sb-borg

Above: We’ve moved into Phase Two of the evolution of the sector: Time to start making money not continue promising and promising.

It’s no longer time to plod through all the accumulated rationale prepared by analysts as to the prospects of DraftKings Inc. (NASDAQ:DKNG), bullish or bearish. I think it’s time to cut once and for all, the umbilical cord that keeps feeding the DKNG fantasy that sales growth will be sustained to eventually produce enough free cash flow (“FCF”) to push it into strong profit.

WSJM

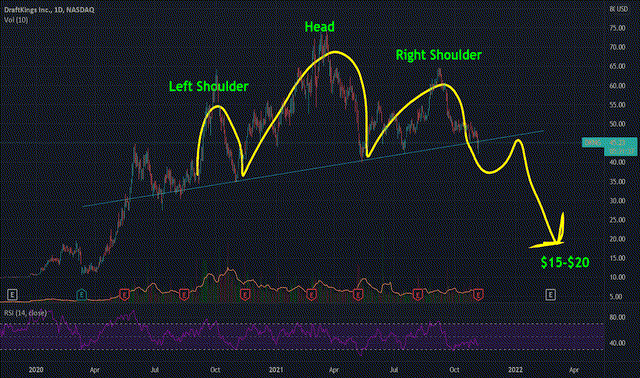

Above: For those techies, the news isn’t very good. I think even $15 as a target may be a bit of a tough go if the recession really ramps fast in 2023.

Sports betting will be a good business five years from now after consolidation and the evolution of a reasonable, sustainable ratio of promotional spend vs. controllable churn among regular players. But it will never be a monster business, because in the end, bells and whistles, league and player partnerships notwithstanding, a sports bet will have devolved it into a commodity entirely based on deal promotions. If the sector shrinks down to five or six major players, it’s a good utility.

Sports betting has much in common with streaming media. Too much spend for too few eyeballs left. Too thin of margins, no real moats for anyone, growth coming ever closer to the brick wall of new markets coming to the rescue. But for survivors, sports betting will indeed become a reliable contributor to EBITDA for the casino operators and the pure play international legatees with global marketing reach.

There is and has always been, lots to like about DKNG. It has been an early mover in the space. It is fast off the starting line as new states legalize. It has loaded up its marketing heft with all kinds of team, league, and brick-and-mortar partnerships that meet the test of broadening its overall reach. Its second place share of market reflects a database that shows long life.

Given that, we cannot ignore the simple truth that, long after phase one of sports betting’s birthing in 2018, DKNG continues to stick to a dead-end formula: throw money at every new state, pay heavy promotional dollars for customer acquisition, and pursue the Jeff Bezos dream that at some point, if the market really swells wildly huge, management will land two feet on lucrative ground. That’s a policy directly headed for, dare we suggest it, the junkyard of wannabee tech stocks, or worse. Change is afoot in the space, but DKNG is sitting tight.

google

Above: DKNG’s great strength was converting its fantasy players into sports bettors at a fast clip, but that pathway has begun to peter out.

Market leader FanDuel (DKNG is a close second) has just inched into profit, indicating it made $22m in the latest quarter and is continuing to hold its lead against bruising competition from the top players in the space: DKNG, BetMGM, Caesars Sportsbook, and others.

Sales growth at far too high a price persists in DKNG’s strategy long after it should have been sent a one-way ticket under the bus. DKNG expected revenues of $2.16b to $2.19b for 2022, rising to $2.8b for 2023. They posit a loss of $475m in $575m which many analysts believe leans a bit optimistic. Projecting 2023 revenue, DKNG believes it can reach $2.8b to $3b which should find 4Q23 moving into the black.

Profitability in 2023 is problematical given the sustaining and growing competitive pressures coming from both the top five well-heeled competitors as well as the other 80 fringe operators still scuffling around the space.

Key competitors already understand that Phase One of the US sports betting explosion is over. DKNG is still using the Phase One playbook: Overspend for new states, keep spending enough in mature states to hold share. It won’t work.

Caesars Entertainment, Inc. (CZR): Has been carving away at promotional spend for the last two quarters and slicing more ahead. CZR has already bought UK’s legacy William Hill’s U.S. business (it sold off the international piece). It provides strength in live sports books throughout the casino landscape.

