stockcam

It’s time to invest in growth again. With the market rallying in the early weeks of 2023 and growth stocks getting a facelift after a year of painful declines, long term-oriented investors have a great chance to buy into high-quality names at valuation multiples that have lost the madness of the 2020-2021 era.

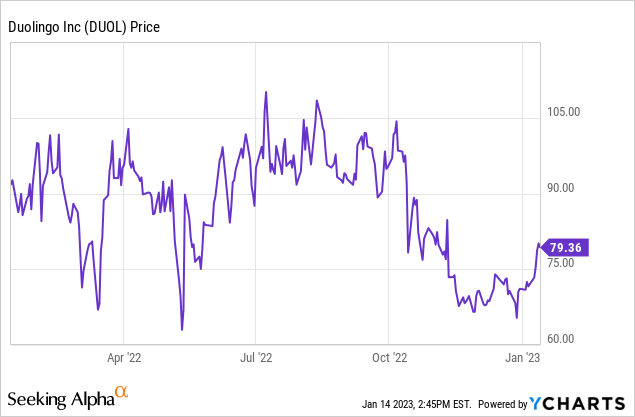

Duolingo (NASDAQ:DUOL) is a fantastic internet app to look into. Most of the sector is battered by declines in online advertising (even titans such as Facebook (META) have lost more than half of their market value), but Duolingo, down “only” ~15% over the past year, has held on to its value thanks to a revenue base that is built almost entirely on subscriptions. And despite the fact that this popular language-learning app has now been on the market for years and is a well-known education brand, the company still shows healthy double-digit growth in bookings, revenue, and most importantly subscribers.

Though Duolingo doesn’t have the “fallen angel” appeal of many other tech stocks at the moment, I can’t help but to still champion Duolingo thanks to its fantastic fundamentals and its consistently expanding product base.

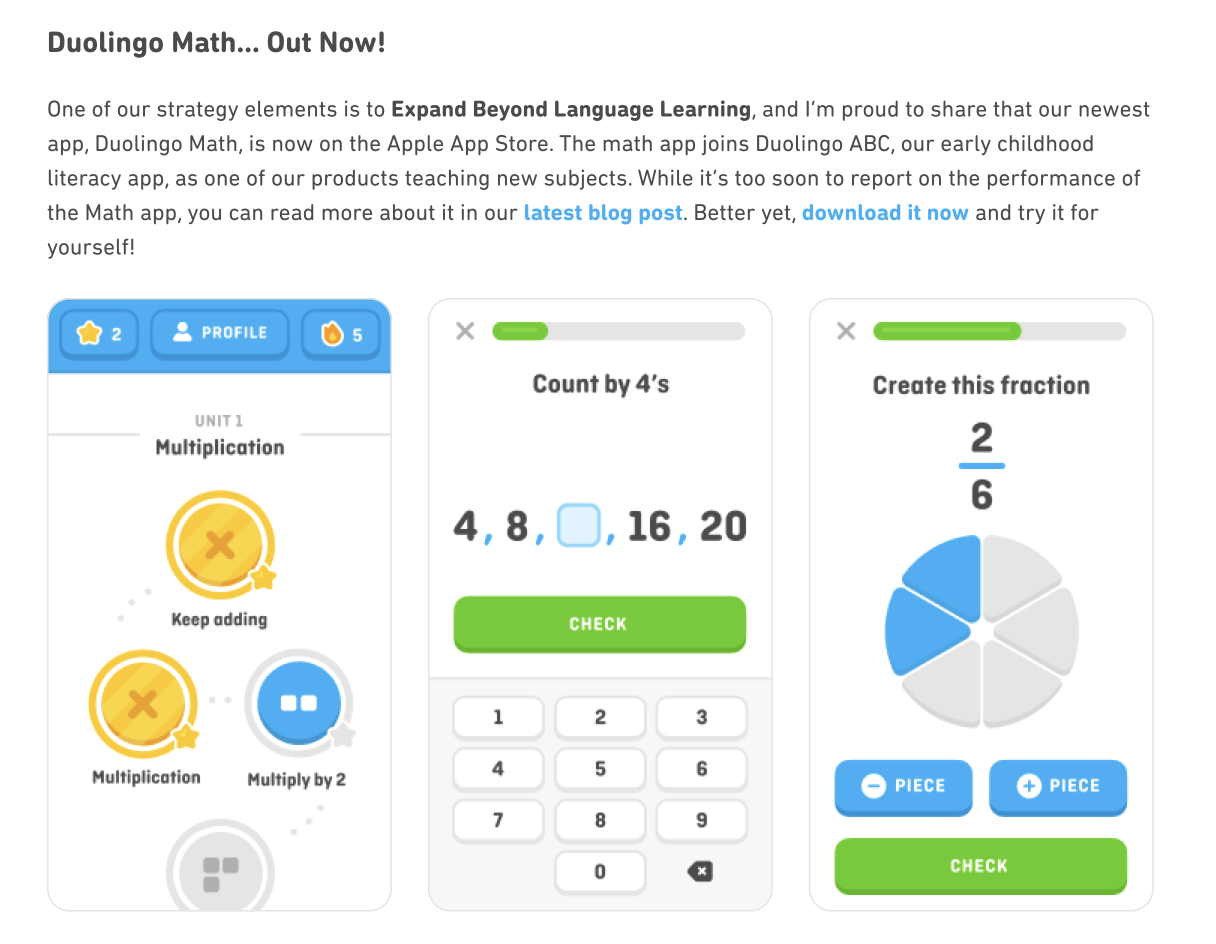

Note as well that Duolingo just released its Duolingo Math product – opening up a brand-new market territory for the company and planting the seeds for its next stage of growth.

Duolingo Math release (Duolingo Q3 shareholder letter)

In the future, I see Duolingo expanding its brand across a wide number of subjects and potentially creating bundles across its products.

For investors who are newer to Duolingo, here is my full long-term bullish thesis for tech company:

- Accelerating growth. Over the past few quarters, despite its own growing scale, Duolingo has maintained bookings and revenue growth north of 40% y/y, driven both by increased monetization/conversion of free users into paid ones, as well as effective engagement across its marketing channels.

- Duolingo has an incredible product. I use Duolingo myself on a regular basis (and yes, I am among the ~7% of Duolingo’s user base who is a Super Duolingo subscriber), and am impressed by the way the company has condensed the difficulty of language learning into bite-sized, gamified lessons. The fact that Duolingo has stats to back up the notion that seven units on Duolingo (roughly the entirety of most of the languages in Duolingo’s catalog) gives users the same proficiency as five semester-long college courses only serves to highlight the immense value that Duolingo provides in its well-designed app.

- Pent-up travel demand is encouraging language learning. One of the top reasons that people learn a language is to travel. With the post-COVID world continuing to normalize and with foreign borders opening up for tourism again, the resurgence in travel will likely also lead to a pickup in demand for Duolingo.

- Additional monetization opportunities. Duolingo has three revenue streams. On top of its Plus subscriptions, Duolingo makes money from advertising and from administering English proficiency tests. The latter, in my view, is a burgeoning market that could eventually see Duolingo turn into a language-accreditation service for languages other than English. New subject matter expansions like math should also serve to broaden Duolingo’s market potential.

- High gross margins. Right now, Duolingo is losing money because it’s focused on product development and growth. But its underlying ~70% pro forma gross margins give it ample room to scale profitably, like many other software and internet peers.

The bottom line here: there are plenty of reasons to believe that Duolingo is still in the early stages of capturing a rapidly growing, casual online-learning market. Stay long here and ride the upward wave.

Q3 Results

If there’s one tech stock that has been almost entirely immune to macro headwinds, it’s Duolingo. The company continued to deliver on its beat-and-raise cadence in its Q3 results, giving us confidence that performance will continue to shine in 2023.

