Daniel Heighton/iStock via Getty Images

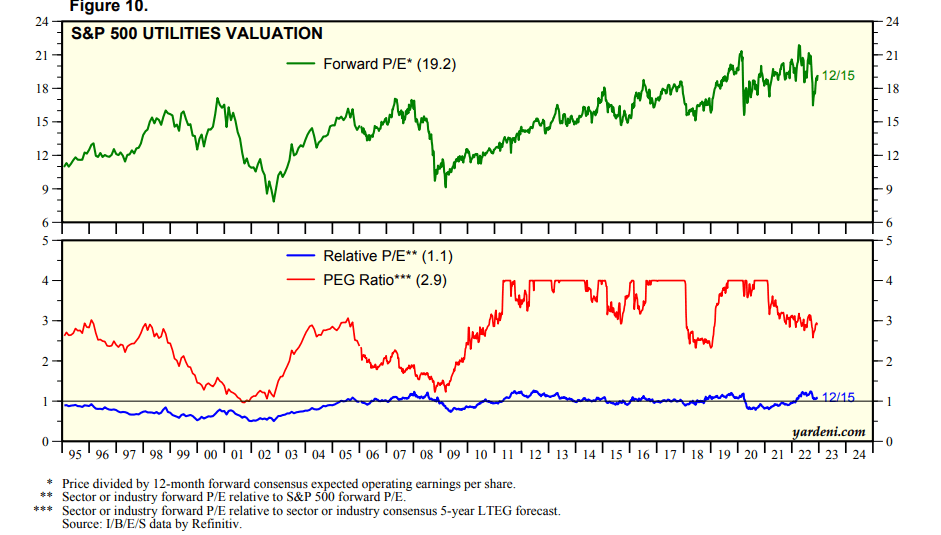

Utilities-sector stocks trade at an expensive forward operating earnings multiple compared to the broad market. At last check, the small defensive niche of the S&P 500 traded at a high 19.2 forecast P/E. With a relative P/E near 1.1, that’s actually near the 10-year average but more expensive than the long-term trend.

One stock with stagnant near-term growth and some balance sheet issues trades at a cheaper forward multiple and has outperformed in 2022. Is there more safety seen in Edison International (NYSE:EIX)? Let’s take a look.

