CatLane/iStock via Getty Images

Dynex Capital (NYSE:DX) is one of those relatively obscure REITs whose investability has become wrapped in uncertainty due to a macroeconomic environment characterized by rising interest rates, back-to-back Fed rate hikes, and the rising specter of a recession. There could be a soft landing, perhaps not, but Dynex is nursing a 12-month decline of 13.4% in the value of its commons. The mREIT invests in agency and non-agency residential mortgage-backed securities and also holds commercial mortgage-backed securities. Founded in 1987, the Glen Allen, Virginia-based firm went public a year later. MBS are essentially securities backed by a pool of mortgages with the agency variant backed by a pool of mortgages issued by government-sponsored agencies like Freddie Mac and Fannie Mae. They’re relatively safe but come with lower potential returns than non-agency MBS.

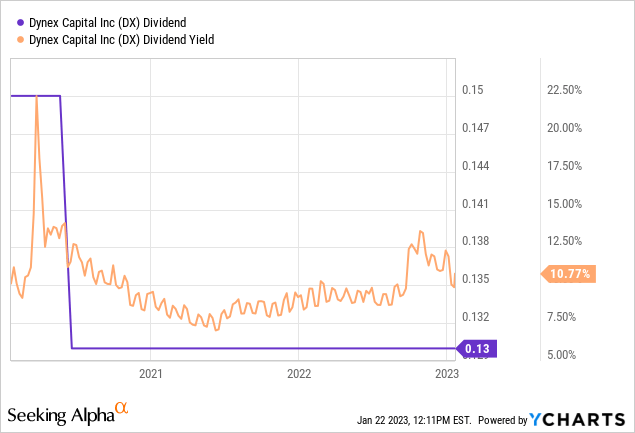

The appeal of MBS is threefold. They offer a high degree of liquidity, a low correlation to risk assets, and income from the cash flow derived from mortgage payments. The total US MBS market exceeded $12 trillion in 2021 and offers investors a way to outperform US Treasuries without a significant increase in the correlation of their fixed income portfolios to equities. The mREIT last declared a monthly per share dividend payout of $0.13, in line with the previous payout, for a yield of 10.77%.

How Safe Is The Monthly Payout?

Dynex has maintained its current monthly payout since June 2020 when it reduced the payout by 13% from a prior level of $0.15 per share. This was a period when most mREIT were forced to cut their payouts due to the rapidly collapsing economic backdrop. Hence, are we staring at yet another cut with the Fed set to hike interest rates to a 17-year high of 5% to 5.25%?

Bears, who currently form the 4% short interest in the mREIT, would point to the retrenching housing market and the potential inability of a growing number of homeowners to service their mortgages as unemployment rises and mortgage rates spike.

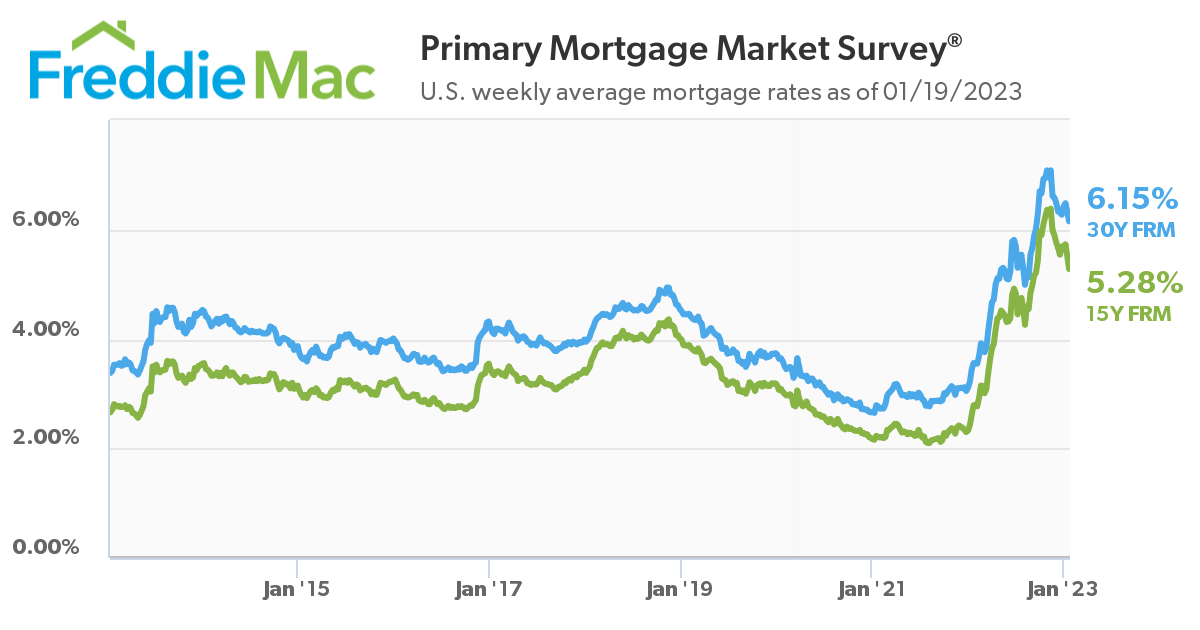

Freddie Mac

And whilst the 30-year fixed-rate mortgage rate continues to trend down in recent months on the back of moderating inflation, it still remains at its highest level since 2008 with the latest figure of 6.15% being the lowest since September of last year. However, unemployment remains under control with the most recent figure for December 2022 dropping to 3.5%, below market expectations of 3.7%.

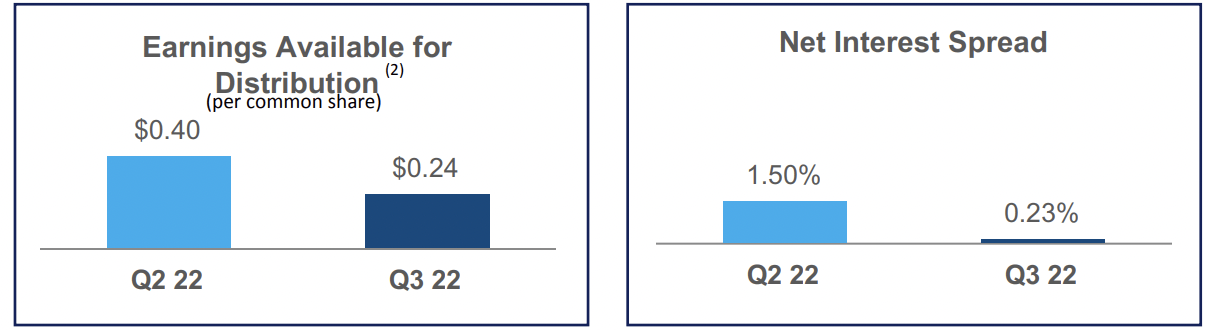

Fundamentally, buying into a seemingly strong yield that’s then cut is what keeps me up at night with the salary like monthly payouts of Dynex’s commons also being a nice feature to have. The mREIT last reported earnings for its fiscal 2022 third quarter saw net interest income of $7.12 million, a decline from $14.1 million in the prior second quarter and a fall of 74.3% from the year-ago period. This came as the mREIT’s net interest spread collapsed to 0.23% from 1.5% in the prior second quarter.

Dynex Capital

This drove earnings available for distribution of $0.24 per share, way below the aggregate 3-monthly dividend payout of $0.39 per share. However, this would be one side of the equation. The mREIT has not hedged its exposure to rising interest rates through conventional interest rate swaps but has instead employed a strategy of shorting US Treasuries. This led to a taxable income in the third quarter of $9.4 million, around $0.21 per common share. The total of both these distributable earnings is $0.45, more than enough to cover their distributions.

The Preferreds Offer Stability And A 7.6% Yield On Cost

Preferred shares are great. They offer bond-like features within an easy-to-buy security that ranks higher than the commons on the dividend totem pole. Dynex 6.90% Series C Fixed-to-Floating Cumulative Redeemable Preferred Stock (NYSE:DX.PC) offer an alternative to the commons for more risk-averse income investors.

QuantumOnline

They currently pay a $1.725 annual coupon, distributed quarterly, which works out to be a 7.6% yield on cost. Further, with the preferreds currently trading at $22.65 versus their $25 redemption value, investors could grab a healthy 9.4% discount to par on their purchase. Dynex has been aggressive with the redemption of its previous preferreds, hence, the Series C comes with a high probability of being redeemed shortly after its call date on April 15, 2025. Assuming the mREIT redeems on this day, it would hold a yield to call of 27.5% as a total income of around $3.88125 would be aggregated with a $2.35 capital uplift.

Whilst this rate of return would of course change in response to the redemption date, it’s a strong baseline rate of return from a security with a low risk of suspending payment or trading at significant divergence from its redemption value. The Series C also comes with a fixed-to-floating clause which will see their annual coupon change to the Three-Month LIBOR plus 5.461% per year from the redemption date. Overall, whether to go with the preferreds over the commons will depend on your appetite for risk and your bearishness on the state of the US economy. Whilst the housing market is already in relatively dire straights, it could get worse to set up the preferreds as a better investment option. I’m neutral on both but lean towards the preferreds.

Be the first to comment