Ethan Miller/Getty Images News

Investment thesis

EHang (NASDAQ:EH) has made concrete progress in obtaining certification from the Chinese Aviation Administration of China. The time taken to date has been longer than expected, and risks remain over delays. However, given we are now relatively close to a positive outcome, we reiterate our buy rating.

Quick primer

EHang is a Chinese urban air mobility (“UAM”) company developing and pioneering the use of passenger drones. It has the support of the Chinese Aviation Administration of China (CAAC), the aviation authority of the People’s Republic of China. A working group to progress certification of the EH216 model passenger drone was formed by the CAAC in April 2021, and in December 2022 entered into the final phase of Demonstration and Verification of Compliance after all the certification plans were officially approved by CAAC (page 1). Peers include Joby Aviation (JOBY), Lilium (LILM), Archer Aviation (ACHR), and Blade Air Mobility (BLDE).

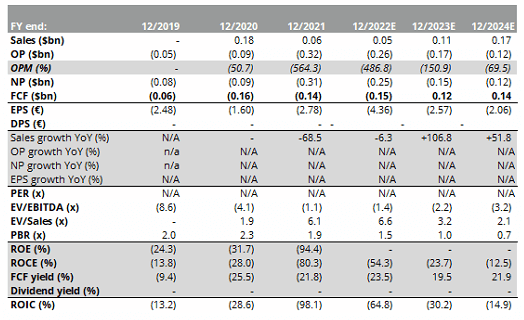

Key financials with consensus earnings estimates

Key financials with consensus earnings estimates (Company, Refinitiv)

Our objectives

We want to update our view from May 2021 where we rated the shares as a buy (the original rating is here from December 2020). We want to assess whether the core argument – state-sponsored activity resulting in certification for commercial operations – remains intact.

View from an official perspective

Management is keen to stress that as a world-first initiative, obtaining any type of official certification will and is indeed taking time. However, after more than 6,800 test flights and with 15 operational sites primarily on the mainland (page 5), EHang is closer than ever to becoming the global first AAV (autonomous automotive vehicle) manufacturer and flight operator. Interest has consistently grown around the world, and there are now 1,200 plus unfulfilled unit orders for the flagship E216 series, as well as some for the long-range VT-30.

Crucially, there is no official timeline as to when certification will be issued, although ‘around January’ (assuming 2023 here but no year stated) was mentioned in the Q3 FY12/2022 conference call. At this current juncture, the company has reached the final stage before becoming officially able to sell and operate its AAVs.

View from our perspective

Over 2 years have passed since our original piece. The shares initially screamed up over 500%, and then experienced a 96% drawdown before rising over 300% from its historic low in October 2022. The shares were targeted (successfully) by Wolfpack Research, and arguably obtaining certification is taking much longer than market expectations. At the very least the shares should come with a health warning!

Our core thesis remains unchanged; EHang’s outlook is dependent on obtaining certification from China’s aviation authority, and progress is being made. The counterargument here is that with the opaque process in place for EHang to become a commercial venture, regulatory risk is very high. However, given the lack of competition in the domestic market, EHang’s position as China’s poster boy for passenger-grade AAVs appears to remain in place.

Although we cannot confirm EHang’s customer orders or any timeline on delivery, consensus forecasts (see table above in Key financials) indicate that sales volume will increase considerably in FY12/2023 (over 100% growth YoY). We have no insight into where these deliveries will go (over 200 are said to be in the Asia region), but we were positively surprised that the company has announced a partnership with HAECO Group, a subsidiary of Swire Group. HAECO Group is a maintenance, repair, and overhaul (“MRO”) business that has Cathay Pacific Airlines as its customer (also part of the Swire Group). Swire Group is a privately-owned quality franchise conglomerate with a strong historic legacy in the Asia Pacific – we do not believe it would establish a partnership without quality due diligence and assessment of commercial viability.

The addressable market for EHang is likely to be restricted to mainland China, and gradually build out overseas – this remains a sizable market. There will be negative incidents after certification (unfortunately as with all areas of aviation, although some safety records are better than others). However, the commercial opportunity for EHang remains large and relatively closer than previously.

Positioning and shareholder register

Investing in a speculative business in China dealing with world-first new technology, with high regulatory risk and limited disclosure means that this is a high-risk investment. Against this backdrop, any long position in your portfolio must be minimal (1% or less). If you feel that this is not viable in terms of position sizing, bear in mind that this is closer to private equity than listed.

One positive characteristic we have noticed is the growing number of large Western institutional investors on the shareholder register. Although some of these are passive funds (Vanguard, Norges), there are patches of quality long-term investors appearing (State of California, Teachers Insurance & Annuity Association, FMR). Whilst any investor can make investment errors, we believe access to information by large institutional investors is better than retail generally, and in a very binary investment thesis as EHang, their presence in a speculative stock is a positive.

Valuation

The shares are trading on estimated PBR FY12/2022 1.5x, and FY12/2023 EV/sales 3.2x. There are no earnings-based estimates, which makes a fundamental assessment difficult. However, current valuations denote limited market expectations for growth.

Risks

Upside risk is EHang obtaining certification from the CAAC. Whilst this will not mean a sudden generation of positive earnings, the outlook is a vast improvement from a business in preparation mode.

Downside risk comes from delays, postponements, and failure to obtain certification. Although the company appears to have support from the CAAC, falling at the final hurdle would place the company without a viable business.

Conclusion

EHang remains a speculative investment, and the last 2 years have been a very bumpy ride. Trying to value the company with fundamental analysis is somewhat of a moot exercise, and this characteristic should make the shares uninvestable for most. However, it has taken time but the company has made progress in the certification process with the CAAC, and their explanation of the difficulties faced as a ‘global-first’ business is credible. Whilst investing in the shares remain a waiting game for a binary outcome, we believe being long on a minority position in a portfolio still makes sense. We reiterate our buy rating.

Be the first to comment