peakSTOCK

A Quick Take On Eargo

Eargo, Inc. (NASDAQ:EAR) went public on October 15, 2020, raising approximately $141 million in gross proceeds in an IPO that was priced at $18.00 per share.

The firm provides hearing aid technologies via a telecare consumer-direct model.

Given the risks associated with Eargo, Inc.’s recent history and positioning in the market, I’m on Hold for its stock in the near term.

Eargo Overview

San Jose, California-based Eargo was founded to develop modern hearing aid products that can be worn in the ear in a virtually invisible manner, reducing the stigma of hearing loss treatments.

Management is headed by president and CEO Christian Gormsen, who has been with the firm since 2014 and was previously at GN Group, an intelligent audio solutions company.

The company’s primary offerings include:

-

Neo HiFi

-

Eargo 5

-

Eargo 6

-

Eargo 7.

Eargo’s Market & Competition

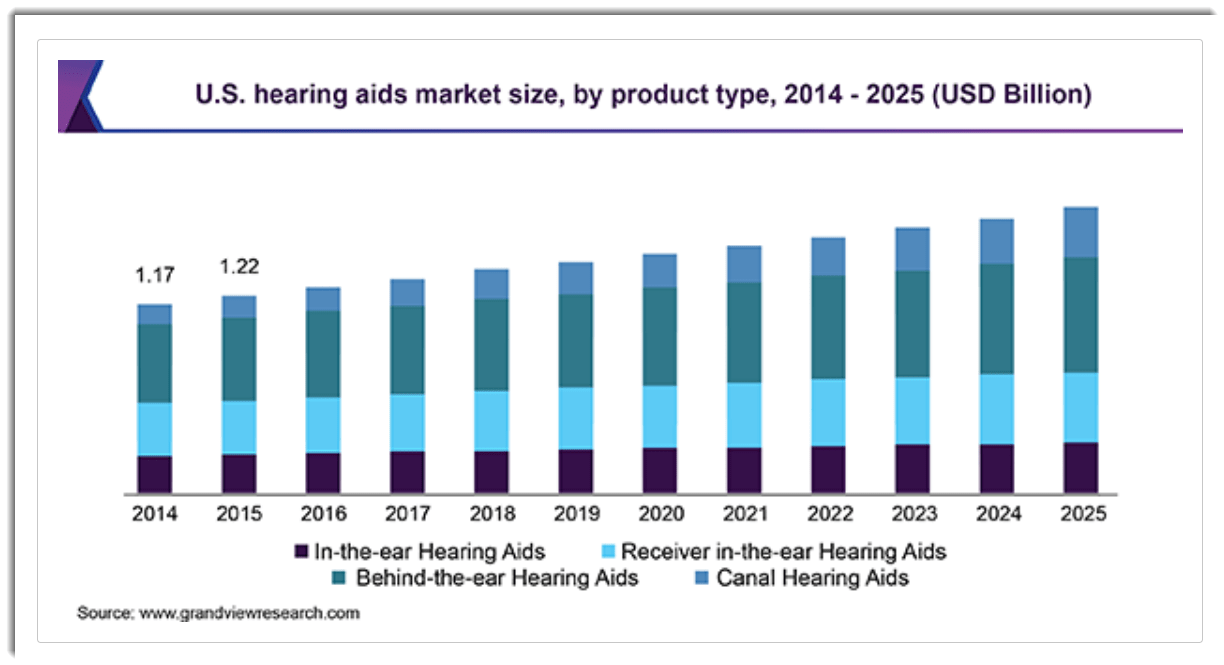

According to a 2019 market research report by Grand View Research, the global hearing aid market was an estimated $5.3 billion in 2018 and is projected to grow at what appears to be a moderate rate through 2025.

The main drivers for this expected growth are improved technological solutions combined with a growing elderly population and increasing demand for hearing enhancement devices.

Also, The chart below shows the historical and projected growth of the U.S. hearing aid market by product type from 2014 through 2025:

U.S. Hearing Aids Market (Grand View Research)

Major competitive or other industry participants include:

-

GN Store Nord

-

Sonova

-

Starkey

-

William Demant

-

WS Audiology.

