AsiaVision

Investment Thesis

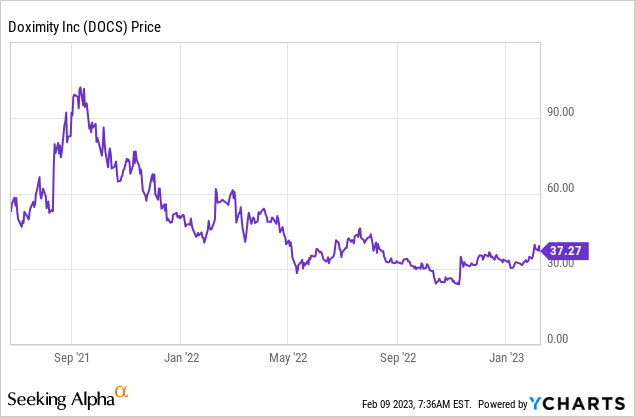

Doximity (NYSE:DOCS) is a US-based healthcare technology company founded in 2010. It went public in 2021 but the stock has been performing badly due to macro headwinds and is now down over 60% from its all-time high.

The company operates as an integrated healthcare platform and has a large addressable market with a low penetration rate. It is also already profitable with attractive margins, which is rare among high-growth companies. However, despite the large drop in share price, its valuation is still pretty stretched and growth rates are likely to slow down. This is indicated in its latest earnings as revenue growth was soft while guidance also came in below consensus. I do not see much upside from the current price therefore I rate the company as a hold.

Why Doximity?

Doximity is a digital platform for physicians. The company offers multiple products that are purpose-built for the healthcare industry. This includes telehealth, newsfeed, professional network, scheduling, digital fax, and e-signature. Physicians prefer it as it integrates everything together, significantly enhancing efficiency and consistency. They now don’t have to go Zoom (ZM) for telehealth, then DocuSign (DOCU) for signatures, and LinkedIn for networking as it is all in one place.

On the commercial end, its marketing solution is another fast-growing product as the company has a very valuable and targeted customer base. It is seeing strong demand from pharmaceutical and health system companies as they are able to specifically target physicians to improve ROI (return on investments). For example, IQVIA (IQV) reported a ROI of 11:1 from the product.

Doximity

The TAM (total addressable market) for the space is pretty big. According to Doximity, its TAM is estimated to be around $18.5 billion, with marketing and staffing accounting for $14.3 billion while telehealth software accounting for $4.3 billion. Its current penetration rate is only 2.3% which provides ample room for expansion.

The market has been growing rapidly as the healthcare industry is extremely dated with legacy technologies. It is pretty surprising that 80% of healthcare documents are still being sent via snail mail and fax. Healthcare professionals should not have to waste their precious time dealing with inefficient admin tools. The industry is poised for a digital transformation and should provide strong tailwinds for the company.

Doximity

Q3 Earnings

Doximity just reported its third-quarter earnings and the results are quite disappointing, as growth rates slowed while operating margin contracted. The company reported revenue of $115.3 million, up 18% YoY (year over year) from $97.9 million. Gross profit was $101.7 million compared to $86.8 million, up 17.2% YoY. The gross profit margin was steady at roughly 88%. The growth is mainly driven by the land and expand strategy, as the net revenue retention rate came in at 117%. The figure for the top 20 customers was even higher at 127%. Customers with over $100,000 in annual revenue also increased by 12% from 258 to 290. The growth rates have slowed significantly compared to last quarter which recorded a 28.8% revenue growth. Management said this is due to a launch delay but they did not how big the impact was.

Anna Bryson, CFO, on delayed launch

Our revised fiscal 2023 outlook is primarily the result of new product launch delays. Simply put, content approval has taken more time due to the novel formats of our new point-of-care and peer-to-peer offerings. These delays are having a larger impact on our near-term revenue due to a higher mix of new products sold in Q3 than initially thought. We do expect to have this content approved and ready to go live in the coming months

Besides slowing growth, the bottom line is also weak. While it is very profitable, it is not showing any operating leverage. It seems like the company is ramping up S&M (sales and marketing) spending substantially because it needs to maintain growth rates. While revenue was up 18%, S&M expenses were actually up 29% YoY to $33.2 million. R&D (research and development) expenses also increased 26.5% YoY to $20.5 million. Total operating expenses increased 24.1% from $51 million to $63 million. Due to heavy spending, operating income only increased by 7.5% YoY from $35.8 million to $38.5 million. The operating margin decreased from 36.6% to 33.4%. EPS for the quarter was $0.16 compared to $0.26, down 38.4%, but this isn’t really comparable due to the difference in income taxes. The company expects FY23 revenue to be between $417.7 million and $418.7 million, below the consensus of $428.3 million. I expected more and this quarter is a let-down in my opinion. I hope revenue growth will reaccelerate once they sort out their product launch delay.

Investor Takeaway

I like Doximity’s products and prospects as the massive healthcare industry is poised for transformation and the company is able to provide a modern integrated solution for physicians. However, I do not like its latest results and valuation. Its third-quarter earnings result is not what you want to see from a growth company. Growth slowed significantly from the high twenties to the high teens while operating expenses increased significantly in order to support growth. No operating leverage is shown and the operating margin also contracted meaningfully. The product delay may have affected growth, but honestly, I didn’t think the impact would be this big. Despite the drop in share price, the company is still trading at an fwd PE ratio of 54.02x which is expensive, especially when considering the deceleration in growth rates. I do not think there will be much upside potential until the company starts to show better performance once again. Therefore I rate Doximity as a hold.

Be the first to comment