noel bennett/iStock Editorial via Getty Images

We have a good grip about Dufry (OTCPK:DUFRY). We anticipated the potential business combination with Autogrill (OTCPK:ATGSF; OTCPK:ATGSY) and we commented when it was finally announced. The Mare Evidence Lab buy case recap was based on the following:

- Higher FCF generation from pre-COVID-19 level thanks to cost-saving initiatives;

- A positive trajectory in travel rebound thanks also to the strategic/inorganic acquisition of Hudson during the health crisis;

- A compelling valuation versus Wall Street analyst expectations that were pricing a full recovery in numbers in 2024 and just a fraction of the permanent cost-saving that the company was aiming to achieve.

Half Year results

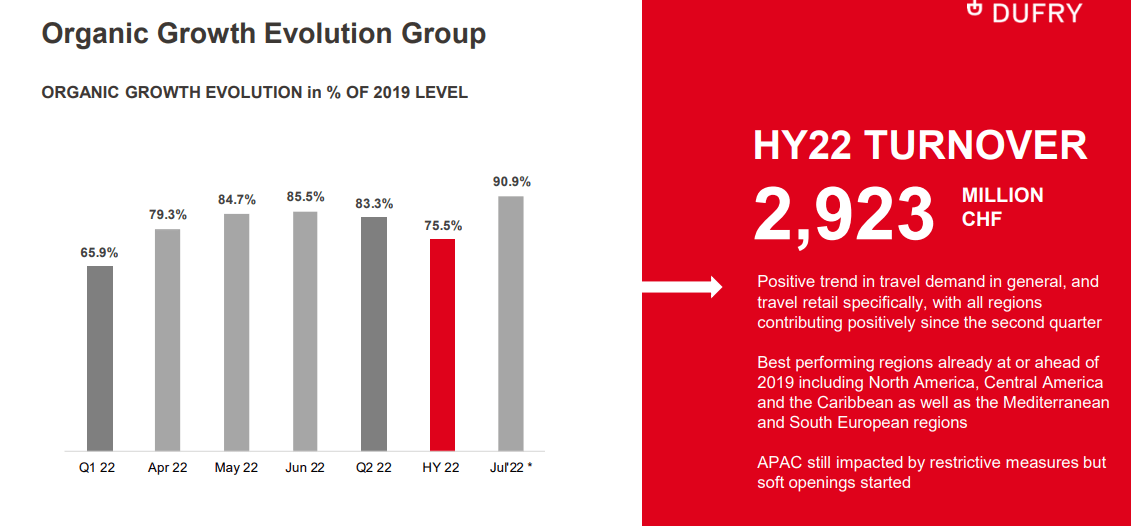

In the first half of the year, the Swiss multinational group increased its revenue line by 147% to CHF 2.9 billion compared to the same period in 2021. The recovery had already started in the first three months of the year but further accelerated in the second quarter with the group’s turnover at 75% of pre-pandemic levels, with July at 90%.

Dufry travel rebound

The United States is among the areas of the group to have marked the greatest growth, but positive signs also come from Central America and the Mediterranean countries. On the other hand, China remains in decline, due to the prolonged closures due to government travel restrictions. In numbers, APAC revenues totaled CHF 55.4 million against CHF 52.1 million recorded in the same period one year ago (equal to 16.3% of the sales achieved in 2019). In the Americas, turnover doubled to CHF 1.3 billion from CHF 638 million (82% compared to the 2019 numbers). While in Europe, the Middle East and Africa area, the main region for Dufry’s business, the company recorded a turnover of CHF 1.46 billion compared to CHF 376 million last year equal to 78% compared to 2019. However, thanks to the world tourism recovery, profitability improved. Core EBIT stood at CHF 104 million compared to the CHF -244 million recorded in the first semester of 2021. The group’s core EBIT margin was at the same level as HY 2019 (despite a turnover that remains approximately 30% below the levels of 2019).

