stockcam

What is Duolingo?

Duolingo (NASDAQ:DUOL) is a language learning platform that uses game-like lessons and challenges to help users learn new languages. It provides a variety of online language courses for different levels and offers instruction in more than 40 languages.

What is their Competitive Advantage?

Their competitive advantage is making learning fun. Anyone who has used Duolingo knows the app has created fun bite-sized lessons that have been crafted through a combination of engaging syllabus, gamification and AI algorithmic learning. In essence the app is a network effect as users grow, the algorithm has more data to provide the right level of difficulty in lessons but also gamify in the process.

AI algorithms using deep learning predict at any given moment the probability of a user being able to recall a word in a given context and then can figure out what that user needs to keep practicing. The algorithms analyze user data to then personalize the learning experience.

Duolingo’s process has been working to date:

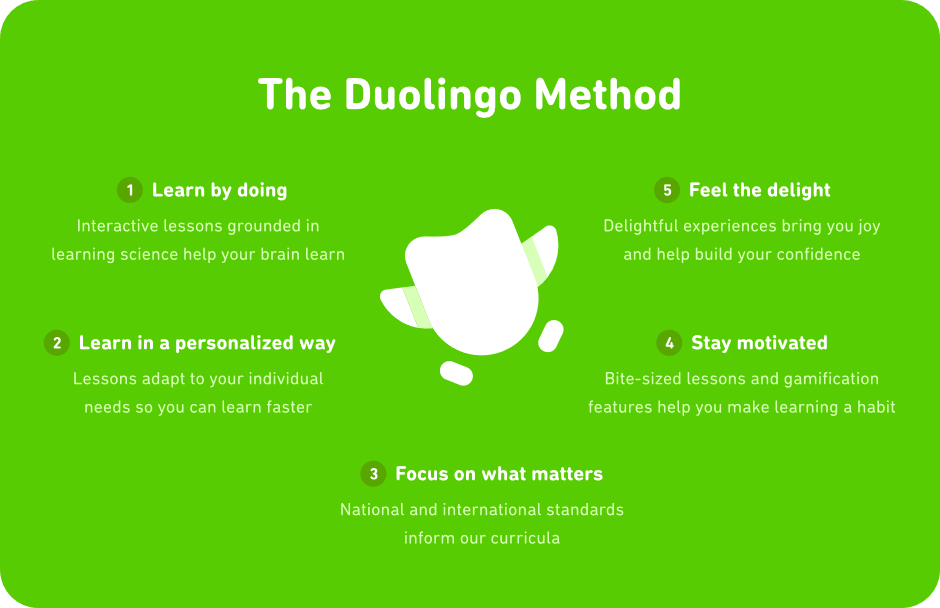

The Duo Method (Duolingo Website)

“Duolingo’s bite-size lessons feel more like a game than a textbook, and that’s by design: You’re more motivated to keep learning when you’re having fun. But Duolingo isn’t just a game.

It’s based on a methodology proven to foster long-term memory of what’s being learned, machine learning technology that personalizes learners’ experience, and curricula informed by national and international standards.”

Its free version of the app is another competitive advantage. While there are competitors who offer a free version of their service, the amount of languages available and breadth of content available on Duolingo act are what set it apart. The free version which collects ad revenue funnels learners into Duolingo’s premium paying subscription ad free service.

Negative Reviews

I have read negative reviews online that language learning apps including Duolingo’s have excellent active user numbers (through gamification) but the method is not the best way to learn a language. This speaks to whether Duolingo’s competitive advantage has staying power in providing long term value to learners:

Why Duolingo Won’t Get You Fluent (But Why You Should Use it Anyway)

500 Days of Duolingo: What You Can (and Can’t) Learn From a Language App (Published 2019)

They argue the best way to learn language is through conversation which Duolingo does not provide. However, from my analysis no other competitor can provide a better solution to this issue. Furthermore, it needs to be recognized that language apps in general won’t make you fluent in a language by themselves. Conversations are required. However, apps such as Duolingo help in the immersion process, vocabulary, listening skills and grammar. The app can get individuals up to a conversational level of speaking.

In summary, Duolingo’s competitive advantage is the app is beneficial for language learning beginners.

Market Size & Competition

Speaking to The Guardian in 2014, von Ahn said: “There are 1.2 billion people learning a foreign language and two thirds of those people are learning English so they can get a better job and earn more. The problem is that they don’t have equity and most language courses cost a lot of money.”

Determining the size of Duolingo’s market is difficult due to the overlap in learning between online and offline syllabus. However, we can get a sense of the opportunity from looking how much of the market Duolingo dominates and various research reports on the future growth of the industry.

