photovs

For years, one of the most popular investments for conservative risk-average investors, such as retirees, has been utilities. There are some very good reasons for this, including the fact that these companies tend to be incredibly stable entities that typically boast dividend yields that are above many other things in the market. Unfortunately, it can be difficult to put together a diversified portfolio of these companies without having access to a considerable amount of capital. In addition, the overheated market that the country has been experiencing over much of the past decade has pushed the yields of these companies down to unremarkable levels. Fortunately, there is a solution to both of these problems. That solution is to invest in a closed-end fund that specializes in the utility sector. These funds provide access to a diversified, professionally-managed portfolio that can in many cases deliver much higher yields than any of the underlying assets possess. In this article, we will look at one of these funds, the Duff & Phelps Utility and Infrastructure Fund (NYSE:DPG). I have discussed this fund before but a year has passed since then so obviously a great many things have changed. This article will therefore focus specifically on these changes and provide an updated analysis of the fund’s financial performance. Thus, we will see if this 11.08%-yielding fund could deserve a place in your portfolio today.

About The Fund

According to the fund’s webpage, the Duff & Phelps Utility and Infrastructure Fund has the stated objective of providing its investors with a high level of total return. This is hardly surprising for an equity fund since equities are a total return instrument. After all, people that invest in these securities are typically interested in both receiving dividends and generating capital gains. The fund specifically states that it will emphasize current income as the way that it provides these returns, although capital appreciation is something that would also be nice to experience. As may be expected, the fund aims to achieve its objective by investing specifically in utilities and infrastructure providers. It does not specifically state how it defines a utility or an infrastructure provider, but as we will see in this article, this mostly includes electric, natural gas, and water utilities along with midstream energy companies, railroads, and similar companies. Basically, these are the companies that allow modern society to function in the way that we are accustomed to. It is important to note that the fund does not specifically state whether it only invests in common equities issued by these companies or if it can also purchase preferred equity from the sector. If the fund can include preferred shares, then this could help reduce its volatility somewhat since preferred equity does not usually fall as much as the common during bear markets. In addition, it will frequently have higher yields than common equity and thus could do wonders at improving the fund’s ability to generate income for its investors. On the flip side though, it also does not typically deliver much in the way of capital gains when the market is in a bullish phase.

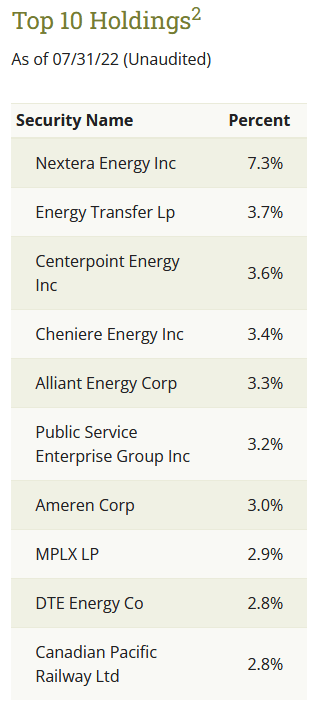

As my regular readers likely know, I have frequently discussed both utilities and midstream companies here at Seeking Alpha. As such, the largest positions in the fund will likely be familiar to many readers. Here they are:

Duff & Phelps

I have discussed most of these companies in the past, but admittedly not all of them. In particular, I have never discussed Canadian Pacific Railway (CP). Canadian Pacific Railway is always the only company on this list that is not a utility or a midstream company. This alone is not necessarily a problem since it does have many of the same characteristics that the other companies possess such as generally stable cash flows. After all, railroads are generally the most efficient way to transport products over land because they can transport substantially larger amounts of cargo than trucks and cargo has to be shipped over land in order for products that we want to buy to be in the local store. The case for utilities having stable cash flow is fairly self-explanatory since people typically prioritize paying their utility bills ahead of making discretionary expenses. Midstream companies typically have their cash flow guaranteed by contracts. Thus, all of these companies should prove to be reasonably stable over time.

We see a number of changes here compared to when we last looked at this fund a year ago. In fact, the only companies that were among the fund’s largest holdings last year are NextEra Energy (NEE) and Ameren Corporation (AEE). Every other position was added over the past year. This may make us think that the fund has a fairly high turnover, which could be concerning for some investors. This is because it costs money to actively change positions in a portfolio, which the stockholders have to pay for. Index funds have become popular for precisely this reason as their lack of much in the way of portfolio changes allows them to have considerably lower expenses than actively-managed funds. This does not mean that a fund that does a lot of asset trading will have lower performance but it does mean that management has a much harder job to cover costs and beating the index. With that said, the Duff & Phelps Utility and Infrastructure Fund has an annual turnover of 45.00%. This is not particularly high for an equity closed-end fund, although it is still substantially higher than an index fund. It’s also worth noting that the fund’s annual turnover was 50.00% the last time that we looked at it so it appears that management is reducing trading activity.