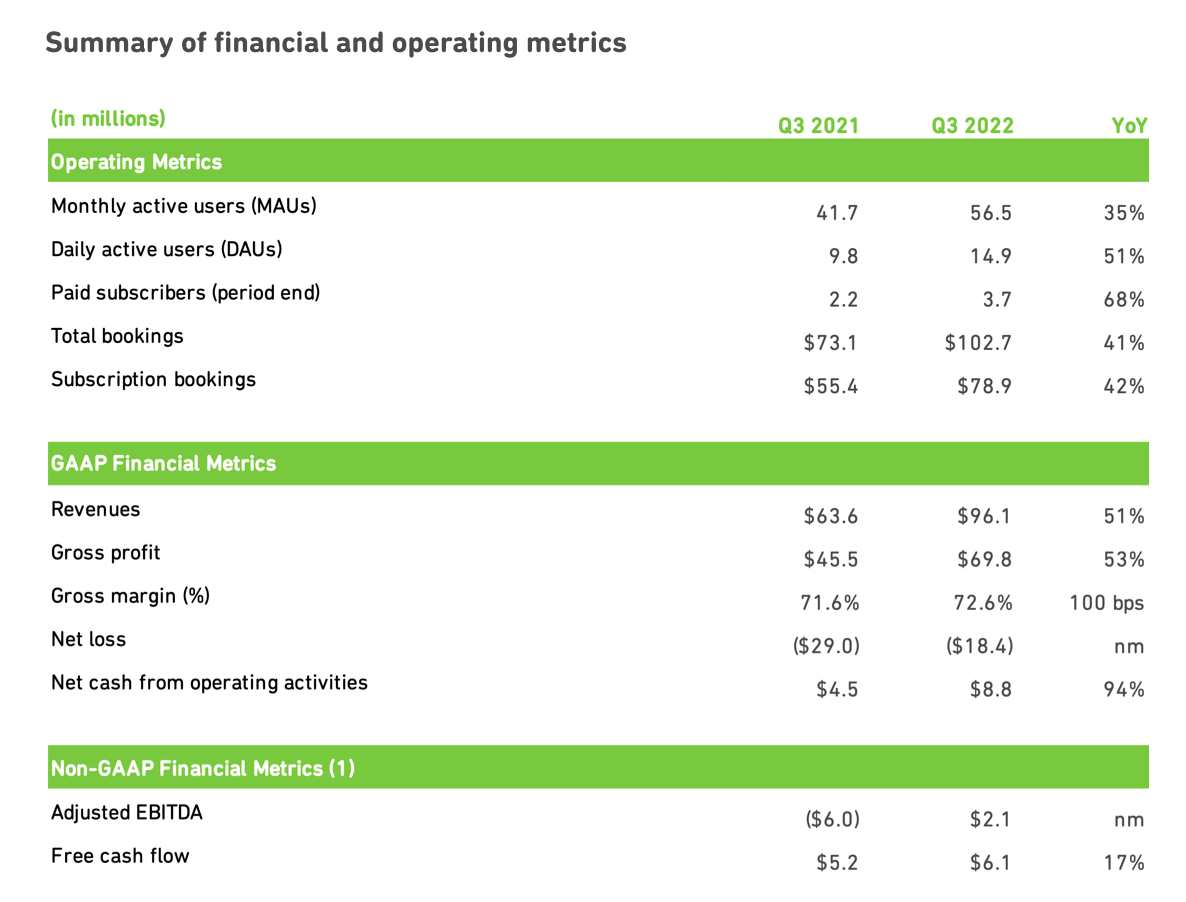

Here are some of the highlights in the snapshot below:

Duolingo Q3 highlights (Duolingo Q3 shareholder letter)

Key to note is that Duolingo’s paid subscribers grew 68% y/y to 3.7 million, outpacing even DAU growth of 51% y/y. Duolingo reported that both DAU and MAU growth accelerated for the fifth straight quarter.

Revenue of $96.1 million also grew at a stunning 51% y/y pace, outpacing Wall Street’s expectations of $95.3 million (+50% y/y).

Duolingo’s strategy of gamifying learning has continued in full force. The company recently introduced new timed challenges as well as a flashcard-type game called Match Madness that have driven a substantial increase in in-app purchases (which largely take the form of players purchasing gems to trade for extra “lives” or boost time within certain challenges). In-app purchases are now roughly 5% of Duolingo’s total bookings, up from 3% in the prior year.

So far, management has noted that the company has not seen any slowdown from macro challenges to its top-line trends, barring a small headwind to advertising revenue which makes up a very small portion of Duolingo’s overall haul (in Q3, advertising revenue of $10.6 million represented 11% of Duolingo’s total revenue). Per CEO Luis Von Ahn’s remarks on the Q3 earnings call:

We’re not seeing any signs of consumer softness in our subscription metrics and as a result, we’re raising our full year guidance again. I want to spend a little more time talking about our user growth because it’s so important for our business […]

And our strong use in growth this year will also help drive bookings growth in the future because we have a great free product without a paywall, a good portion of the learners that have joined us this year will convert to paying subscribers in the coming quarters, providing a tailwind for subscription bookings.

