FrozenShutter

Last month, I argued that Disney (NYSE:DIS) was breaking out of its downtrend. Since then, the company reported earnings that were well received, and shares popped into the $120s. This range was presumed to be an area of strong resistance and/or support. It is now becoming increasingly possible for Disney to again return to the $140s or higher within 2022.

This seems most likely to occur if Disney can report similarly strong earnings for its next fiscal quarter. Disney’s results for the prior quarter were largely ahead of expectations, with great strength shown by Parks & Experiences. Net adds for Disney+ also continued to impress. Disney’s advertising business also contributed nicely, and is likely to continue to do well this year, as political spending contributes to it. Continued strength from Parks & Experiences is also expected.

Disney also recently announced new pricing and an ad-supported version of Disney+ that will take effect on December 8, 2022. Disney now expects 2022 to be the peak loss year for Disney+ and anticipates the service being profitable by 2024.

I believe Disney’s valuation has reflected management’s decision to earn less than their content is worth in order to grow subscribers. A key to its future will be whether Disney can effectively increase costs and maintain those subs, as well as grow them over time.

Disney ended the prior quarter with a total direct to consumer and subscription revenue rate that would annualize to about $20 billion in sales. This is actually under-earning for the content, which could potentially bring as much as $25 billion. Price increases should help close the gap a bit.

At the same time, Disney is running multiple varied and occasionally overlapping services, with questions about where sports fits. Activist Dan Loeb argues for the spinning off of ESPN, among other possible changes. Disney also lacks total ownership of Hulu, and this structure appears likely to add costs, while splitting potential earnings.

There is no good reason for Comcast (CMCSA) to sell its stake in Hulu on the cheap. Also, Disney may find it has some regulatory burden to prove it can wholly own Hulu. Such concern is likely to be substantially lower if Disney were to spin off ESPN first, but there exists the possibility of further necessary concessions above and beyond Comcast’s asking price.

I expect this current quarter to provide continued strength from Parks & Experiences. Open parks continue to benefit from abnormal demand characteristics following the pandemic, and this could end up being a peak performance season, including considering the capacity to pull off price increases. The lessening of Chinese lockdowns also benefits global parks, and especially the local Shanghai and Hong Kong locations that were closed down and subsequently restricted. Disney also does a brisk cruise ship business that could perform better than expected.

