Vera Tikhonova/iStock Editorial via Getty Images

Disney has dropped a lot, but this is not always an indicator of “cheap”

Down 45% from its all-time high, The Walt Disney Company (NYSE:DIS) is a stock that has been getting cheap, with buy ratings left and right all over the internet. For me, I can see the value in the assets being irreplaceable as well as their IP. The nostalgia of the Disney franchise just doesn’t seem to fade, regardless of the amount of time that has lapsed. Even to this day, the classic Snow White and Cinderella movies are enjoyable even for children that have grown up watching CGI films. The company going into Covid, unfortunately, showed just how vulnerable their business is to global macro turmoil. To hedge this, Disney has made a wide foray into the direct-to-consumer streaming video business.

This stock in my eyes is both a comeback story and a bit of a business pivot into less vulnerable areas of commerce should travel be disrupted again. After digging into the balance sheet and income statements, I see some good and some bad. Even though Disney stock has dropped a lot, I am not going to slap a buy rating on it just yet. This is a hold based on my below analysis.

Direct-to-consumer business to the rescue

Disney 2021 10K

The meat of Disney’s wholly owned direct-to-consumer video platform can be seen above. The company also owns interests in a variety of local market broadcasting stations. Furthermore, Disney has a controlling stake in Hulu. Combined with Disney plus, this forms a formidable opponent to Netflix (NFLX), Apple + (AAPL), Amazon (AMZN) Prime, and Paramount plus (PARA). The Hulu ownership structure is laid out as follows (from the 2021 10-K):

The Company has a 67% ownership interest in and full operational control of Hulu. NBC Universal (NBCU) owns the remaining 33% of Hulu. The Company has a put/call agreement with NBCU, which provides NBCU the option to require the Company to purchase NBCU’s interest in Hulu and the Company the option to require NBCU to sell its interest in Hulu to the Company, in both cases, beginning in January 2024 (see Note 4 of the Consolidated Financial Statements for additional information).

I’m sure that I’m leaving out more than a few media businesses in the above DTC list. All told, Disney owns more than a couple hundred businesses and brands. However, it remains that the physical assets, linear and merchandise provide the lion’s share of the profit. The diversification into DTC streaming media gets all the attention, but it will take some time before it represents a significant portion of Disney’s income. For now, user growth is the story, since subscriptions versus PPV represent the majority of Disney plus revenue. Disney is trending up while Netflix is flattening out.

Park restrictions continue abroad

Below this section, I will outline my recent experience at a domestic Disneyland with mind-blowing demand. On the flip side, Disney is still experiencing operating losses at properties in China that continue to lock down over Covid concerns. When or if this rolling lockdown situation will ever end in China is anyone’s best guess. Many were assuming major Covid lockdown policy changes might be on the horizon after the 20th National Congress, but this recent lockdown in Shanghai was actually after the congress adjourned. Luckily, both the Hong Kong and Shanghai properties are not fully owned by Disney, therefore the park operation losses are not completely borne by Disney alone. Disney has a non-controlling interest in the Hong Kong property of 48% and 43% in the Shanghai park, respectively.

While Disney can be somewhat certain of the demand forecasts for all properties outside of China, the operations in China remain a wild card.

My Magic Kingdom Experience

Having recently been to the California Magic Kingdom park, I would also like to share some personal experiences on my observations. This was a family trip during the Halloween park decoration period, therefore my experience may be a bit skewed seeing that there was most likely an unusual surge of visitors to see the Halloween affairs.

At the beginning of October, I attempted to book a ticket to the Magic Kingdom less than a week before a visit. I waited a bit too long to book and the tickets were gone by the end of the hour. The hour that my wife and I spent “thinking about it” cost us our tickets. Drats. We later decided to conjoin this trip with one we had planned to Las Vegas at the end of the month and we were able to find tickets at the end of October, but just barely. I kid you not, within 5 minutes of being on the ticket reservation page, the subsequent day that would have enabled us to have two consecutive days at the park was gone. I immediately booked our one-day trip 3 weeks before visiting.

The park itself must have incurred massive expenses related to the holiday makeover, as not only was everything Halloween-themed but the Haunted Mansion was completely changed to a “Nightmare Before Christmas” theme. The markup on food and beverage that Disney makes is massive. 50-cent bags of potato chips were $3, $5 for a pickle, and $7 for any drink including a bottle of water. Since I last visited, there were noticeably more Disney merchandise shops on every corner with unique, but overpriced apparel, toys, and memorabilia. The food quality served at Disney was laughably low quality across the board. I’m going to go out on a limb and say that the food and beverage is at least marked up 300% or more.

The new Genie plus app that park visitors use to book “fast pass” line queues is also interesting. It helps you to maximize your experience and traverse the park making bookings at rides in certain time slots that allow you to board faster. This is not only for rides but for food and beverage as well. You can click open the map, find your closest eatery, and book a meal. There is both a normal and fast pass lane for F&B. There are so many nooks and crannies at the park that they manage to fit food stalls into. I would have never known about the hidden dipped corn dog truck, but with the app, now everyone can find them. There were lines out of the wazoo to get an overpriced elementary school-quality lunch. Disney is maximizing their F&B sales with the Genie Plus app.

Again, this is all my personal experience in California. The Q4 earnings call, just released as I am writing this, indicates an overall weakening in park demand which may require discounts to increase attendance. A week before our Los Angeles trip, a friend also went to the Orlando park, reporting a mad house of attendance there as well.

Expensive on the outside, let’s look under the hood

Yahoo Finance

Disney is certainly overvalued on a TTM P/E basis at 57 X earnings. At 18.7x EV/EBITDA, the company is trading at one of its cheapest valuations, but not the cheapest. For the cheapest valuations on Disney on an EV/EBITDA basis, we would have to go back to the 1980s when Disney traded as low as 8X. In a turnaround story situation, I like to look at a few items. Peter Lynch liked to see a turnaround having an increasing cash position and a decreasing debt position.

Disney Cash trends (yahoo finance)

Cash on the mrq balance sheet for Disney stands at $12.9 Billion. From 2017-2021, we can see the cash increase trends growing quickly, from $4 Billion in 2017 to almost $16 Billion in 2021. In most circumstances, this would be positive, but Disney is in the brace position here, garnering most of the cash from Debt rather than operations. The shutdowns and furloughs combined with low-interest rates during this period had more than a few companies loading up on cash through cheap capital markets.

With free cash flow falling from $9.8 Billion in 2018 to $1.2 Billion TTM, Disney has a ways to go before it can begin to consider paying down the debt load or re-instituting the dividend.

Valuation

In turnaround situations where assets have been impaired and there may be more amortization and depreciation than normal, I like to look at how a company is growing EBITDA in the near term and compare that to the EBITDA per share. This is a modified PEG ratio. In the case of Disney, they have a TTM EBITDA of $11.9 Billion. The total shares outstanding are 1.78 Billion, giving us an EBITDA per share of $6.6 a share. With Disney currently trading at below $100, this would give us a price-to-EBITDA ratio of around 15 X. To have a fair value along this metric, we would need EBITDA to be growing at 15% per year on a trailing 5-year basis. As Disney lost about 40% of its pre-COVID EBITDA in 2020, I am just going to drill down on the growth since the earnings nadir.

Bottoming out at $9.9 Billion in 2020, over the 2 year recovery period of reopening and increases in DTC media, we can see EBITDA growing at a CAGR of 9.637% from 2020 to TTM. I will be generous and give them a multiplier of 10 instead of 9.6. I’ll also bump their EBITDA up to $7 a share to assume that will beef up in the near term as park visitation gets back to normal and inflation hopefully subsides a bit. Even in this scenario, we have a fair price of $70 a share.

Modified Graham Number

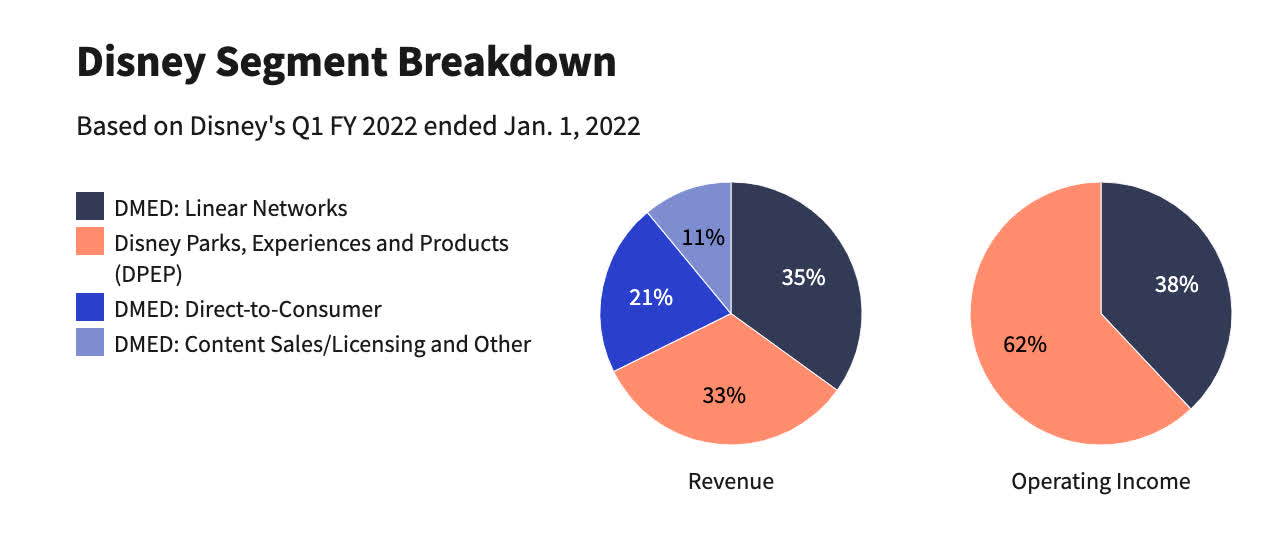

Disney Revenue and Profit (Investopedia)

Looking at the above breakdown of Disney’s revenue and operating income, we can see that the Disney story is still one highly predicated on physical properties operating efficiently. Media of all types accounts for 38% of income, while the direct-to-consumer segment is still more of a cash burner than it is a cash cow. With 62% of operating income coming from the parks, experiences, linear networks and products, let’s take a look at the value based on both the physical assets and earnings.

Taking a look at the price using a modified Graham Number substituting EBITDA per share for EPS. The Graham Number, taught in the original Intelligent Investor, is simply the SQRT of 22.5 × (Earnings Per Share) × (Book Value Per Share). Substituting $7 in EBITDA per share for EPS and using the current book value per share of $51.28, we have SQRT: 22.5 X 7 X 51.28 = $89.86. This is a useful metric when looking at companies with large amounts of tangible assets. Disney is still heavily tangible, but is beginning the shift into a semi-intangible IP / media company with more intangible assets than previous.

This is a company with irreplaceable hard assets. It would be almost impossible to acquire. You can also see that Disney is open to joint ventures, owning non-controlling interests in properties in China, as well as non-whole interests in media companies. If they ever needed to leverage their properties to grow the IP centric/media business, this is certainly an excellent route for fundraising. They can sell partial non-controlling equity interests in any of their resorts or parks, freeing up capital without diluting shareholders or borrowing at current high rates.

Debt and potential dividend return

Disney Debt Trends (yahoo finance)

As noted before, a Peter Lynch turnaround story has a couple of elements, increasing cash and cash equivalents plus decreasing debt. We can see from the above, with 2017 total debt on the right ending with 2021 total debt on the left, the trends are increasing debt levels. This is a bracing position rather than the fulcrum of a turnaround with both debt and cash increasing. This is a similar trend I am seeing in cyclical semiconductors.

Risks

More global lockdowns or international macro/geopolitical events that hinder travel will remain risks until Disney can become profitable on higher margin direct-to-consumer streaming products and other non-tangible IP. Anyone familiar with Netflix’s cash flow statements observes that while they have consistently positive earnings, they have erratic and often negative free cash flow. The streaming business is highly competitive with participants needing to spend more on forward content than their trailing income provides to keep up with the competition. Free cash flow negative businesses will not be kind as rates continue to rise and borrowing to grow any business will not be easy.

Job losses and a prolonged recession may also stoke fears that the consumer will have fewer dollars to spend on every overpriced thing that Disney provides. Their products are very discretionary, but not in line with luxury vehicles or high-end clothing. Experiences are usually the last discretionary item to be cut from the family budget.

Catalysts

The U.S. travel industry has come roaring back, and the theme park and resort profit has responded accordingly, although cooling off worldwide as of Q4 2022. An abolishment of lockdowns in China would be a catalyst, making a profit from Asia more predictable. Steep increases in streaming user growth are another obvious one. If Disney continues to double their streaming revenue YOY, regardless of the profitability, the market should respond favorably to that.

Conclusion

Disney is still overvalued on modified value ratio formulas using non-GAAP metrics. The assumptions I used were very liberal and gave Disney a bump to beef up the forward year’s EBITDA. Disney can continue to de-risk and pivot their business from an asset-heavy one to a mix of streaming media and intangible IP. However, the DTC business is still a money loser while the theme parks are a money printer.

After recently visiting Disney Land California, I realized it’s got to be tempting for Disney to continue to expand the theme park empire after witnessing the rabid demand for the product after the Covid leash has ripped off. While global visitation may be waning, the U.S. market is strong from the eyeball test. The global market, however, is a different story. Inflation is much worse in Europe and Asia as the dollar strengthens. The belt tightening abroad will be much more prevalent than the domestic pantaloons.

The fact remains, that the pandemic genie has gotten out of the bottle and it may only be a matter of time until the next scary thing comes along that forces lockdowns. It could be years or a decade, but the global government now has a protocol in place to deal with these matters that are not friendly to physical businesses.

I still tend to treat the Disney story as more Theme Park and resort-centric, although this is changing. I own this stock as part of my beta-orientated portfolio strategy that self-indexes the price weighted DJIA index, but I have not placed any focused/outsized bets. I would put my hat in the ring under $90 with a price range of $70 on the low end and $89 on the high end. This is using a modified PEG ratio implementing EBITDA and a modified Graham Number doing the same. This is a hold, but getting close.

Be the first to comment