Sundry Photography

Dear readers/followers,

Dolby (NYSE:DLB) is a hard company to be negative on, given the fundamental strength of its overall portfolio. It adds to this by being not timeless, but close to market-dominating in a way that almost makes its portfolio appeal timeless.

I’ve reviewed Dolby twice before – each time, the company has failed to reach the mark of buyability. Let’s review the latest results and see if anything has changed here.

Updating on Dolby Labs.

Dolby Labs, a company that has been publicly traded for about 17 years, is the company that owns most of the theatre and home sound technologies we take for granted today. It’s a pretty self-sufficient business that doesn’t do a whole lot of M&As but acquired Doremi Labs for $92.5M back in 2014. Overall, the company holds dozens of technologies for analog and digital noise reduction, encoding, compression, Audio and Video processing, and digital cinema.

The business is easily understood and easy to explain – improves sight and sound, delivering solutions to create experiences across consumer and specialty industries.

At its heart, Dolby is a business that Mr. Wonderful – Kevin O’Leary might approve of – it’s mostly a licensing business. That means that the company basically just collects licensing fees, which represent its annual revenues. For Dolby, that’s most of their business – around 90% of this.

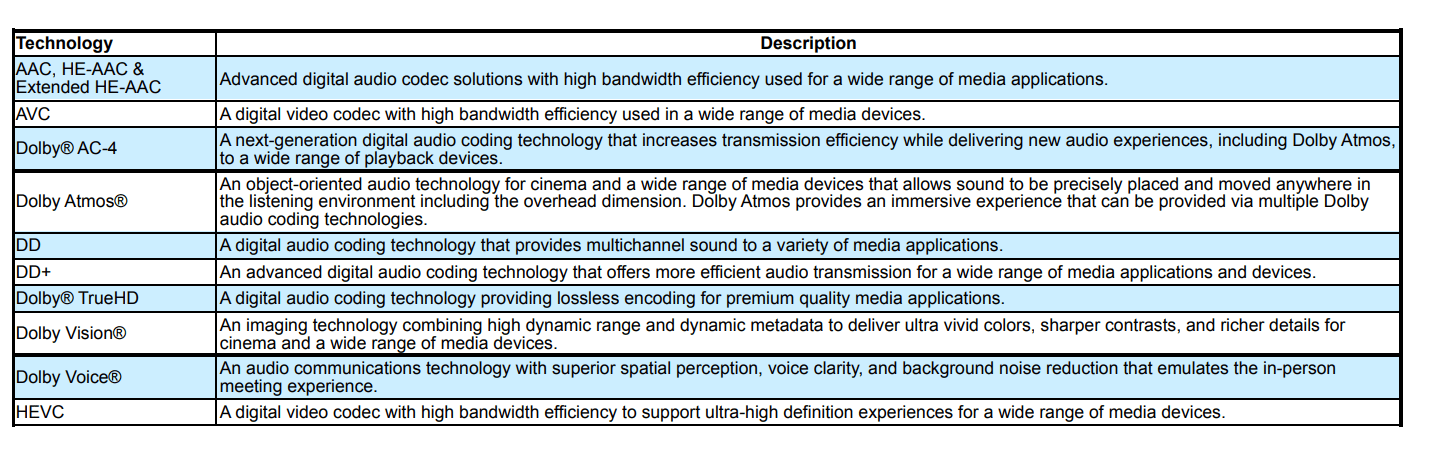

This is a selection of licensed business areas.

Dolby Licensing (Dolby 10-K)

The composition in turn of these licensing fees comes mostly from broadcast- meaning television and the like, as well as mobile licensing. Another 25-30% comes from CEs (Disc devices, Soundbars, DVDs) and PCs (MAC/Windows-based OS), as well as the smallest from gaming consoles, auto DVDs and Cinema.

Wherever there is a Dolby Logo, there is a small amount of money going to Dolby Labs in licensing, in one of the company’s models, using integrated or patent licensing. Most of the customers use a two-tier licensing model, where the company’s decoding tech is provided to semi-manufactures, which implement the tech, which in turn are sold to OEMs.

Dolby considers the former “Implementation Licensees” and the second “System Licensees”, where the latter obtain licenses from Dolby that allow them to make and sell user-end products which the former have integrated Dolby tech into.