As my regular readers on the topic of closed-end funds are likely well aware, I do not generally like to see any position in a fund account for more than 5% of the fund’s total portfolio. This is because that is approximately the level at which a position begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is the risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification, but if the asset accounts for too much of the portfolio, then this risk will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market itself does not, and if it accounts for too much of the portfolio then it may end up dragging the entire portfolio down with it. I demonstrated how this can be an issue in a recent article. We can see above that only one position, NextEra Energy, is above this 5% threshold as of the time of writing. This may be concerning as NextEra Energy appears to be somewhat overvalued at the current price, which has been shown in numerous articles that have been published on this site over the past few months. Thus, we may see this company fall somewhat farther than a less highly-valued stock should we enter into a prolonged bear market. Investors should keep this in mind and be sure that they are willing to be exposed to the risks of this particular company before making an investment in the fund.

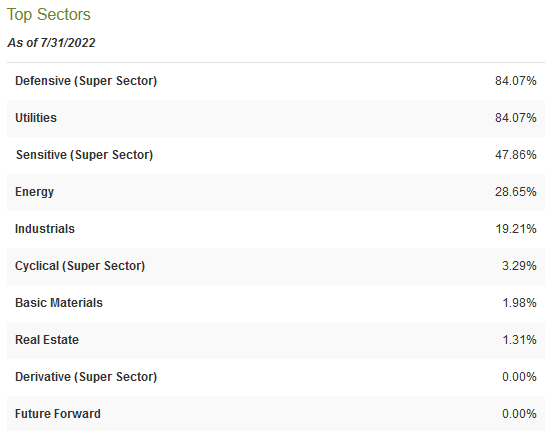

As stated earlier, the Duff and Phelps Utility and Infrastructure Fund invests in utilities, midstream companies, and other types of infrastructure firms. We saw that earlier just by looking at the fund’s largest positions list. However, the overwhelming majority of the fund’s portfolio is invested in utility companies:

CEF Connect

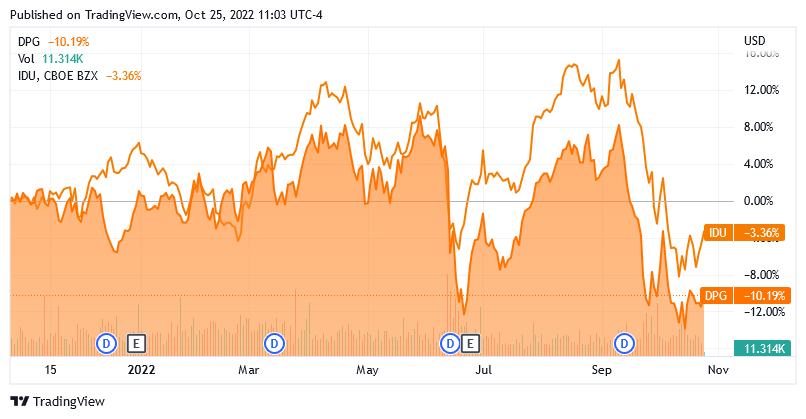

As we can clearly see, 84.07% of the fund is invested in utilities, a sector weighting that dwarfs any other. As such, we can benchmark it against the utility index to measure its performance. Unfortunately, the Duff & Phelps Fund does not do too well here. Over the past twelve months, the fund has lost 10.19%, which is substantially worse than the 3.36% loss suffered by the utility index:

Seeking Alpha

The fact that the Duff & Phelps Fund has a substantially higher yield does help to offset this somewhat but overall, the index fund did still deliver a higher total return over the twelve-month period. With that said, the index is not a perfect comparison for two reasons:

The index fund invests only in utilities while the closed-end fund invests in things outside of the traditional utility space such as midstream companies, railroads, toll roads, and similar businesses. The index fund only invests in American companies but the closed-end fund is a global fund.