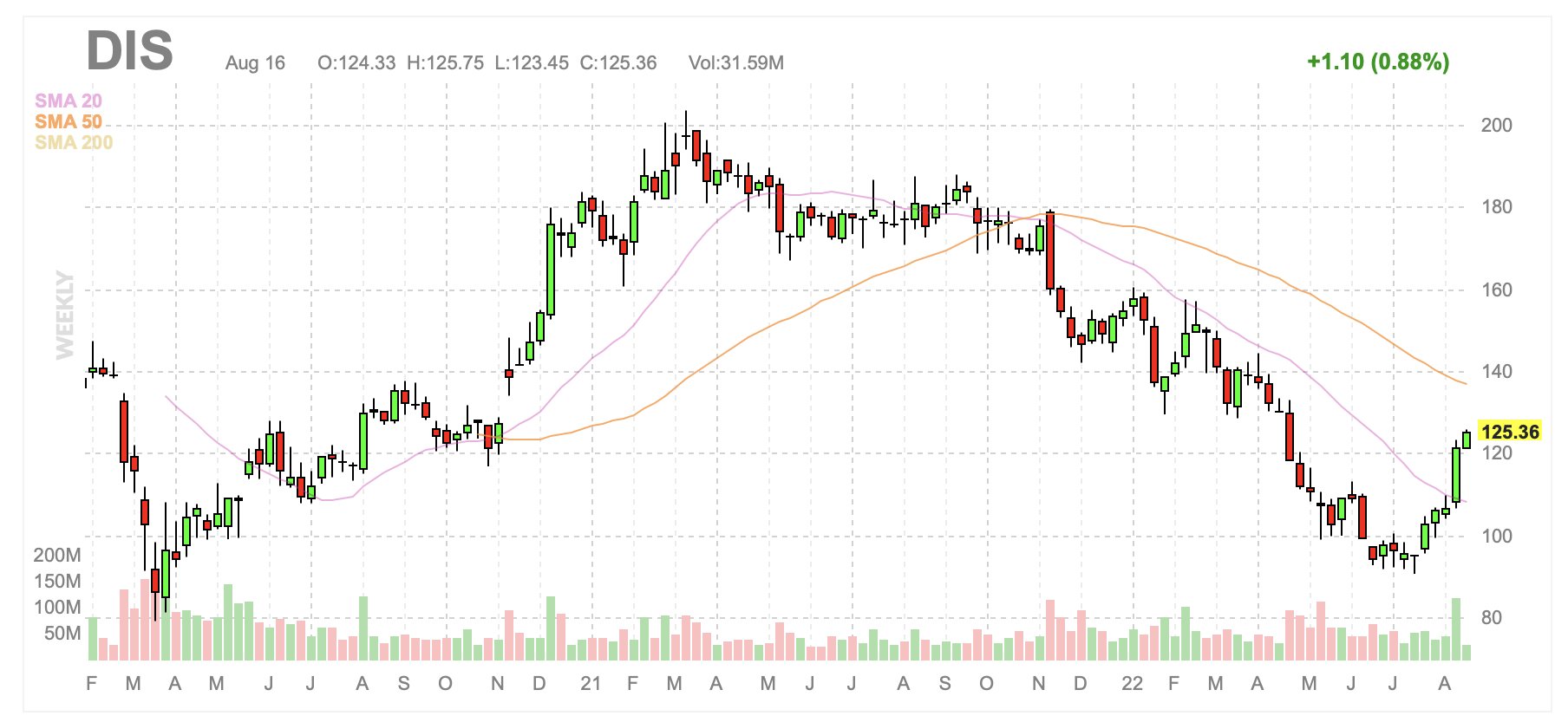

My theory from last month was based on the premise that Disney shares were breaking out of a declining wedge that they were stuck within since the start of 2022. That wedge ended with a capitulatory bottom, and now there has also been a post-earnings gap up in price through apparent resistance around $120. This now makes $120 probable support.

DIS weekly candlestick chart (Finviz.com)

Even more probable is that around $140 appears to be significant current resistance. The company spent time around $140 in late 2020, and again in late 2021. Also, DIS traded around $140 for a substantial part of the first few months of 2022, before finally making that capitulatory drop from which we now return.