BetMGM: Is expected to revive its effort to buy its UK partner Entain’s 50%. It is part of an overall bullish move by parent MGM Resorts International (MGM) to a leadership position in every vertical in which it holds a major stake: Las Vegas Strip, U.S. Regional casinos, MGM China. BetMGM’s aggressive pursuit of sports betting leadership reached an estimated 29% share of market just below FD and DKNG each of which hold anywhere from 37% to 45% depending on the state.

Barstool Sportsbook (PENN): Understand that the idea is not to madly pursue market share but make money on the share you have. Use sports betting customer demos to market its casinos to a younger demo. Turn profitable faster. Smart money here.

Flutter (OTCPK:PDYPF, OTCPK:PDYPY). As the market leader with its FanDuel, parent Flutter offers its U.S. unit a powerhouse international business as a cash flow bolster. The resolution of its dispute with Fox Sports (FOX) over valuing its 18% of FD means that PDYPY is now free to seriously pursue a spin-off. That would position FD as a pure play in U.S. sports betting with Fox as a major holder should they decide to hang in. It points clearly to Phase Two which is consolidation and a retreat from excessive promotions ahead.

After the leaders, you have the second-tier operators like BetRivers, PointsBet, Bet365, etc. These are tied to either international operators or U.S. casinos. And that is the beginning of the formation of Phase Two:

The two pure plays in the space will be FD and DKNG fighting head to head for a combined, sustainable market share of 60% of the entire sector revenues as it reaches the end of the legalization phase. (Moving from the present 30 states to those about to go live (Massachusetts and Ohio, will bring growth to the leaders in 2023). But the really big kahunas are in something of legislative limbo at the moment. Sports Betting suffered a major defeat in California at last month’s election.

The tribal casinos appear to be in the driver’s seat ahead, but given what else is going on, the likelihood of California going legal any time before 2026/7 is remote. Texas is mulling, Florida is still in hand-to-hand combat between the Seminoles and potential commercial operators with the state not appearing to be in any rush to get it done. So, realistically the 30/32 states either now legal or about to go live is where the industry will probably come to a rest stop over the next five years or more.

Best estimates of U.S. online legal sports betting’s future.

Forget the insane estimates some analysts made of the ultimate size of the market we saw throughout the wild sequential legalizations of 2020 to 2021. Some analysts were forecasting a $200b business by 2026 as shares of DNG and some of its peers exploded to all-time highs. My projection in tandem with industry associates comes in between $23b and $28b total revenue for 2026.

Given the ongoing, aggressive pursuit of market share by the top five sites like BetMGM and other first tie operators, I have concluded that the two leaders would lose overall share of market as it now plays out at ~60% of all revenue, to somewhere around 20% combined each.

The stabilization by that time would make both companies profitable without question. Essentially running out of new states and going head to head to maintain existing shares on top of which its first-tier competitors were gaining against them brings both to somewhere around $6.0b in revenue for DKNG and $7.2b for FD in revenue for 2025. Promotional spend would clearly shrink enough for that to happen but it can’t go away entirely. The reason: The construct of sports betting odds making and proven hold percentages against handle over many decades will always hover around 7%. With expenses under control, sports betting will be a nice adjunct to the casino or international betting business but never a bonanza.

More jokers loom in the deck for 2023.

Just days ago, after returning to Disney (DIS), CEO Iger made the first ever, tangible statement that yes, it is possible, they could consider spinning off ESPN. If that happens, it’s a mortal lock that the site will move quickly into sports betting. Better late than never, of course, but realistically late to the game.

Closer to happening:

Amidst all the current transformational chaos as the sector moves out of Phase One to Phase two, we have the imminent probability that privately held sports apparel giant Fanatics, is about to enter the betting fray. Its logic on the surface seems sound. It claims a customer base of 82m avid sports fans sliced and diced for immediate attack with the skillful marketing it has employed for team apparel.