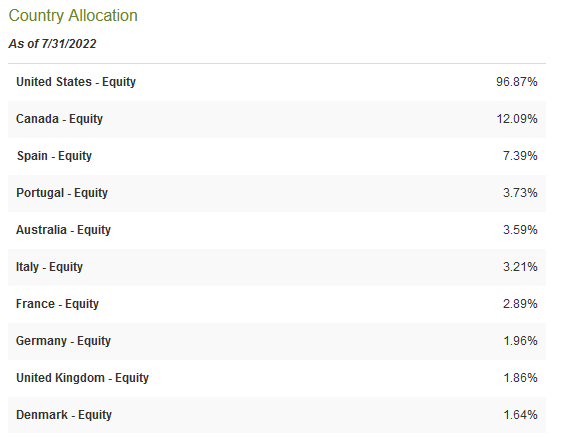

As just stated, the Duff & Phelps Utility and Infrastructure Fund invests in both domestic and foreign equities. This is an important difference because American equities have outperformed equities in many other nations. This is especially noticeable when we compare the United States to Europe. The S&P 500 index (SPY) is down 15.98% over the past twelve months but the iShares Europe ETF (IEV) is down 25.27% over the same period. Thus, the foreign stocks held by the fund may be dragging down its performance relative to the index. It may be some comfort to potential investors that the fund is currently very heavily invested in the United States, though:

CEF Connect

As we can see, 96.87% of the fund is currently invested in the United States, which dwarfs its weighting to any other nation. This is something that is nice to see in the current market environment considering that the challenges facing the American economy today are much less than those facing Europe or much of Asia. The fact that the fund is a global fund also brings certain advantages in that the fund can move its money to other nations should their fundamentals begin to improve relative to the United States. This is one advantage of active management and it is something that is worth considering before deciding whether to invest in the index fund over the closed-end fund.

Leverage

As stated in the introduction, closed-end funds like the Duff & Phelps Utility and Infrastructure Fund can use certain strategies to boost their yields above what the underlying assets actually possess. One of these strategies is the use of leverage. Basically, the fund borrows money and then uses the borrowed money to buy stocks issued by utility and infrastructure companies. As long as the purchased stock delivers a higher total return, then this strategy works quite well to boost the overall return of the portfolio. As the fund can borrow at institutional rates, which tend to be much lower than retail rates, this will normally be the case. However, the use of leverage is a double-edged sword because it boosts both gains and losses. Thus, we want to make sure that the fund is not using too much leverage since that would expose us to too much risk. I generally do not like to see a fund have leverage exceeding a third of the value of its assets for this reason. The Duff & Phelps Utility and Infrastructure Fund meets this requirement as of the time of writing as the fund’s current leverage ratio is only 32.52% of its assets. Thus, the fund appears to be maintaining a reasonable balance between risk and return.

Distribution Analysis

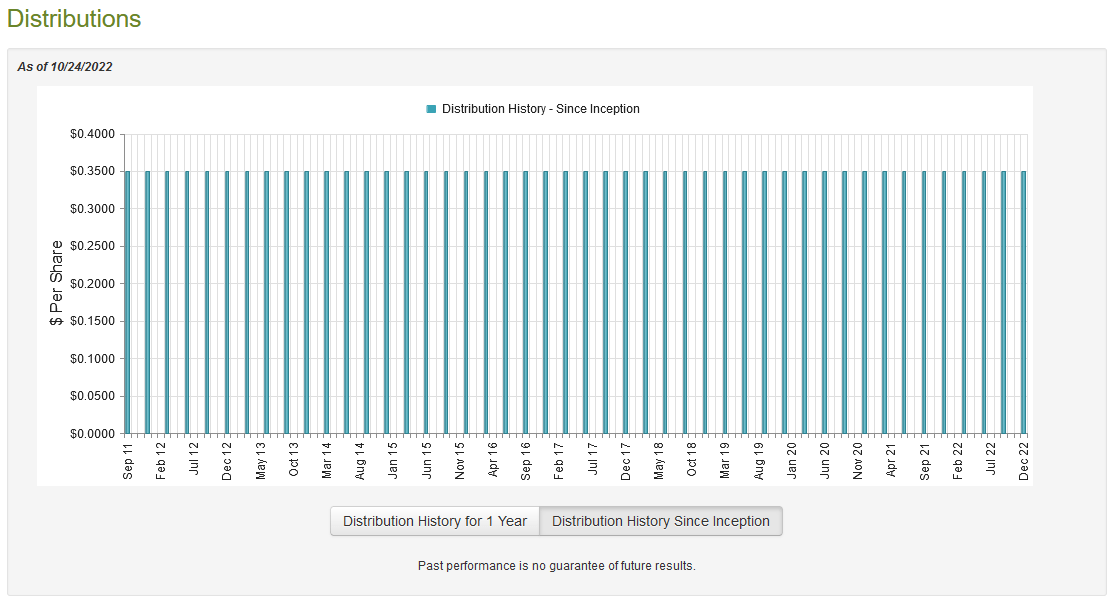

One reason why investors like utilities is that these companies tend to have higher yields than most other things in the market. In addition, the Duff & Phelps Utility and Infrastructure Fund specifically states that it aims to deliver its total return to investors in the form of current income. As such, we can likely assume that the fund boasts a reasonably high distribution yield. This is indeed the case as the fund currently pays out a quarterly distribution of $0.35 per share ($1.40 per share annually), which gives it an 11.08% yield at the current price. This is obviously substantially higher than the 1.63% yield of the S&P 500 index and it is even well above the 2.51% yield of the aforementioned iShares U.S. Utilities ETF. The fund has been remarkably consistent in its distribution over the years. In fact, it is one of the only funds that has never changed its distribution since its inception:

CEF Connect

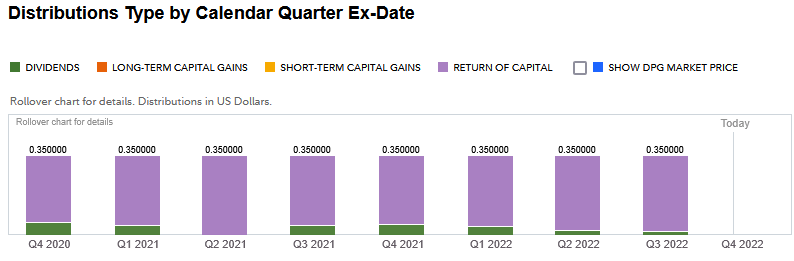

This will undoubtedly appeal to anyone that is looking for a steady and consistent source of income to use to pay their bills. Unfortunately, the fact that it has not increased its distribution also means that the fund’s distributions have been constantly losing purchasing power with the passage of time unless the distribution is reinvested. This is something that could be a problem in today’s inflationary environment. It is also difficult to understand how the fund has shown such consistency over the years when very few other funds have managed this feat. The fact that a sizable proportion of the fund’s recent distributions are considered to be a return of capital exacerbates these concerns:

Fidelity Investments

The reason why this may be concerning is that a return of capital can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to qualify as a return of capital, such as the distribution of money received from partnerships or the distribution of unrealized capital gains. These are both things that this fund might be doing. As such, we should have a look at the fund’s finances to figure out how it is financing these distributions and determine exactly how sustainable they are likely to be.

Unfortunately, we do not have a particularly recent report to use for that purpose. The fund’s most recent financial report corresponds to the six-month period ending April 30, 2022. As such, it will not give us much insight into the fund’s performance over the past few months. It will however tell us how the fund handled the market turmoil in the first four months of this year. During the six-month period, the Duff & Phelps Utility and Infrastructure Fund brought in a total of $13,177,097 in dividends from the assets in its portfolio. However, $5,678,266 of that came from the various master limited partnerships that the fund holds and so was considered to be a return of capital and not income. This gives the fund a total income of $7,498,831. It paid its expenses out of this amount, leaving it with $1,918,905 available for the shareholders. This was nowhere close to enough to cover the $26,605,021 that the fund actually paid out in distributions during the same period, however. This is certainly something that is quite concerning at first glance.

However, there are other methods that the fund can utilize in order to obtain the money that it needs to cover its distributions. The first one that comes to mind is capital gains. Fortunately, the fund enjoyed some success at this during the period. The Duff & Phelps Utility and Infrastructure Fund realized $19,382,342 in net capital gains and had another $10,683,304 in unrealized capital appreciation over the period. This is a fairly impressive result considering the steep market decline that we saw in April 2022. It was also enough to cover the distributions and overall, the fund saw its net assets increase by $6,210,743 even after paying the distributions. Thus, it does appear that the distributions are sustainable and investors do not really need to worry about the return of capital classification.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Duff & Phelps Utility and Infrastructure Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can obtain them at a price that is less than the net asset value. That is because this scenario implies that we are acquiring the fund’s assets for less than they are actually worth. That is unfortunately not the case with this fund today. As of October 24, 2022 (the most recent date for which data is currently available), the Duff & Phelps Utility and Infrastructure Fund had a net asset value of $11.44 per share but the shares currently trade for $12.89 per share. This gives the fund a 12.67% premium to net asset value, which is an incredibly expensive price to pay for any closed-end fund. This current price is also substantially above the 11.89% premium that it has traded on average over the past month. Overall, this greatly decreases my interest in what would otherwise be a fairly impressive fund. That price is simply too high to justify an investment.

Conclusion

In conclusion, utilities and infrastructure companies are likely fairly decent places to be as the economic conditions in the United States continue to worsen. The Duff & Phelps Utility and Infrastructure Fund provides a reasonably decent way to get diversified exposure to the sector and receive a high yield in the process. Unfortunately, the fund’s valuation is far too high to justify an investment currently. This fund also has underperformed the index fairly dramatically over the past year, which could be a problem for those investors that are desperate for the preservation of capital. Overall, there are worse funds out there though and I would be willing to consider this one if the price were more reasonable.

Be the first to comment