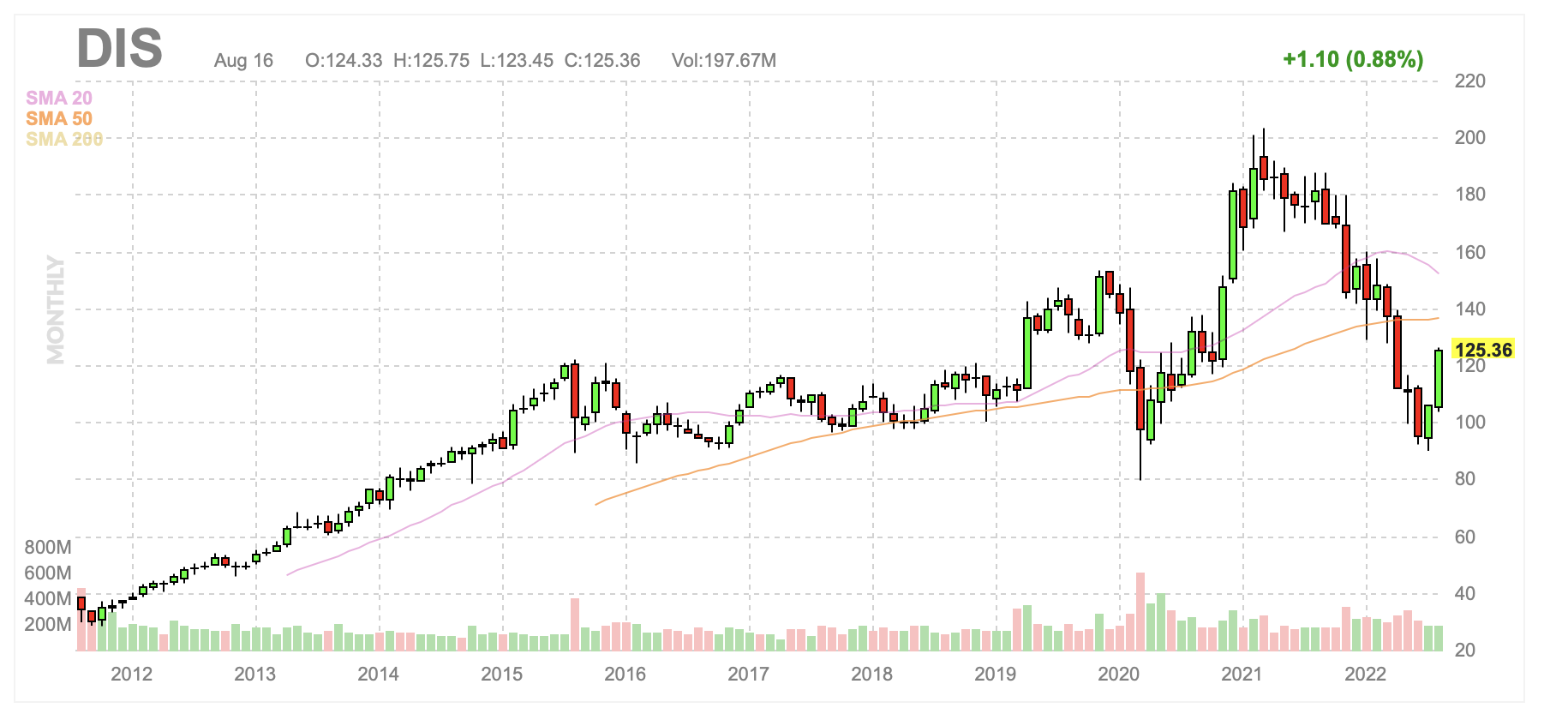

DIS monthly candlestick chart (Finviz.com)

Disney likely has an above-average ability to raise pricing on its products, whether goods or services, due to their strong brands. Disney is already increasing streaming prices this year, and is likely to push further increases in 2023 and/or 2024. Parks appear likely to see increases on tickets, souvenirs, and related goods and services too. The potential for such future increases is probably contributing to the strong performance this year.

A problem for Disney appears to be the proper treatment of ESPN. Much of the sports business has embraced sports betting, and it is apparent that ESPN could substantially benefit from new and highly profitable business lines. Disney may now be acting in a manner that is different than other possible owners of ESPN would likely chose by not fully embracing sports betting. As a result, ESPN could be a valuable asset that may find many interested. Even if Disney does not sell ESPN, or do other things proposed by Third Point, this attention has been a positive for its valuation.

Conclusion

Disney shares sustained a capitulatory drop in the first half of 2022, but long-term support that was set during the pandemic held. Shares broke out of their multi-month descending wedge, and are now back above $120, where they appear likely to stay for the near term.

Disney’s capacity to institute price increases on branded goods, content, and its parks is a tremendous benefit that remains under-appreciated. Disney’s decision to under-earn from its content library in order to gain streaming subscribers continues to be a major cost to earnings. Forthcoming price increases should lessen this burden.

Now, Disney looks likely to remain between $120 and $140 for the remainder 2022, with a reasonable chance of testing upside resistance on a strong market rally.

Be the first to comment