johnandersonphoto/iStock Editorial via Getty Images

Eagle Point Credit (NYSE:ECC) last declared a per-share cash dividend payout of $0.14, around a 15.8% yield that has occasionally been enhanced with special payouts. The last special supplemental dividend was $0.50 per share, the prior special was $0.25 per share and came just a few months before. Hence, ECC means one thing; income. That’s its raison d’être since public inception and 2014 IPO. It’s hard not to get excited about the possibilities posed by a CEF which has paid out a more than 20% annual yield over the last 12 months. This has been through comfortable monthly installments to render the CEF as a core income holding.

Net interest income for the closed-end fund’s fiscal 2022 third quarter was $0.47 per share, which means the CEF paid out around 89% of this as regular dividends to common shareholders over 3 months. This is a payout ratio that whilst high isn’t flashing red against what’s expected to be an intense economic disruption of the corporate debt market this year. Interest rates are set to rise to a 17-year high of between 5% to 5.25% and the US could possibly fall into a recession.

CLOs And The Year Ahead

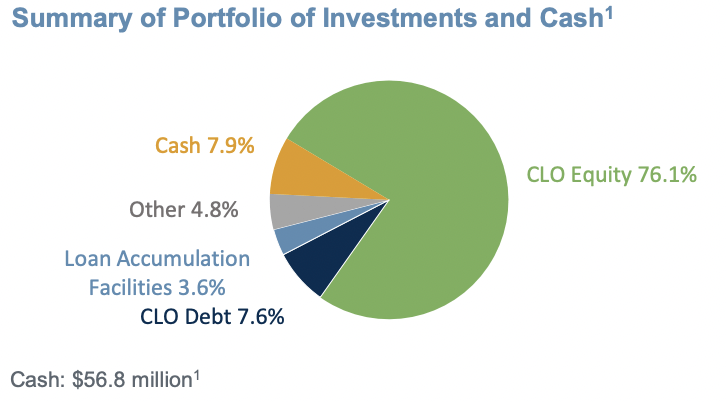

What is in ECC’s portfolio? A ton of collateralized loan obligations. The CEF primarily invests in the equity and junior debt tranches of CLOs, a relatively unknown investment vehicle that’s created from different types of pooled corporate loans. The respective tranches then receive the normal interest and principal payments from the corporate borrowers.

The CEF last updated its shareholders with a December portfolio update. As of the end of December, its NAV per share was between $9.03 to $9.13, opening up a double-digit premium with the commons currently trading at $10.60.

Eagle Point Credit

The equity tranche of CLOs is constituted of unrated and low credit-rated loans and sits at the bottom of the CLO structure. ECC’s weighted average loan rating was non-investment grade at B+/B, highlighting a portfolio with a higher chance of default. However, whilst the core investment area is clearly a high risk, the CEF has chased a material level of diversification. The underlying portfolio is diversified across 1,868 loan obligors with the CEF’s largest exposure to a single obligor being at 0.93% and with the total exposure to its top 10 loan obligors at just 6.16%.

Eagle Point Credit

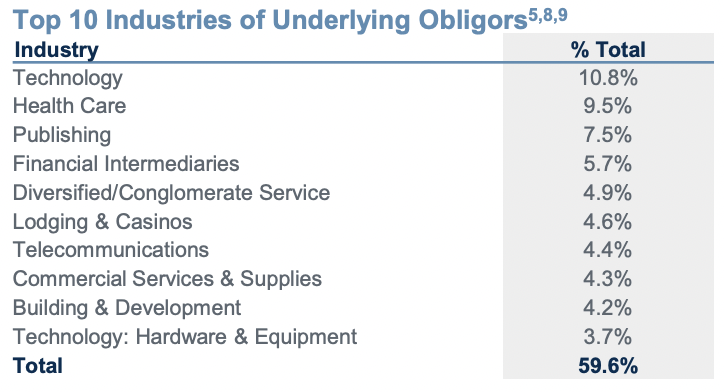

This is further diversified across several industries from technology to telecommunications and health care. Bears could point out that the comparatively higher level of technology exposure going into a recession is a weak point. Further, with the CEF trading at a 16% premium to NAV, there might be scope for weakness in the event of a recession that sees corporate defaults rise. But the bull case is built on income, and the CEF has so far created a portfolio that’s diversified across nearly 2,000 companies to mitigate, reduce, and ultimately eliminate the risk posed by singular defaults.

Exploring The Series D Preferreds

Preferred shares offer a unique investment profile, and Eagle Point’s 6.75% Series D Cumulative Preferred Stock (NYSE:ECC.PD) should also be considered in any conversation about the CEF. The Series D preferreds started trading in November 2021 when 1 million shares were sold at a $25 par value for a total capitalization of $25 million.

QuantumOnline

The likelihood of the income received by preferred holders being disrupted from now until its November 29, 2026 call date is incredibly low. It would take a near-cataclysmic event on the scale of 2008 to disrupt CLOs to the point of Eagle Point suspending its dividends. This increases the safety of the 8.1% yield paid monthly and could render these preferreds as backstops for portfolios of risk-averse income investors.

They also come with a number of investor-friendly clauses. Firstly, they are cumulative, which means that any income not paid out within the context of their normal distribution date will be aggregated as an unpaid distribution liability that Eagle Point is obliged to fully return when they redeem the preferreds. Eagle Point is also required to redeem the preferreds on or after the call date. This opens up the potential of a 20% capital uplift, with the preferreds currently trading at a discount to their par value.

Assuming the company redeems at its call date, preferred owners would have received $6.6094 in total dividend payments and $4.23 in capital uplift. $10.84 in total returns works out to be a yield-to-maturity of 52.2% over a four-year holding period, around a 13% annualized return. To place this in context, the S&P 500 has returned around 11.88% since 1957. Bears would be right to flag that these are perpetual, so any redemption event could be years after the call date. I’m currently neutral on the CEF, but I’ve placed the preferreds on a watch list for further consideration against other investments.

Be the first to comment