Eargo’s Recent Financial Performance

-

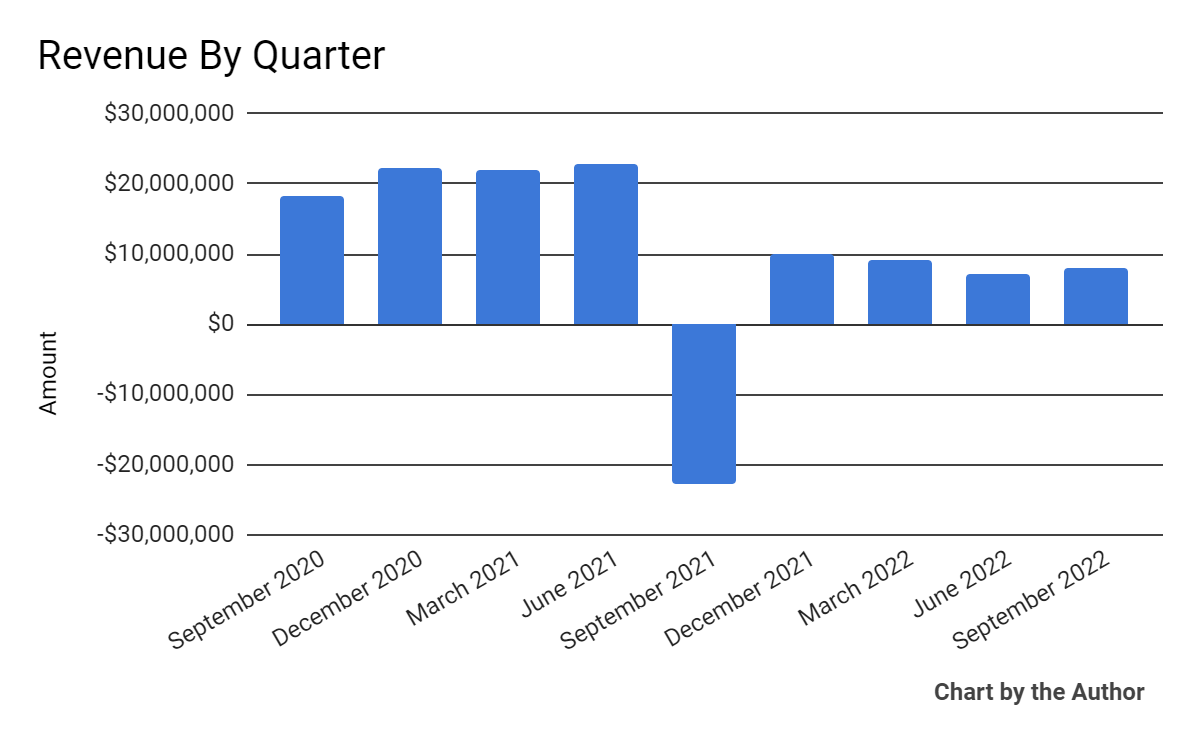

Total revenue by quarter has trended lower in recent quarters:

Total Revenue (Seeking Alpha)