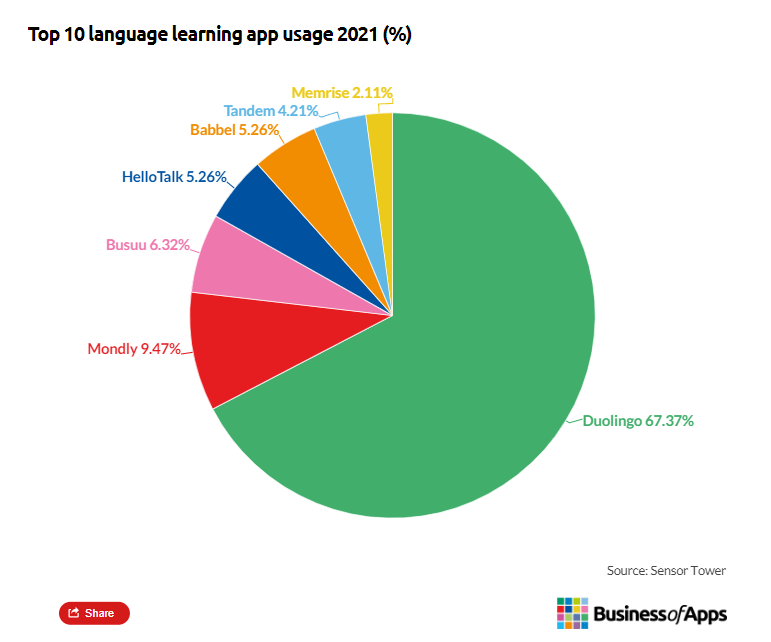

Duolingo has over 60% of the language app market.

App Market Share Language Learning (Business of Apps Website)

Online language market future CAGR rates range from 10% – 20%.

Meticulous research believes CAGR of 20.3% in forecast period between 2022 and 2029.

Brandessence Market Research believes the number is closer to 18.3% CAGR until 2028.

Verified Market research thinks the language market will grow annually at 10.65% until 2026.

Wall street analysts have 2023 and 2024 have sales growth at 26% and 23% respectively. So Duolingo is growing faster than the industry at least over the next two years.

Financials

Revenue growth is expected to slow from 45% in 2022 to 26.6% in 2023. However, it is expected to remain above 20% until at least 2025. The pandemic wave brought heightened isolation time which artificially increased revenue growth levels in the years 2020-2022. 20% top line growth is still respectable going forward. Subscription revenue from premium offering makes up 72% of sales with 16% to advertising on free version and the remainder from the Duolingo English Test. Operating metrics in latest quarterly report continue to point to outperformance in daily active users (DAUs) and paid subscribers both increasing over 50% YOY.

Luis Von Ahn CEO “Today, nearly 70% of our daily active users have a Duolingo streak longer than 7 days.” This highlights there is increasing engagement among Duolingo users.

Gross margins current and forecasted are expected to remain above 70%, with predominant cost of revenues stemming from third party processing fees, wages and stock based compensation.

Net margins for 2022 are negative at -18% and are likely to remain so until 2027. While market reaction wasn’t positive to this long path to profitability in a rising interest rate environment, the company’s top line is arguably more important at this stage. As discussed later management execution in controlling bottom line will be important to monitor as they grow from here.

Debt financing remains minimal at 4% of total capital indicating low default risk probability. Cash flow from operations is heavily impacted by share based compensation. Just like net margins we should expect to see this grow over time operating growth metrics and management execution play out.

Valuation

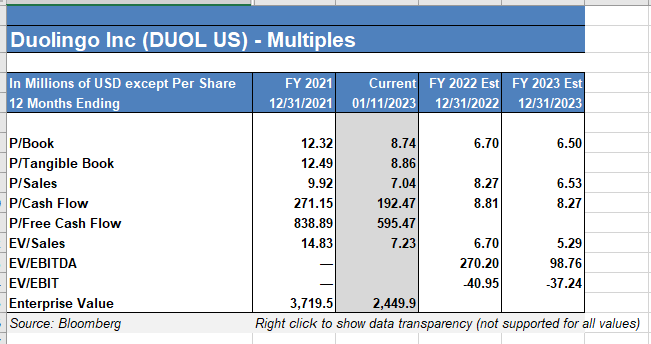

Duolingo Historic Multiples (Bloomberg)

On a historic basis Duolingo has become significantly cheaper over the last few years.

Valuation comparable to other listed education software providers of a similar size:

Comparative Valuation Metrics (Compiled with Finviz.com)

Powerschool and Instructure holdings are the closest comparable listed companies to Duolingo, under the GICS sector Application software > Specialty Software > Education Software category.

Both are learning based platforms, Powerschool providing cloud-based software for K-12 education connecting students, teachers administrators and teachers to improve student outcomes. Instructure Holdings is a web-based learning management system. Duolingo is only slightly more expensive on P/S basis but you get double the sales growth. Book value is high due to other companies’ capitalization of intangibles on their balance sheet and FCF is essentially negative for Duolingo with SBC pushing cash from operations positive. The zero debt is nice to see but negative margins is one to watch. Yes, the company is in growth mode but a pathway to profitability should be monitored especially in higher interest rate environment.

Earnings Call

I have highlighted below some the key points from the latest earnings call:

Management do not see any signs of slowdown in subscriptions and their raised guidance confirms this view. The app is quite recession proof given its free service offering and low monthly subscription model. Similarly the company does not foresee any hiring freezes or layoffs.