As to other parts of our business, you all know that the digital advertising market has faced headwinds this quarter. And while this impacted our ad revenue, the overall impact to our business has been small because ad monetization isn’t a major focus for us.

Rather than actively seeking to grow this revenue stream, ads have served more of a strategic purpose for us, which is to help give learners a reason to convert to paying subscribers.”

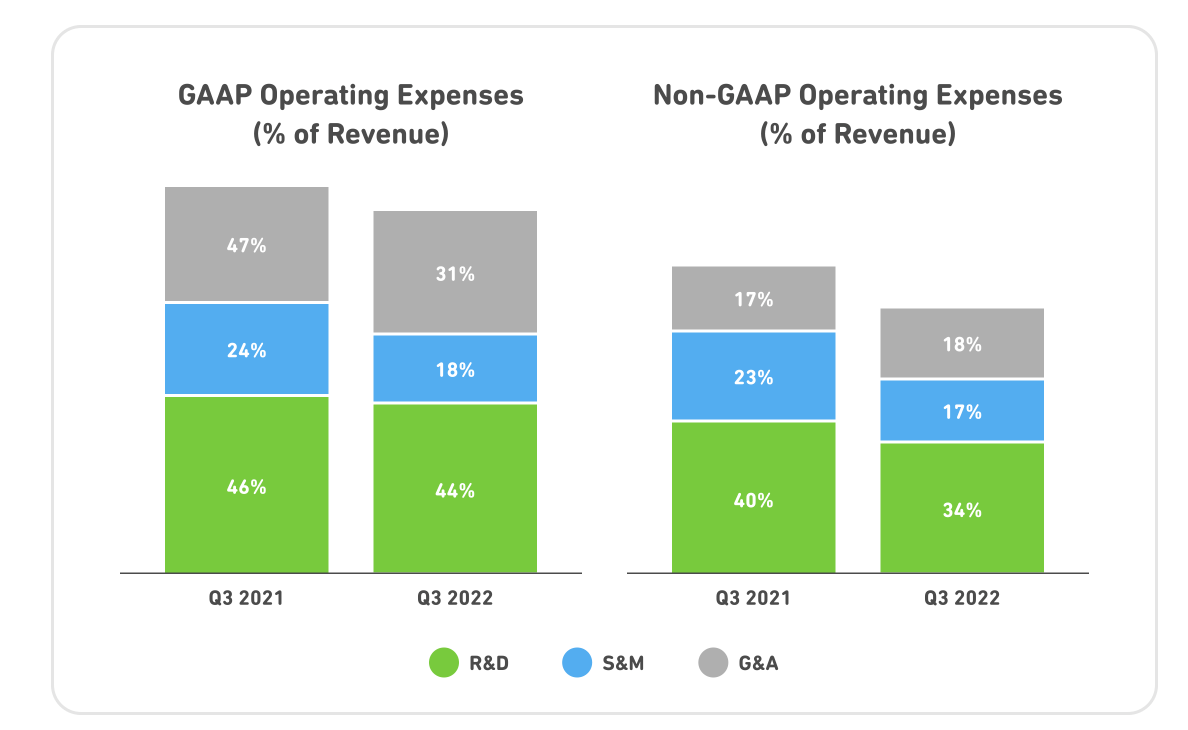

From an opex perspective, Duolingo has moderated its advertising and customer acquisition spending, while also avoiding the layoffs that have plagued the rest of the sector. Natural operating leverage has given Duolingo tremendous gains in profitability, as total opex shrunk to 69% of revenue on a pro forma basis, down from 80% in the prior-year quarter – driven by six-point reductions in both G&A and sales and marketing spend.

Duolingo Q3 opex trends (Duolingo Q3 shareholder letter)

Duolingo also generated $2.1 million in positive adjusted EBITDA this quarter, representing a 2.2% adjusted EBITDA margin – a huge eleven-point improvement from -9.4% in the year-ago Q3. In my view, the company’s strong bottom-line performance increases its appeal in today’s relatively more risk-averse market.

Key takeaways

An expanding product universe, a sticky customer base with a high-margin recurring revenue stream, and tremendous growth in active users and subscribers – there’s a lot to like about Duolingo. Stay long here.

Be the first to comment