Its website is perfectly adapted to add a betting cross-marketing promotion. Its growing valuation now seen as $25b should provide enough depth of financial resources to support big-time, over-the-top marketing. At the same time, its existing database offers great potential as a foundational customer source as was Daily Fantasy Sports for DKNG and FD. CEO Mitchell Rubin, who has earned the right to bloviate as his company nears an IPO sometime in 2023, has declared war on the sector by predicting Fanatics Bets or whatever he will call his site, will become #1 in the space.

Good luck Mitch. But sorry to say, my sainted grandfather used to reply to friends who bragged about how their businesses would spin mountains of gold against competitors, “This guy is smoking herrings…” I’m afraid Mr. Rubin may be processing the same fish with that robust forecast.

This is not to imply that a Fanatics sports betting site will not have real-world potential. Its main characteristic, the one we like best, is its similarity to Barstool Sports. PENN Entertainment, Inc. (PENN) bought Barstool because it gave them low-cost access to Dave Portnoy’s 55m stoolies. It never pretended to become a market share leader. It did focus on initial spend, slowing, coming down to earth, pushing cross-over users from the stoolie data base. That seems to us to be a smart business model for Fanatics.

They won’t have a moat, but the very nature of their business would suggest many promotional variables to the current MOs of the pack. For example, they could offer winners a choice between cashing out money, or using their winnings for merchandise. Ex: You have $200 in your account as wins. So you have a choice of the cash or a great team jersey for your kid. The kicker here of course is that Fanatics redeems at retail, but buys inventory at cost. The company keeps the vigorish in between and the customer is happy.

That makes great sense and brings a dimension to the site others can’t readily copy, especially if you decide to discount the merchandise paid to winners. That’s just a thought among many we believe Rubin and his savvy cohorts can pursue to differentiate Fanatics from the pack. But in the end its hardly a path to leadership above DKNG and FD and other first-tier shops. To be frank, Fanatics is very late to the party-four years in fact. Playing catchup ball won’t be easy or cheap against deep-seated veteran brands in the sports betting space.

Given that, the entry of Fanatics in a business which already has 90 competitors in the process of either being squeezed out, or leaving the field of battle altogether because there is no victory in continuing EBITDA losses, Fanatics has no secret sauce. It will, however, disrupt the state of play and probably wind up accelerating the exit of the ultra-marginal players in the space.

Why sell DKNG?

There is a real case to be made, admittedly a bear scenario but only that, which suggests that in the current mindset of its management, DKNG will never make any money worthy of a significantly higher valuation to its stock. A more bullish scenario goes something like this: DKNG will remain among the leadership group. But even if it sustains the mathematically proven house edge of 7% through its growth path, it will face continuing, disruptive intrusions by the top-tier share leaders so promotional spend at some level will survive. It will deliver an okay performance, but by most calculations now out there as analyst PTs, it looks like a $20 a share stock at best.

So where does the yellow brick road to the all-knowing wizard lie? Clearly in either a merger with a brick-and-mortar gaming operator, or an international player which could provide the scale and ballast to contribute accretive U.S. EBITDA to a larger parent or partner. Yet, now, over 4 years into the trading of sports betting stocks, the DKNG management appears to be wedded to a strategy of more of the same. They’ve done a fine job in holding share to date, but at a cost that is unsustainable. To us, that puts the stock in a sell position now as the recession looms ever closer and the prospect of players beginning to ease up on average betting patterns gets more real.

Our calculations arrive at a far different picture for PDYPY where we believe a transaction can happen this year, that will hold a nice premium for holders that will more than compensate for the wide gap between the price of DKNG and PDYPY. Otherwise, facing recession, facing intrusions from the likes of Fanatics and possible deals among peers, what is the reason for holding the stock?

I believe DKNG still has true believers in hold patterns. Ark Investment and Vanguard still have huge positions in the stock. Whether they’ve made some nice coin on the way up, lost some back is less telling than the fact that they hang in. I have no fly on either wall. I can only assume that major holders see something I don’t. Or maybe they’re trapped into entry points that are so much above the current trading range that they are disinclined to massively reduce their positions at the moment. Or, that they are indeed part of the true believers who have bought into the mantra that DKNG’s sequential sales growth is proof enough to them that the stock will recover big time and they will clean up.

Light a novena or two, there’s hardscrabble life for DraftKings Inc. stock just ahead, and a tax loss sell now might make sense too.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment