterprises, such as Workday, allowing them to organize search results and perform other related tasks. In recent years, ESTC has expanded its offering base from the core enterprise search software into the areas of security and observability. ESTC’s software is open-source, which drives high community involvement (e.g., bug fixes) as well as high visibility into emerging projects on the platform. The software is offered through both major cloud providers (AWS, Google Cloud, and Microsoft Azure) and as a proprietary self-managed software.

Elastic Investor Presentation, January 2023

A potential transaction would come at quite an opportunistic time from an operational perspective. Driven by the macroeconomic slowdown, FX headwinds, and ESTC’s significant exposure to Europe, the company’s financial performance has been impacted, particularly in the higher-margin small and medium-sized business customer segment. ESTC’s revenue growth has slowed down quite markedly to 28-30% year-over-year in the recent quarters – down from 42-81% growth displayed since 2018. Management has guided for 24% sales expansion in FY2023 (ends April) – lower than 26% projected back in June ’22. In response to macroeconomic headwinds, in November ’22 ESTC initiated a strategic turnaround. As part of the strategic shift, management has decided to lay off 13% of the workforce.

Having said that, despite short- and medium-term difficulties, the business seems to have good operational prospects and a substantial growth runway. The TAM – which the company has estimated at $88bn – is still underpenetrated, particularly in ESTC’s core enterprise search segment. Moreover, the company has put an increasing focus on revenues from cloud-based offerings, which have already expanded from 17% in FY2019 to 39% as of Q2’FY23 (ends April). For reference, the cloud business has grown at 50% year-over-year in the latest quarter compared to 14% for self-managed offerings. Management has highlighted that the fast growth of the cloud software segment has been/is expected to be driven by continuing customer migration from on-premise offerings as well as expanding partnerships with AWS, Microsoft Azure, and Google Cloud. Moreover, growth of the enterprise segment sales – accounting for the majority of revenues – has thus far barely budged despite decreasing customer budgets. For illustration, number of customers with over $1m in annual contract value (ACV) grew 53% in FY22.

Competitive Landscape

Elastic’s main competitors in each of the three business segments are provided below:

- In the enterprise search segment, ESTC competes against Solr (private), Lucidworks Fusion (private), and Coveo.

- In the observability segment, the main peers are Splunk, New Relic (NEWR), Dynatrace, DataDog, and App Dynamics (owned by Oracle).

- Main comps in security space are Splunk, Azure Sentinel (owned by Microsoft), CrowdStrike, Carbon Black (owned by VMware), and Symantec (owned by Broadcom).

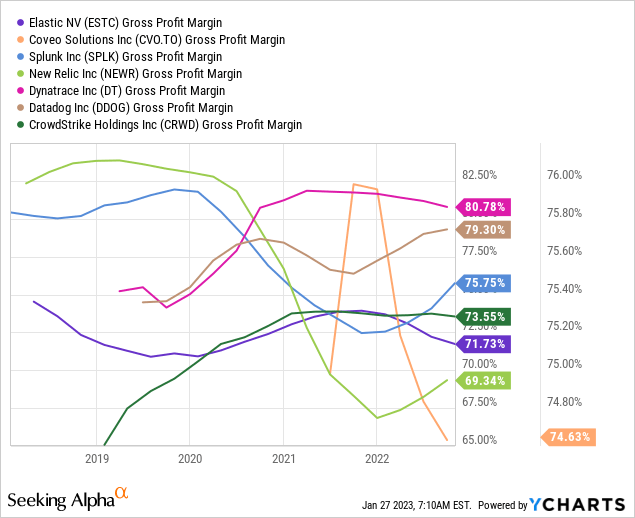

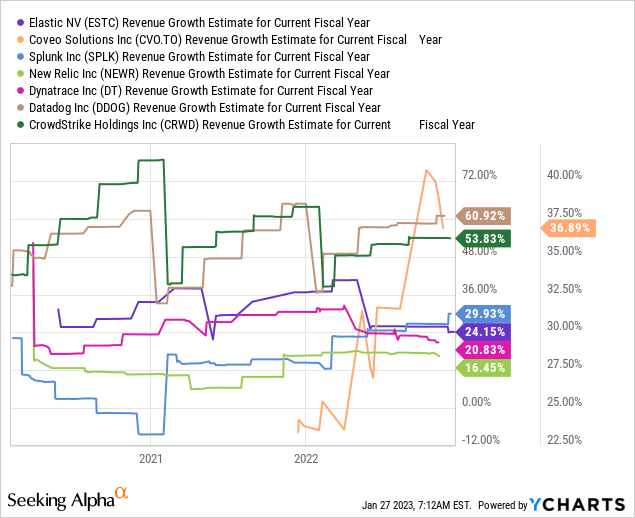

Graphs below illustrate the growth rate and gross margins of Elastic and its publicly-listed competitors.

YCharts YCharts

Elastic’s Competitive Advantages

A couple of points suggest ESTC might either command a premium or be valued in line with its competitors. Firstly, ESTC has been the industry leader in the enterprise search segment, offering the most popular enterprise search tool globally. From the company’s founder/CTO:

In Enterprise Search, I’m talking to customers, I’m seeing the competition that we have, I get a chance to experience their product. In Enterprise Search, we have been leading the pack, and I don’t see in the next few years how others are going to be able to come over and be able to lead the Enterprise Search space. We have probably the most popular search engine in the world today in Elasticsearch, and through that, we enable enterprise search capabilities to our customers that are far and above beyond what anybody else can provide. And we’re not slowing down irrigation as you see it with vector search capabilities, machine learning, this is like significant advancements that we have and a market position.

Secondly, the company’s other competitive advantage versus peers – particularly in the currently deteriorating macroeconomic environment – has been bundled search/observability/security offerings. As noted by Elastic’s CFO:

I think you’re spot on that when people fundamentally think about the idea, particularly in this environment that people are looking — no longer looking for best of breed in everything, but they’re looking for the best of suite or the best platform and the fact that we have a unified platform in which you can bring data from multiple sources for multiple solutions, that’s always been one of our core competitive strengths.

Finally, Elastic is apparently one of the few vendors offering both observability and SIEM (security information and event management) solutions.

Risks

One of the risks here is that Elastic’s management earns very sizable salaries. For reference, the CEO and CFO pocketed a combined $27m in total compensation in FY2022. This suggests the management might wish to retain their positions rather than support a company sale. However, given the recent control/severance agreement amendment, I do not think management would be fundamentally unwilling to support a potential merger.

Conclusion

Given a number of interesting aspects, including M&A dynamics in the technology sector, ESTC’s rather undervalued business, and management incentives, a company sale might be brewing here. In line with other recent technology sector transactions, I would expect a potential acquisition to be announced at a premium to current price levels.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment