Sean Anthony Eddy

Investment Thesis

DLH Holdings Corp (NASDAQ:DLHC) recently announced solid FY22 and Q4 FY22 results. Their revenues and net income grew significantly. In this thesis, I will analyze the financial results and talk about their recent acquisitions and what will be its impact on the company. In my opinion, they are undervalued, and it is a great buying opportunity.

About DLHC

DLHC experts in public health and health operations. They solve the complex problems military customers and civilians face using artificial intelligence, cloud-based applications, and advanced analytics. They also provide various human services and solutions like data collection and management, IT system architecture design, and social health assessments. In addition, it offers life science services like disease prevention, clinical trials, and health informatics analyses to underserved communities at risk through strategic communication campaigns. DLHC was incorporated in 1969 and headquartered in Atlanta, Georgia.

Financial Analysis

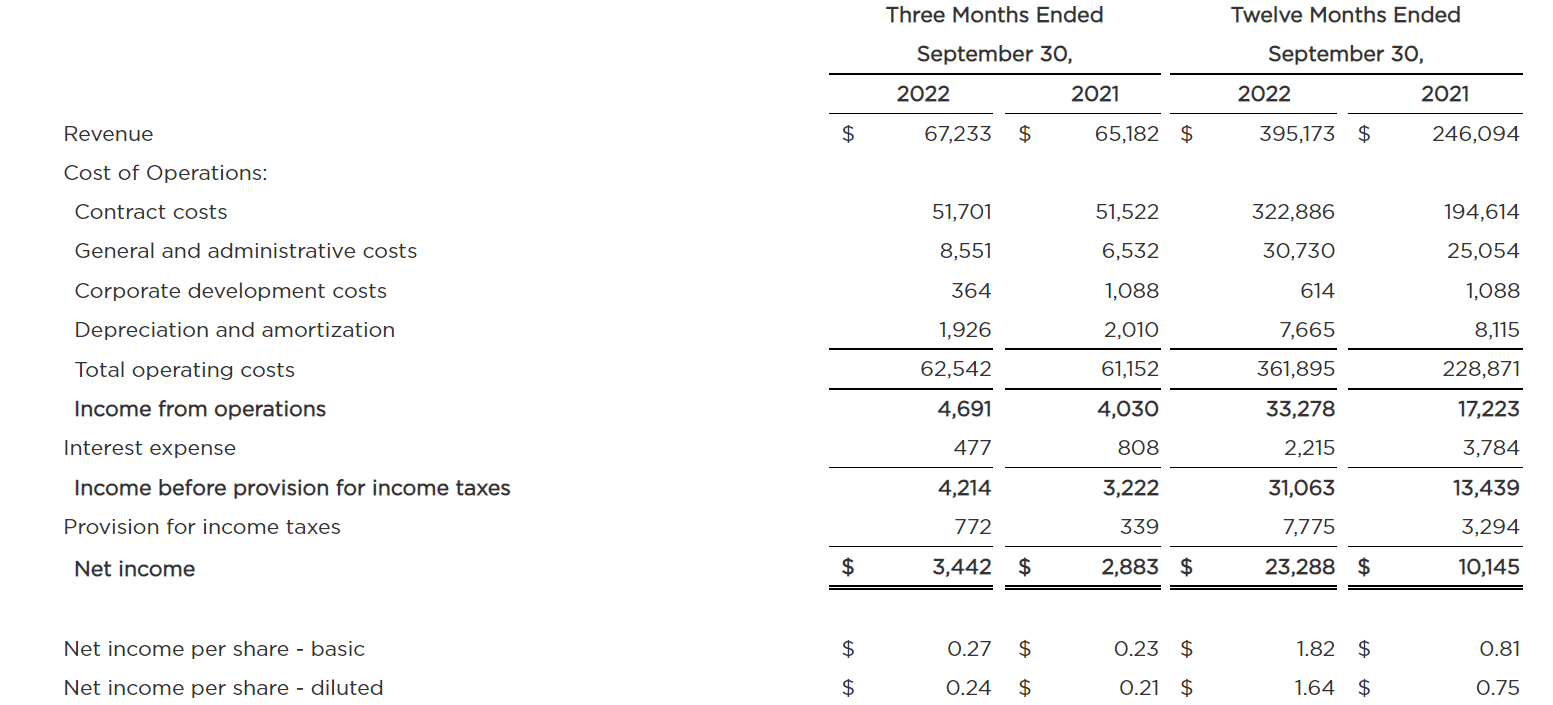

DLHC recently announced its FY22 annual and Q4 FY22 results, and in my view, it’s quite impressive. They beat the Q4 FY22 market EPS estimates by 4.68%, and the Q4 FY22 revenue estimates were in line with market expectations. The reported revenue for FY22 was $395.1 million, an increase of 60.5% compared to the revenue of FY21. I think the primary reason behind this increase was the FEMA contract which contributed $126 million in FY22. Under the FEMA contract, the company provides support in Alaska for those seeking temporary hospital support during the covid pandemic. They are placing experienced medical staff in communities throughout Alaska. The reported net income for FY22 was $23.2 million, an increase of 129.5% compared to FY21. I believe the main reason behind the increased net income is the investments done by the company in the human capital and business development functions. The reported diluted EPS for FY22 was $1.64, an increase of 118.6% compared to FY21.

DLHC’s Investor Relations

Talking about the Q4 FY22 results, the reported revenue for Q4 FY22 was $67.2 million, an increase of 3.1% compared to the corresponding quarter of last year. The net income for Q4 FY22 was $3.4 million, an increase of 19.3% compared to Q4 FY22. I believe the primary reason behind this increase was the improved program mix and decrease in interest expense. The diluted EPS for Q4 FY22 also grew by 14.2% compared to Q4 FY21. Overall, the financial performance of DLHC in FY22 was impressive, and I believe they will continue to do better in upcoming quarters.

Technical Analysis

Trading View

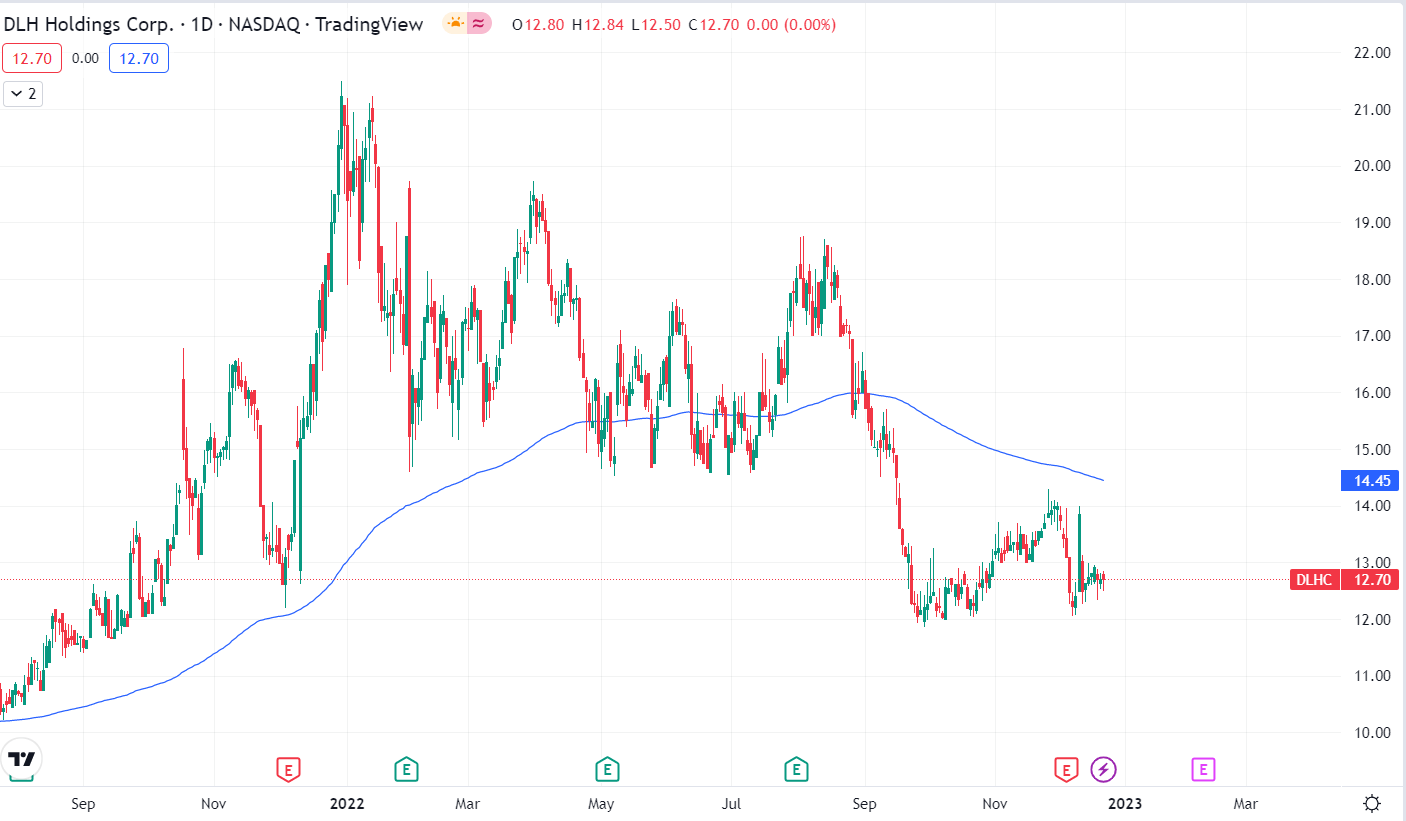

Currently, DLHC is trading at the level of $12.7 and is below its 200 ema, which is at $14.5 in a daily time frame. When a stock is trading below its 200 ema, it is considered in a downtrend. In last one year, the stock has corrected 40%, and now it is trading near a crucial support level of $12. If the stock breaks the level of $12 in a daily time frame, we can see the stock fall to the level of $9, but if it sustains the level of $12, we can see an upside rally up to the level of $18. In my opinion, DLHC can provide us with a great short-term risk-to-reward ratio trade one can enter the stock at the level of $12 with a stop loss of $11 and a target of $15. One can also buy the shares of DLHC at the level of $12 for long-term investment purposes.

Should One Invest In DLHC?

Recently DLHC has acquired privately held Grove Resource Solutions (GRSI). They have opted for a syndicated term loan of $190 million and credit facility of $70 million to fund the acquisition. This acquisition will surely have an impact on its balance sheet but I believe the company currently has a low debt liability and I believe they will efficiently manage this debt given the higher expected earnings from the acquisition. This acquisition will surely increase the interest burden on the company but I think the significant earnings growth expected from the acquisition will largely offset the interest expense. So, I think this is a smart strategic move by them. GRSI workforce features some of the best technology leaders in the industry. GRSI has 700 trained employees and provides cyber security solutions to civilians, the U.S. navy, and the National Institute of Health (NIH). The company acquired GRSI for $185 million, and with this acquisition, the company is strengthening its information technology and engineering capabilities diversifying its portfolio. The management has estimated that GRSI will contribute annual revenue of up to $140 million to the company. GRSI is well known for its IT and technical capabilities and with this acquisition it will help DLHC show their aggressive and dedicated nature toward the company’s growth.

They have three-year revenue growth (CAGR) of 35%- and three-year diluted EPS (CAGR) of 58.7%. This shows that they are constantly giving healthy returns and are on the right growth track. With the recent acquisitions and improved workforce, I think it will maintain its growth trajectory.

DLHC has an A valuation grade by the Quant. They have forward GAAP P/E ratio of 15.75x compared to the sector ration of 17.70x which shows that they are undervalued. In my opinion PEG ratio is a better valuation method for growth companies. PEG ratio between 0.5-1 is considered good and below 0.5 it is considered ideal for a company showing that the company is undervalued. They have a PEG GAAP (TTM) ratio of 0.07x compared to the industry PEG GAAP (TTM) ratio of 0.38x showing that they are currently undervalued when compared to its peers. They also have Price/Sales (FWD) ratio of 0.42x compared to the industry ratio of 1.23x. With covid cases rising again globally there might be a boost in their revenue and I think they might provide significant returns in FY23. Their growth aspect looks promising, and after correcting more than 40% in last one year they are currently trading at a discounted price, so I think it is a great buying opportunity.

Risk

High Dependence

They derive 99% of their revenues from agencies of the Federal government. The high dependence can be a matter of concern because of the small business administration program (SBA) the government prefers veteran and minority-owned businesses for the contracts. So, if the government ceased doing business with them, then they might lose their contracts which can severely impact their business and revenue. But they are taking adequate steps to tackle this situation; they have developed strong relations with their new customers like VA and HHS, which will provide various numbers of small contracts that will significantly contribute to its revenue.

Bottom Line

In my view, it is a high-growth and promising company. They are looking fundamentally strong, and their revenues are growing every quarter, which is a positive sign. In addition, they are currently undervalued according to the industry standards, and they are trading at a discounted price, providing us with a great buying opportunity. So, after analyzing all the aspects, I assign a buy rating on DLHC.

Be the first to comment