skynesher/E+ via Getty Images

This dividend ETF review series aims at evaluating products regarding their past performance and their current portfolio quality.

DTH strategy and portfolio

The WisdomTree International High Dividend Fund (DTH) has been tracking the WisdomTree International High Dividend Index since 06/16/2006. It has a portfolio of 410 stocks, a distribution yield of 3.25% and a total expense ratio of 0.58%.

As described by WisdomTree, to be eligible in the index, companies must pay regular cash dividends, be incorporated in Japan, 15 European countries, Australia, Israel, Hong Kong or Singapore, have a market capitalization of at least $200 million and an average daily dollar volume of at least $200,000. The top 5% ranked by dividend yield and the bottom half of a risk ranking based on momentum and quality metrics are excluded.

Then, companies ranking in the top 30% by highest dividend yield are selected for inclusion. They are excluded when they fall out of the top 35%. Their weights are adjusted based on dividends. The index is reconstituted once a year. Components are mostly large companies (81%).

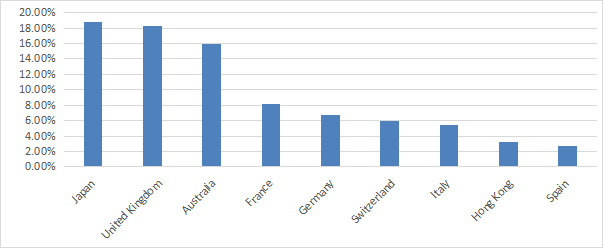

The heaviest countries in the fund’s portfolio are Japan (18.8% of asset value), the U.K. (18.3%) and Australia (15.9%). Other countries weigh no more than 8% individually and 47% together.

DTH countries (Chart: author with Fidelity data)

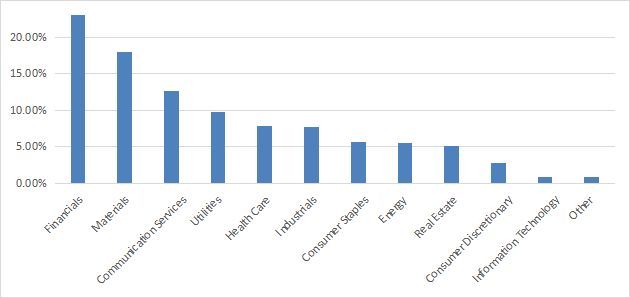

The three heaviest sectors are financials (23% of asset value), materials (18%) and communication (12.6%). Other sectors are below 10%.

DTH sectors (Chart: author with WisdomTree data)

The top 10 holdings (next table), represent 23% of asset value. Exposure to BHP Group is significant: over 6%. Risks related to other companies is limited. For convenience, the tickers below are listed in the U.S., whereas the fund holds stocks in primary listing exchanges.

|

Ticker |

Name |

Weight |

EPS growth %TTM |

P/E TTM |

P/E fwd |

Yield% |

|

BHP Group Ltd |

6.30% |

N/A |

10.83 |

9.31 |

8.43 |

|

|

Rio Tinto Group |

3.13% |

119.23 |

5.72 |

7.27 |

11.42 |

|

|

Novartis AG |

2.53% |

202.77 |

7.73 |

13.23 |

4.05 |

|

|

Nippon Telegraph and Telephone Corp |

1.99% |

23.64 |

10.54 |

10.77 |

3.33 |

|

|

GlaxoSmithKline plc |

1.83% |

-17.71 |

16.88 |

12.80 |

5.35 |

|

|

SoftBank Group Corp |

1.74% |

41.07 |

3.47 |

9.88 |

0.95 |

|

|

Fortescue Metals Group Ltd |

1.64% |

36.94 |

4.69 |

N/A |

9.20 |

|

|

Sanofi |

1.61% |

-46.78 |

17.51 |

12.24 |

3.75 |

|

|

Commonwealth Bank of Australia |

1.44% |

45.62 |

15.37 |

N/A |

3.68 |

|

|

Anglo American plc |

1.40% |

318.03 |

7.21 |

8.42 |

5.76 |

Past performance

The next table compares DTH performance since January 2008 with the First Trust Dow Jones Global Select Dividend ETF (FGD), reviewed here, which has a slightly higher yield and includes U.S. based companies.

|

Since 1/1/2008 |

Total Return |

Annual Return |

Drawdown |

Sharpe |

Volatility |

|

DTH |

11.24% |

0.75% |

-61.51% |

0.15 |

19.38% |

|

FGD |

64.41% |

3.57% |

-66.21% |

0.27 |

20.92% |

Data calculated with Portfolio123

With a meager 11% total return in 14 years, DTH has significantly lagged FGD. As a reference, SPY has returned 288% in the same time (about 10% annualized). DTH annualized total return since 2008 is close to zero.

In fact, DTH share price has suffered a loss of -23.6% since inception in June 2006:

DTH share price (TradingView on Seeking Alpha)

Including distributions, the total return since inception is 52%, or 2.7% annualized (calculated with Portfolio123). The average annual inflation rate since 2006 has been 2.1%, so the inflation-adjusted total return after tax since inception would have been close to flat, and likely slightly negative for most investors.

Takeaway

DTH has a portfolio of about 400 stocks paying high dividend yields from developed countries. More than half of asset value is concentrated in three countries (Japan, U.K., Australia) and three sectors (financials, materials, communication). The strategy looks good and includes a risk filter. However, historical performance is underwhelming. Capital loss since inception has resulted in an inflation-adjusted annualized total return below 1%, before paying tax. DTH might be a good instrument for swing trading or tactical allocation, but in my opinion it is not a “buy-and-hold” component for a sustainable retirement plan. DTH is not unique in this regard: many high-yield instruments have been suffering significant capital decay and/or income stream decay. DTH has a 3-star rating at Morningstar, which I find overrated. For transparency, a dividend-oriented part of my equity investments is split between a passive ETF allocation and my actively managed Stability portfolio (14 stocks), disclosed and updated in Quantitative Risk & Value.

Be the first to comment