Utilities Sector P/E: >19

Yardeni Research

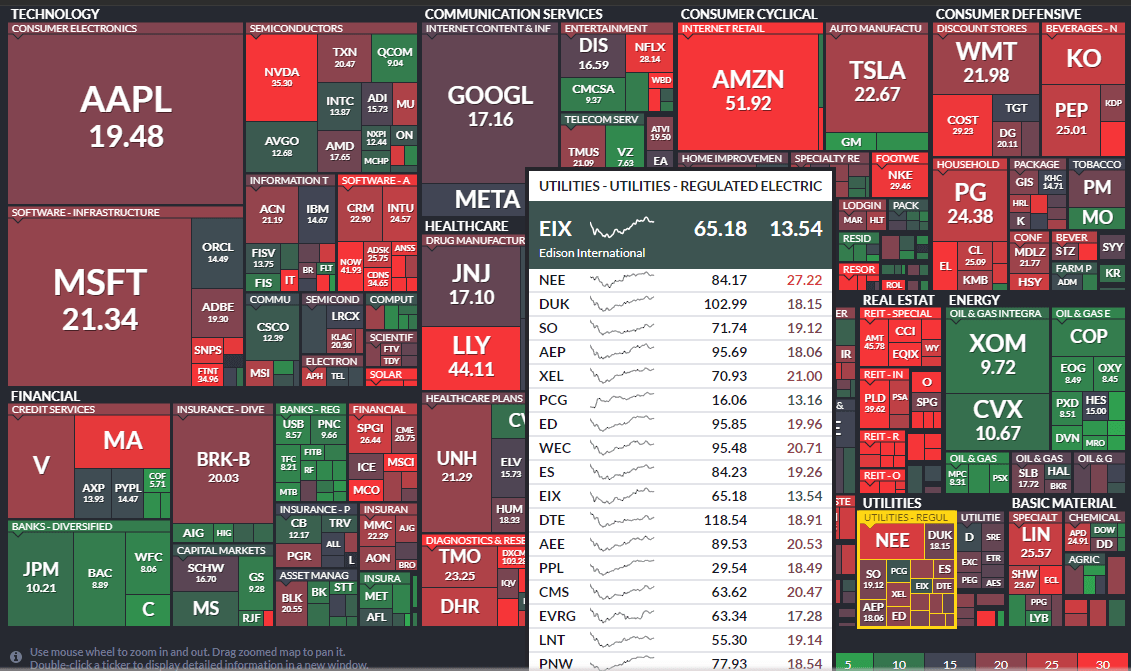

S&P 500 Forward Operating P/E Heat Map

Finviz

According to Bank of America Global Research, Edison International is the parent holding company of Southern California Edison (SCE). SCE is an investor-owned public utility primarily engaged in supplying and delivering electricity in Los Angeles and Southern California. SCE serves over 15 million residents. EIX also holds the Edison Energy subsidiary, which is a non-regulated business that operates across a range of related industries.

The California-based $24.9 billion market cap Electric Utilities industry company within the Utilities sector trades at a high 34.6 trailing 12-month GAAP price-to-earnings ratio and pays a high 4.5% dividend yield, according to The Wall Street Journal.

Recently, Edison International raised its dividend by 5.4% to $0.7375/share. That upbeat news came after the firm issued EPS of $1.48 in its Q3 report, along with a slight y/y drop in revenue. The firm narrowed its 2022 EPS outlook and maintained its long-term EPS growth rate target of +5% to +7%. The bad news, however, was that the management team increased legacy liability values. Ongoing wildfire claims and risks continue to be a concern for the stock, along with other regulatory and political uncertainties.

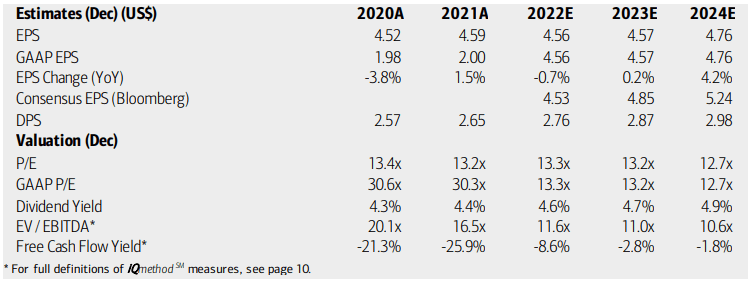

On valuation, analysts at BofA see earnings about flat in 2022 and next year. Per-share profit growth is then expected to rise modestly by 2024. The Bloomberg consensus forecast is more sanguine on EIX’s future growth prospects, though. Even with a somewhat downbeat earnings forecast, the stock’s operating and GAAP earnings multiples appear decent over the coming quarters, while investors are paid to wait. EIX trades at a near-market EV/EBITDA multiple. Overall, I continue to like the valuation, given some of the expensiveness elsewhere in the sector.

Edison International: Earnings, Valuation, Dividend Forecasts

BofA Global Research

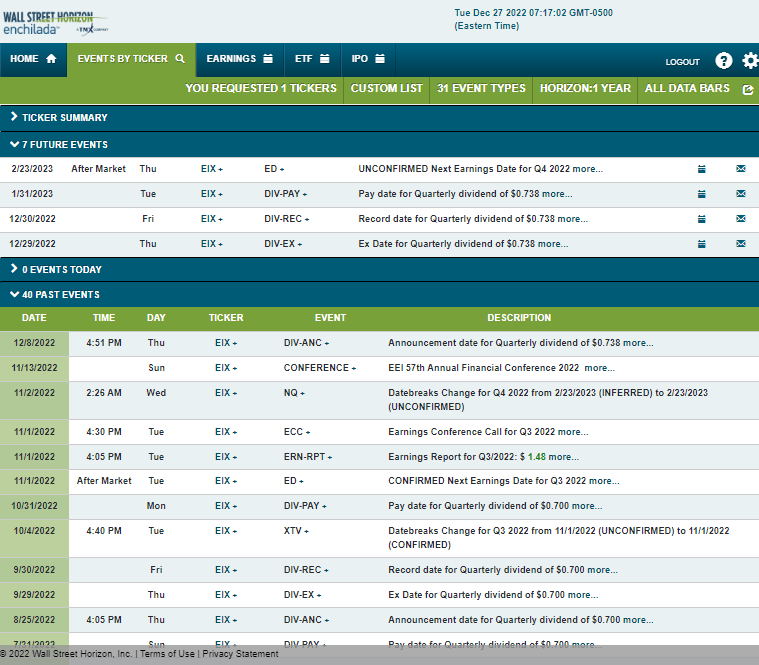

Looking ahead, corporate event data provided by Wall Street Horizon shows an upcoming ex-dividend date on Thursday, December 29 before the company’s unconfirmed Q4 2022 earnings date of Thursday, February 23 AMC.

Corporate Event Calendar

Wall Street Horizon

The Technical Take

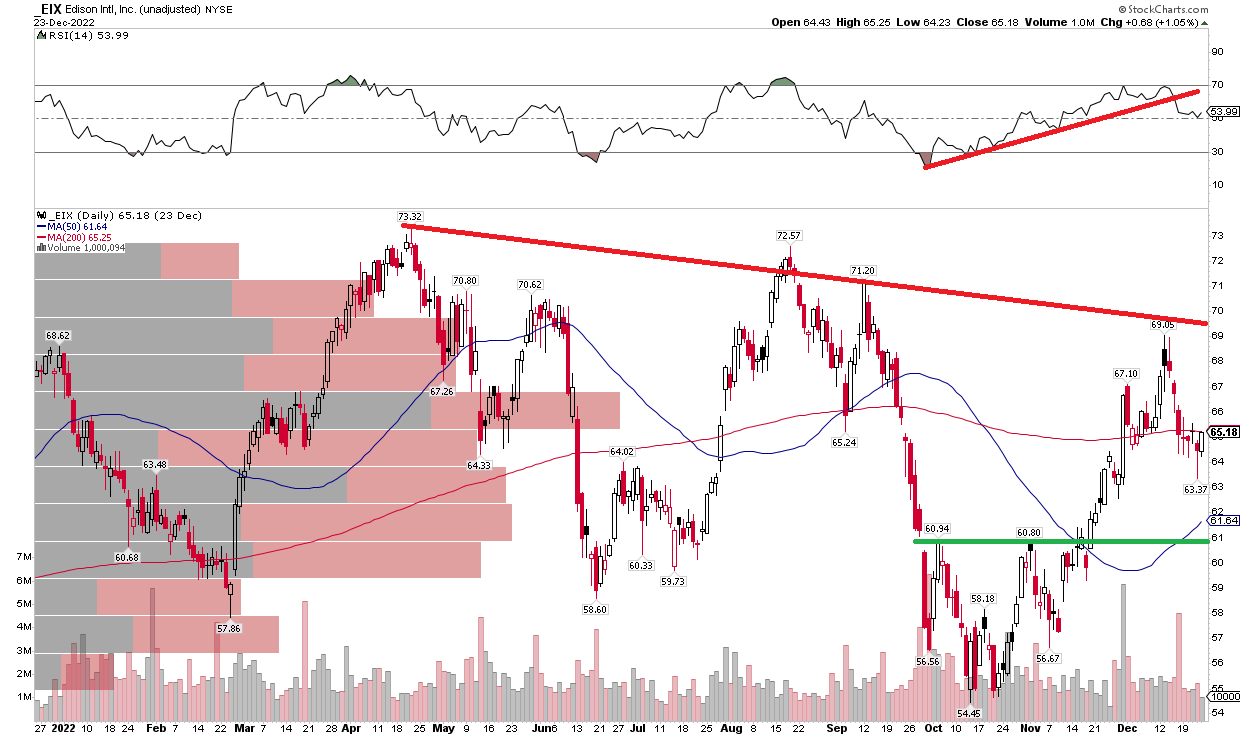

Back in July, I outlined a bullish thesis on EIX. Shares had been in consolidation mode ever since late 2017. The stock was putting in a series of lower highs and higher lows and had recently bounced off its uptrend support line within the symmetrical triangle pattern. Jump ahead to today, and the stock remains confined to a range over the last 52 weeks. Sideway price action is not a bad thing, as it means significant relative strength compared to the broad market.

With a flat 200-day moving average and RSI that has broken an uptrend, the chart on its own looks unappealing, but not outright bearish. I see general resistance in the upper $60 to low $70 while buyers have stepped up in the mid to upper $50s. The stock never got above $74 that I noted back in the summer, so that’s still a price level to monitor on the upside for a confirmed breakout. I see new support around $61 – the range highs from October and November.

EIX: Trendless Price Action in 2022

StockCharts.com

The Bottom Line

I still think some of the bearish case is priced into EIX, but with the stock not acting too well on an absolute basis lately and ongoing balance sheet risks, I’m downgrading the stock to just a hold. We will see what the management team has to say in the upcoming quarter.

Be the first to comment