Digital advertising did experience a headwind during the quarter, but similar trends were seen across the industry with $NFLX, $GOOG also seeing pullback. 20% of revenue is advert driven and the slowdown should only be seen as a short term cyclical concern.

In relation to forward plans Duolingo Maths offers another avenue of growth and the technology they have developed to date should mean economies of scale in future subject rollouts. While optimistic the CEO indicated the app will predominantly focus on language growth going forward. I tend to agree as there are still large opportunities in geographic markets and further monetization of the app to exploit.

Future Avenues for Growth

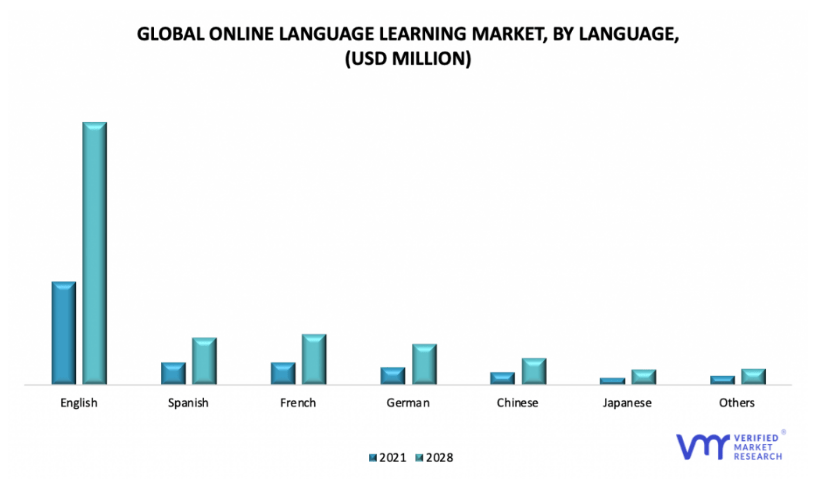

The CEO mentioned on the latest earnings call that the majority of Duolingo’s active users are English speakers looking to learn a second language. However English as a second language is the largest language market worldwide and offers significant opportunity to grow into. It is probably why Asia is the fasting growing segment of the user base.

Global Online Language Learning Market (Verified Market Research )

Duo Math

Duo math is another opportunity to expand the brands offering. While in the early stages I am excited by the CEOs comments of how the learning techniques and algorithms used on the language platform can be scaled quickly to other syllabuses with small teams. This is very encouraging form of scalable growth opportunities.

In the future there could even be other school subjects science, geography etc, all bundled into a fun and engaging way of learning.

Family memberships

Learning through collaboration is important especially when languages are concerned. Duolingo’s Family Membership. I can envision a scene where weeks before a family vacation to Spain a Duolingo family pass is obtained to learn together.

Duo for Schools

Duolingo for Schools is a free layer of management that sits on top of the Duolingo language learning app. You (As a teacher) can gain visibility into and a level of control over your students’ experience on Duolingo, tracking progress in the process. Any integration into the classroom would be a great step for growth. Any community growth strengthens the competitive advantage by building network effects and brand value.

Testing

Duolingo currently offers an English Test. There is scope to expand to other tests and become a hallmark in standard testing for language learning.

Risks to Duolingo

Short Sighted Goals

Duolingo core product is teaching a language in a fun and interactive way. I noticed on latest call how the CEO is looking to grow the GEM economy within the app. The GEM economy is the currency of Duolingo and would be used to “buy” access to additional in-game challenges, add additional lives etc. While a margin accretive avenue of growth I hope this gamification doesn’t detract from the core learning goals in the process. For example, too many prompts to play/buy gems may irritate players. Also, unfairness in the leader board may cause people to lose interest in competing as those who pay (buy GEMS) have better chance to score higher.

Usefulness for Intermediate and Advanced users

While beneficial for beginners there is a risk the app is not useful for more experienced users. This may impact the longevity and recurring revenue model of Duolingo’s subscription service where it derives the majority of their revenue. I would like to see features that expand the service to these customers perhaps through Testing (discussed earlier), conversation rooms, more difficult syllabi and expansion of foreign language podcasts for learning.

“Passive learning creates knowledge. Active practice creates skill.”

Path to profitability

The stock fell on last quarter report given latest net margin is -18% with analyst forecasting profitability won’t be reached until 2027. Yes, the company is in growth mode, but need to monitor to ensure negative earnings don’t get out of control especially in higher interest rate environment.

Metaverse/Gaming (long shot)

Long term threat from metaverse style gaming options that are more interactive that the current mobile app model in teaching.

Conclusion

Duolingo has a large market to grow into, many lucrative markets remain untapped. There are many growth avenues for Duolingo to solidify its market leading position. E.g. community expansion, GEM economy, testing, other learning subjects etc. The company is fairly valued on a comparative basis and valuation metric basis, but under-valued if it maximizes its growth potential. I would buy a starter position and add on weakness here, given the expensive macro backdrop. I would add to my position if growth metrics continue to outperform and the community grows. I like the exponential growth prospects, but the company has only been public for 2 years and I would like to see further confirmation of management execution before adding further.

Be the first to comment