Conclusion and Valuation

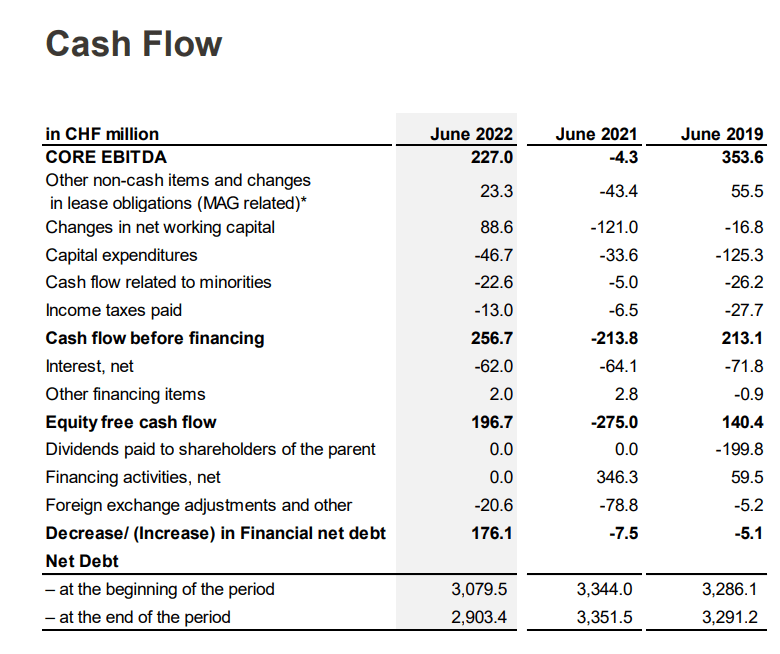

In the meantime, the merger with Autogrill is proceeding according to plan. The go-ahead should come from the extraordinary shareholders’ meeting on 31 August. Dufry expects that the first step of the transaction, namely the transfer of the 50.3% stake in Autogrill by Edizione to the Swiss company, will take place within the third quarter. Important to note is the debt evolution. Indeed, net debt amounted to CHF 2.9 billion at the end of June compared to the 2019 numbers at CHF 3.1 billion. As noted in our investment summary, cash flow is also higher compared to the pre-covid-19 level. These results provide support for the stock in the short term, but the increase in macro risks in the second half and in 2023 will go in part to counterbalance this effect. However, we reaffirm our valuation and our risks.

Dufry cash flow

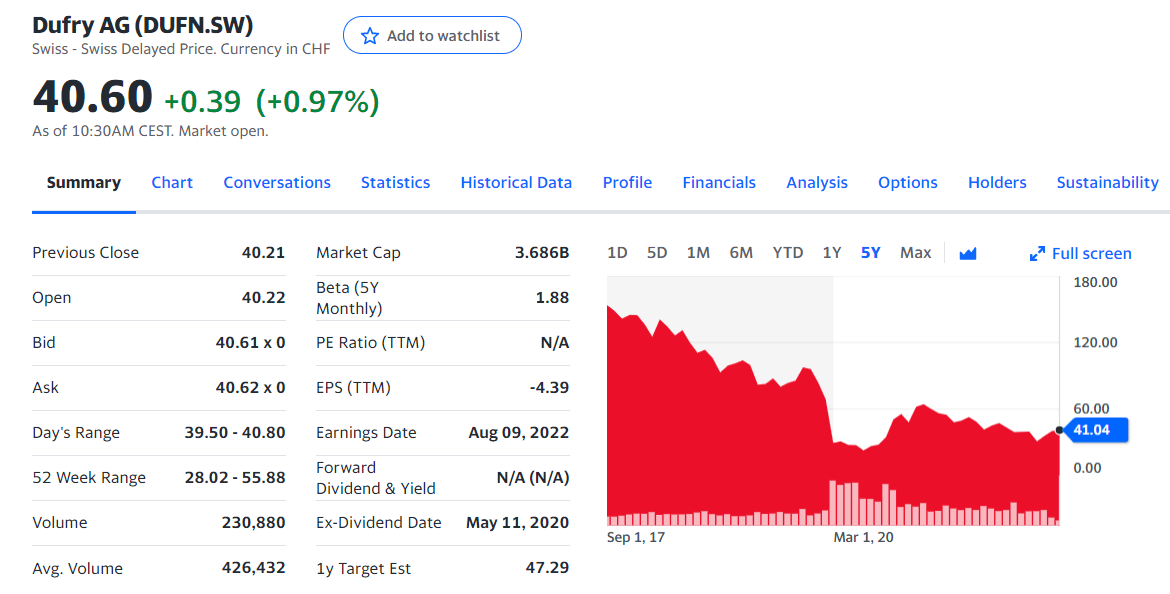

Dufry AG stock price evolution

Be the first to comment