mesh cube

Digital Realty (NYSE:DLR) is a good income play in the data center industry, as the company has strong fundamentals and a highly recurring revenue profile, enabling it to distribute sustainably the vast majority of its profits to unit holders.

Company Overview

Digital Realty is a real estate investment trust (REIT) for federal income tax purposes, being one of the ten largest listed REITs in the U.S., measured by its market value of about $33 billion. The company was founded in 2004 and it’s focused on providing data centers, collocation, and interconnection solutions to its customers across the globe.

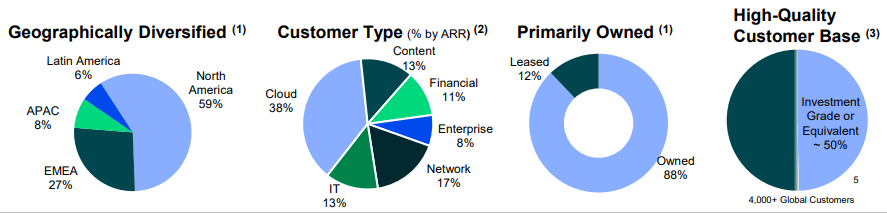

Digital Realty owns, acquires, and manages technology-related real estate, which is primarily owned by the company. At the end of last September, the company owned more than 300 data centers and had more than 4,000 customers, of which the largest segment is related to Cloud. While the company is still heavily exposed to North America, which accounts for some 59% of its revenue, it has a good geographical diversification, with the rest of revenue coming from Europe, Middle East and Africa, Asia-Pacific, and Latin America.

Business profile (Digital Realty)

Regarding its customer base, it is well diversified across industries and total number of customers, with its largest customer accounting for some 10% of its revenue. Its largest twenty customers account for about half of its total annualized rent, which means that Digital Realty is not too much dependent on a small number of customers, which is positive for the stability of its revenue and earnings profile over the long term.

Business Model & Growth

Digital Realty’s core business is data centers, which are facilities designed to accommodate servers and network equipment. Data centers have several pieces of hardware, of which the most important ones are computer servers, which process and store data, being supplied and owned by Digital Realty’s customers.

This means that Digital Realty business is the property and not the technological equipment, even though its business is obviously related to capex spending from technological companies. The company generates income mostly from providing space for its customers to place their computer servers in exchange for a fee, allowing them to have a less capital intensive business than compared if they had to own the property.

Therefore, Digital Realty provides an outsourcing solution to its customers, which usually have offices in cities that are more expensive than Digital Realty’s locations, making the economics of its data centers more attractive than its customers owning it.

The data center industry is quite concentrated and has some barriers to entry due to the significant investments required to build a data center, which means the industry landscape is not expected to change much in the near future. Digital Realty and Equinix (EQIX) are the two leading companies in this industry, while other players have much smaller sizes.

Therefore, competition in this industry is somewhat low, which is positive for established players as they enjoy good pricing power. Additionally, the costs of building a new data center are considerable, plus moving servers to a new place are also considerable, which means that customers usually don’t change frequently from data center providers, leading to very strong customer retention rates over the long term.

Regarding its growth strategy, Digital Realty has grown mainly through acquisitions, both in the U.S. and abroad. Its two largest acquisitions were DuPont Fabros in 2017 ($7.6 billion acquisition) and Interxion in 2019 ($8.4 billion). These acquisitions led to a higher concentration in the industry and increased Digital Realty’s size, while its most recent acquisition was Teraco in 2022, valued at $1.7 billion, which included seven assets in Africa.

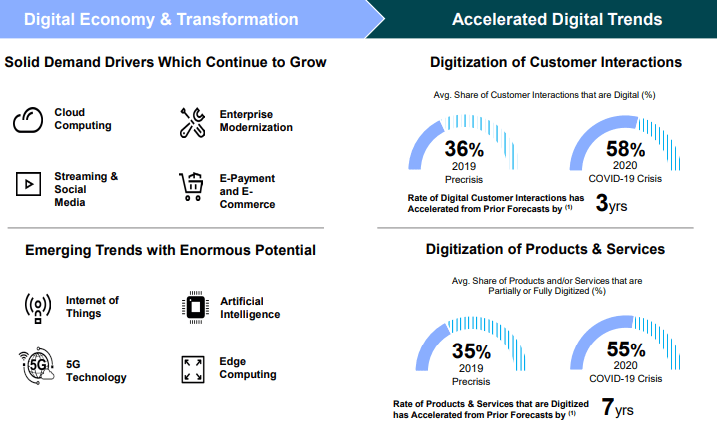

Beyond growing from acquisitions, Digital Realty’s growth prospects are also supported by industry tailwinds, as the demand for data centers is expected to increase strongly in the coming years. Indeed, according to Also, the data center industry was valued at $48.9 billion in 2020, and is expected to reach about $105 billion by 2025, showing that this industry has very good growth prospects ahead.

This growth is supported by several secular growth trends, such as digitalization, rapid growth of data, cloud adoption, and demand for IT outsourcing. These trends were only reinforced by the pandemic, which led to an increase acceptance of digital services and a structural change in labor organization (hybrid and remote workplaces), which are strong factors supporting demand for data centers over the coming years.