-

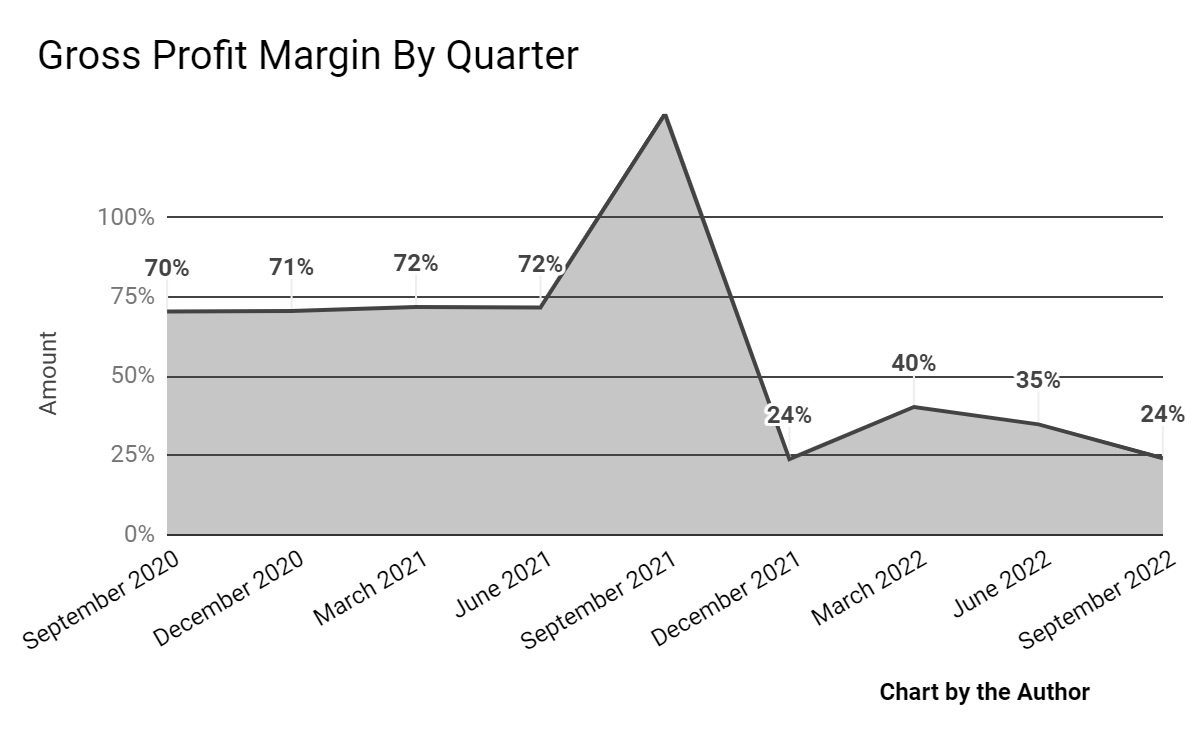

Gross profit margin by quarter has also trended lower more recently:

Gross Profit Margin (Seeking Alpha)

-

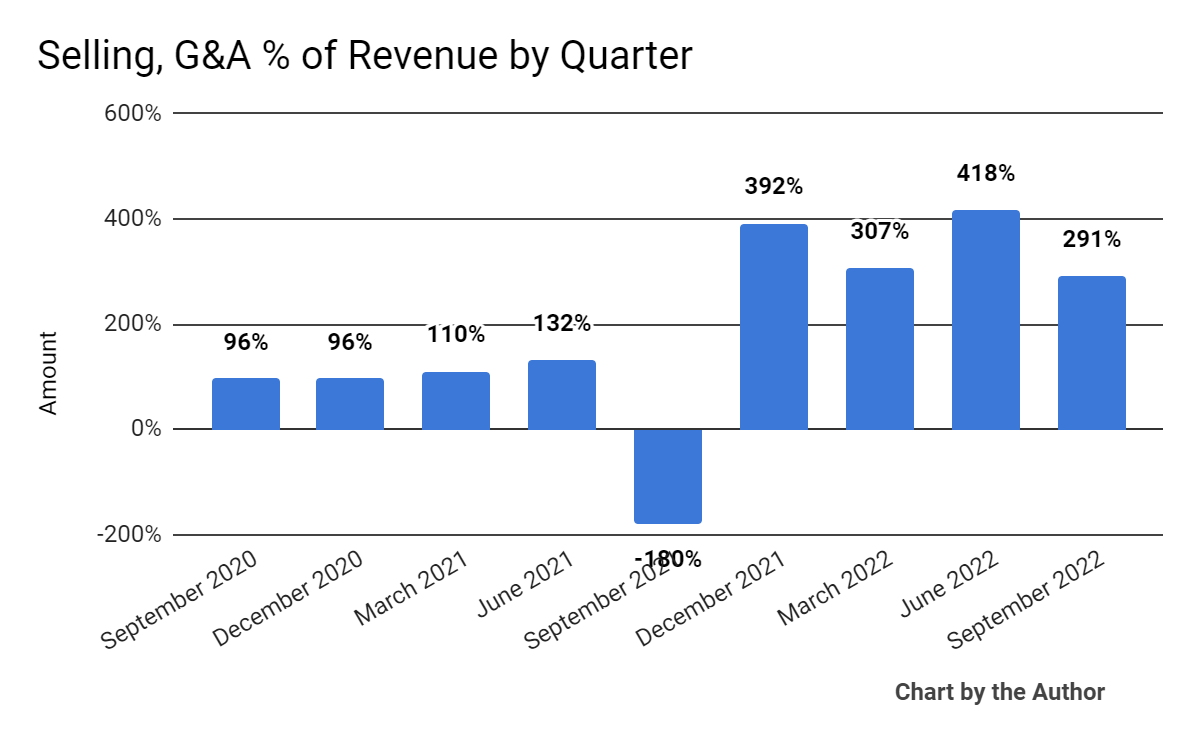

Selling, G&A expenses as a percentage of total revenue by quarter have risen sharply in recent reporting periods:

Selling, G&A % Of Revenue (Seeking Alpha)

-

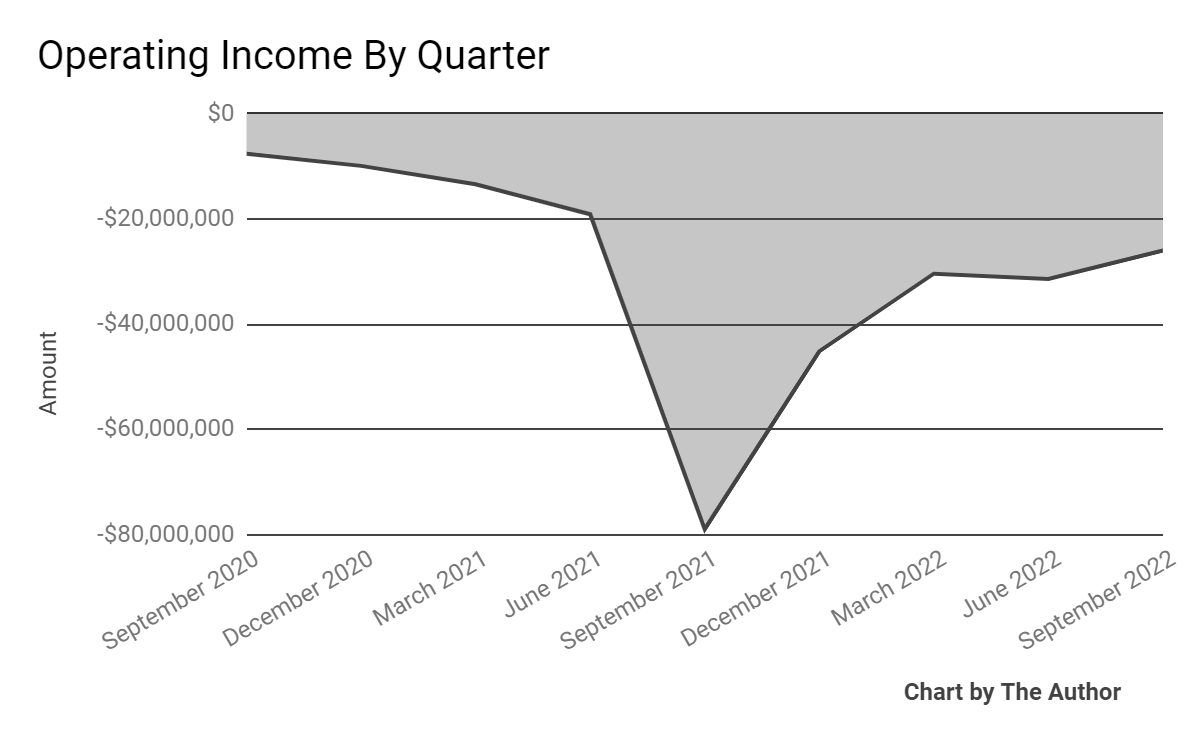

Operating income by quarter has remained heavily negative, as the chart shows below:

Operating Income (Seeking Alpha)

(All data in the above charts is GAAP.)

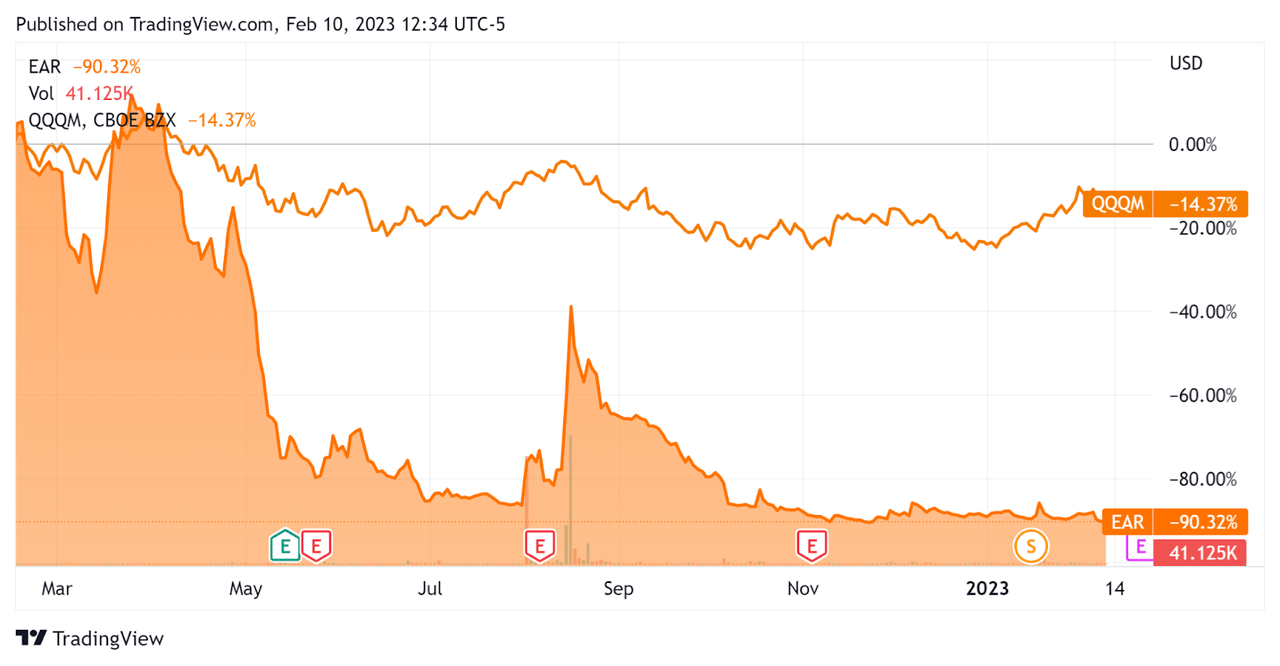

In the past 12 months, EAR’s stock price has dropped 903% vs. that of the Nasdaq 100 QQQM’s fall of 14.4%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Eargo

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

8.7 |

|

Price / Sales |

0.7 |

|

Revenue Growth Rate |

-22.6% |

|

Market Capitalization |

$255,148,560 |

|

Enterprise Value |

$298,913,568 |

|

Operating Cash Flow |

-$141,819,008 |

|

Earnings Per Share (Fully Diluted) |

-$81.02 |

(Source – Seeking Alpha.)

Commentary On Eargo

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the “small but incremental steps toward potentially regaining insurance coverage of Eargo hearing aid devices” for government employees under the FEHB program.

Earlier in 2022, the company settled its DOJ investigation wherein it agreed to pay a $34.4 million settlement “to resolve claims for hearing aid devices for reimbursement to the Federal Employees Health Benefits Program [FEHBP] that contained unsupported hearing loss diagnosis codes.”

The firm also agreed to an investment by Patient Square Capital of up to $125 million in potential total debt and future investment.

Patient Square is now the majority shareholder of the company and now has three seats on the Board of Directors out of seven total directors.

In November, the firm announced a partnership with Victra Wireless stores to demonstrate Eargo devices and provide sales through its approximately 1,500-store network in the U.S.

This was due to a recent FDA OTC Hearing Aid Rule which loosened the requirements for hearing aid sales, subject to certain labeling changes due by April 14, 2023.

As to its financial results, Q3 2022 revenue rose 9.1% sequentially, while gross margin declined sequentially from 35.2% to 24.5% due to changing product mix “and an increase in inventory reserves related to certain slow-moving inventory items.”

SG&A as a percentage of revenue dropped sequentially due to lower advertising marketing spending and a higher lead conversion rate.

Operating loss moderated slightly sequentially while remaining heavily negative.

For the balance sheet, the firm finished the quarter with cash and equivalents of $88.1 million and $125 million in total debt.

Over the trailing twelve months, free cash used was $144 million, of which capital expenditures accounted for $2.7 million. The company paid $19.5 million in stock-based compensation (“SBC”) in the last four quarters.

Looking ahead, the company only provided Q4 2022 guidance of “cash burn […] to be approximately $20 million to $25 million. Due to the uncertainty created in the business, the Company is not providing further financial guidance at this time.”

Regarding valuation, the market is valuing EAR at an Enterprise Value / Revenue multiple of 8.7x, a still impressive figure given the firm’s troubles recently.

The primary risks to the company’s outlook are the damage to its reputation in the marketplace as a result of the DOJ settlement as well as the potential for a slow process for being readmitted to the FEHB government employee coverage program.

A potential upside catalyst to Eargo, Inc. stock could include faster-than-expected ramp-up of its Victra partnership.

However, the premium pricing level of its hearing aid products and the lack of history of consumers purchasing them through a mobile-phone retail store concept makes me leery of the firm’s ability to substantially grow the business through this channel.

While the partnership has some potential future incremental growth possibilities, it’s hard to get too excited by this pioneering approach at this early date.

Given the risks associated with Eargo, Inc.’s recent history and positioning in the market, I’m on Hold for its stock in the near term.

Be the first to comment