A very profitable model for Dolby. The second model is the fully integrated model, where one company does both. There is also the patent licensing model, where Dolby uses more standard patent pools (arrangement between multiple patent owners to jointly offer and license pooled patents to licensees. Dolby also licenses patents directly to manufacturers that use our IP in their products.

The company has over 13,200 patents, with another 4,100 pending in over 100 legal jurisdictions across the planet. The patents currently have expiration in May 2045, meaning around 25 more years of exclusive business, which is a massive moat to consider when looking at the company.

Pro-Dolby arguments circle around the company’s ubiquitous nature, which I view as unlikely to change for the foreseeable future, given that recent trends have more often resulted in more of the company’s tech being used in devices, as opposed to less.

The company’s technologies are common enough that they’re used in a mandated fashion, including things like mandated DD+ in most parts of Europe, DDD+ in most streaming services, and DD being mandated in most HD-region including NA. Also, AC-4, the next generation of audio coding, has been adopted for implementation as a standard in North America, Europe, and LATAM. TV manufacturers are also using it and are adopting it to a higher degree.

Recent results for Dolby are the 4Q22, where they closed to books for the year. The company saw slight revenue declines YOY, with GAAP income of around half the 2021 results, and cash flows lower than 2021 as well. The company was still cash-heavy, holding around $911M in investment, equivalents, and pure cash.

The main challenge for Dolby this last quarter was the reduction in overall shipments due to lower demand and SCM challenges. Consumer devices have seen lower numbers, and with this come some challenges because everything in terms of licensing for Dolby is based on volume.

So when volume falls, so do earnings.

Transactions are taking longer times, so the whole environment is characterized by pressures at this time.

Dolby isn’t sitting inactive of course – it’s pushing development in key TV and movie technologies, and Dolby Vision and Atmos are growing in terms of increased content across both services and other device categories.

Atmos is seeing good traction as well, and the overall digital ecosystem is still driving the underlying trends upwards. But Dolby isn’t immune to the chaos that’s going on in the world.

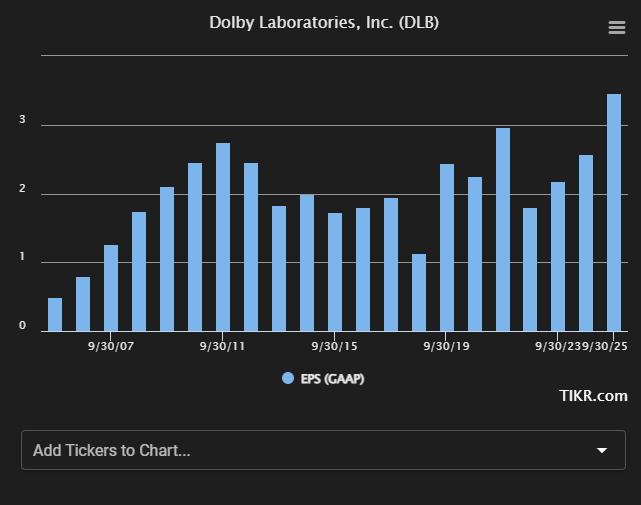

We could call Dolby’s EPS stable, but that would be a lie. The fact is, the company is showing a decent amount of cyclicality not only in its short-term but longer-term trends.

Dolby EPS + Forecast (Tikr.com)

This makes Dolby a continued, tricky investment. Volatility like this isn’t easy, because it also translates into the share price, even if the share price overall has mostly seen growth. The company’s yield also isn’t very impressive at all, though it has been growing over time and currently is at around 1.45%.

This is not a rare opinion for me to hold. Most of the pieces on Dolby featured on SA are neutral, and the one bullish piece since late 2020 has seen negative RoR of 13.82% in a period when the S&P500 is up nearly 8%, a clear underperformance.

There is, therefore, a reason for the ratings we currently hold on this stock, and a positive net cash position isn’t enough to make me positive here – neither is what is undoubted industry dominance. Positive ratings require more than this for me.

Still, I do believe that Dolby ended the year strong enough, and I do see similar trends to the analysts here, that IoT, more digital, and the current trajectory of the audiovisual sector across multiple media channels and devices are bound to send the company’s income upward.

Let’s look at Dolby’s valuation.

Dolby’s Valuation

So, recap here. Dolby typically trades at a range of around 25-30X to earnings on a normalized basis.

This is not something I usually like to see, but for Dolby given its portfolio, it can be understood and even considered valid, due to the strength of the overall portfolio.

Still, the earnings aren’t as stable as we might want and as we saw above, given the cadence of licensing revenues (due to the market exposure) and how they’re coming in. In 2018, EPS dropped by 42%, only to grow by 114%, and in 2022, the company is expected to see another decline of close to 30%.

Dolby is rocky, to say the least, but we’re starting to see a potential upside to the company if we look over the very long term.

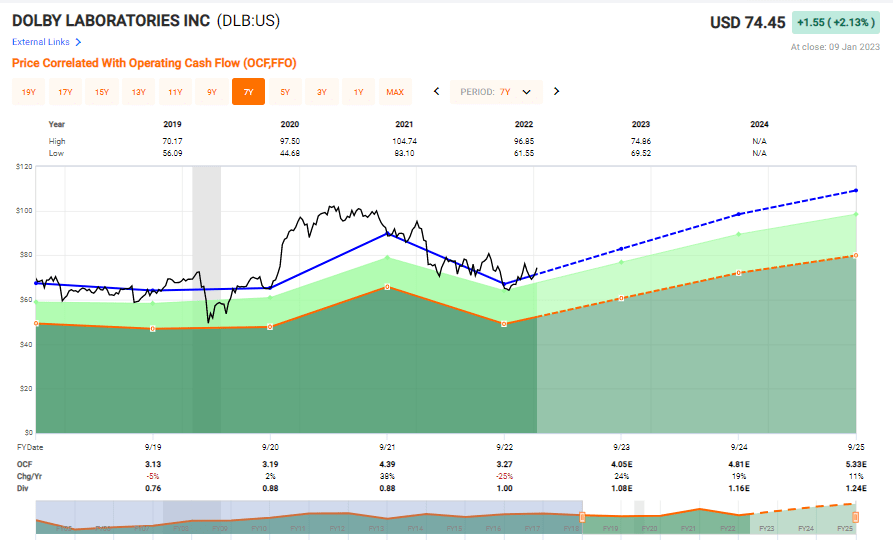

Dolby Valuation (FAST Graphs)

At the right decline now, there’s a compelling valuation to be had – though we’re looking to discount it even more here. Analyst accuracy isn’t the best thing for Dolby – they miss around 33% of the time negatively on a 2-year basis with a double-digit margin of error. So I’d want to buy Dolby not necessarily at 15x P/E, because history has shown it rarely drops to this, but around 16-17x P/E normalized.

Assuming a 15-17x P/E forward range, we’re seeing a potential annual RoR of around 5-10% here, which is starting to look interesting. If the company was to drop down to 16-18x P/E, that upside would increase to around 10-18%, which would be enough to get me buying Dolby, despite the lack of a credit rating and the low, sub-2% yield.

Dolby is the sort of moat-inherent sort of company that I would look to invest in if it traded at 20-30% lower than it is today, but I wouldn’t be all that interested in where it’s trading today.

The difference between many of the large-cap companies is that they may actually quickly drop back down to these levels, which is why I’m writing about it and establishing a target here.

Simply put, it’s still too expensive here – but unlike articles before, there is a positive scenario that can really be considered for the company.

Dolby’s expectations are still based on a bullish thesis that might not materialize even close to as positively as is expected, given the cyclicality we’ve been seeing. Current analyst averages are around $93/share, which comes from a range of $80 on the low side to $116 on the high side – a relatively tight range, which makes the case for a “BUY” rating if you allow for the premium for Dolby.

The reason I don’t is that history has shown that doing so is a good way to get sub-par overall rates of return, which is definitely not what I am looking for. The average upside to PT here is 25%, but my own PT for the company is lower.

My initial target for the company was a $70/share PT. I’m not moving from it – here is my current thesis on Dolby.

Thesis

- Dolby is a fundamentally sound, well-run company with a solid moat. It lacks the usual dividend safety and tradition as well as credit rating, but its portfolio of patents makes for revenue security for the next few decades. I view it as a sound investment at the right price.

- Given the company’s moat and premiums, I consider 20-25X P/E to be valid for Dolby, but 15-18x P/E to be a preferable one.

- This calls for a current 2022E share price of $70 and a 2023E share price of $80, making the company slightly overvalued and a “HOLD” here.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion. The company is yet to fulfill single one of my criteria which is why I view it as a “Hold” here.

Be the first to comment