Secular trends (Digital Realty)

Beyond current technologies that continue supporting growing demand for data infrastructure, emerging trends that can also have a great impact, such as artificial intelligence or edge computing, which means that rising demand for data centers is not likely to slow down in the foreseeable future, boding well for Digital Realty’s long-term growth prospects.

Financial Overview & Dividends

Regarding its financial performance, Digital Realty has a strong track record given that its growth strategy has led to strong revenue and earnings growth over the past few years. Moreover, an interesting feature of its business model is highly recurring revenue profile due to the long-term nature of its contracts.

Digital Realty establishes lease terms with maturity of several years, which provides it with a recurring revenue stream, which is not much exposed to economic cycles, providing good visibility to its top-line over the medium term. Indeed, its average remaining lease term at the end of last September was about 4.7 years, which means most of its contracts have a long duration.

In 2021, Digital Realty reported a positive operating momentum, exceeding its own guidance provided at the beginning of the year. Its revenues amounted to $4.4 billion, an increase of 13.4% YoY, while its operating expenses rose to more than $3.7 billion (+11.5% YoY), leading to an operating income of $694 million.

This was an increase of 24.5% YoY, as the company’s operating leverage is quite good and a small gain in its operating margin led to strong earnings growth. This happens because the company’s cost structure is to a great extent based on relatively fixed costs, which means that when revenue increases, the company is able to increase earnings at a higher rate.

Due to gains on disposals, Digital Realty’s net income increased to nearly $1.7 billion in the year, compared to just $236 million in 2020. Its free funds from operations (FFO) were above $1.8 billion, up by 33% YoY.

During the first nine months of 2022, its operating performance remained resilient, despite the challenging economic background with interest rates going up and the US dollar strengthening considerably. Its revenues amounted to nearly $3.5 billion (+4.3% YoY), while its operating income was €527 million. In Q3 2022, the company’s bookings reached a new record ($176 million), making it the third quarter over the last four with bookings above $150 million. Nevertheless, due to strong forex headwinds, its AFFO per share of $1.67 was only up 1% YoY, and the company reduced its guidance for FFO for the full year due to higher interest rates and forex pressure.

Regarding leasing renewals, the company has been able to increase rents and also a good part of new contracts have CPI-based escalators, enabling Digital Realty to pass inflation to customers. Its backlog was $466 million at the end of Q3, of which some 25% was set to start during Q4, and some 45% was expected to start during 2023, providing good visibility regarding rental income growth over the coming quarters.

Regarding its capital structure, due to the long-term nature of its assets, Digital Realty finances its property portfolio with relatively high debt levels. This justifies its high net debt-to-EBITDA ratio of 6.4x at the end of Q3, which is higher than compared to its closest peer Equinix, but it is still at an acceptable level.

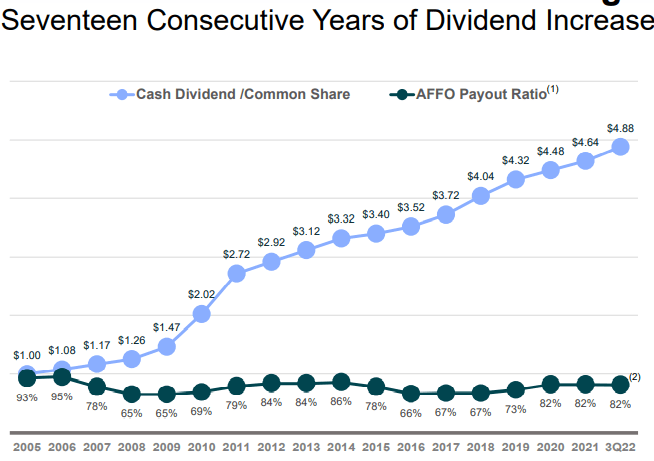

Regarding dividends, Digital Realty has to distribute annually 90% of its net taxable income to shareholders in order to maintain its qualification as a REIT. Not surprisingly, it has a very good dividend history since its inception, delivering several years of a growing dividend. Its payout ratio based on cash flow has been about 80% over the past few years, which seems to be sustainable.

Dividends (Digital Realty)

Its current quarterly dividend is $1.22 per share, or $4.88 annualized, which at its current share price leads to a dividend yield of about 4.4%. This is quite attractive considering the company’s business profile, and also higher than compared to Equinix, making it a good income play within the data center industry.

Risks

Regarding major risks for Digital Realty’s investment case, I see rising interest rates, forex volatility, and higher energy costs as major headwinds in the short term.

The Federal Reserve has been raising interest rates and its hiking pace is set to continue for some more time as the central bank keeps fighting inflation, pressuring financing costs. This is negative for the whole REIT sector, and Digital Realty is not immune to rising funding costs, even though its debt maturities in the short term are relatively low.

This rising interest rate environment has also led to a stronger U.S. dollar, which affects negatively its revenue generated internationally, as the company reports its financial figures in USD. As the company generates some 40% of its revenue abroad, this is an issue that should continue to affect its top-line growth over the coming quarters.

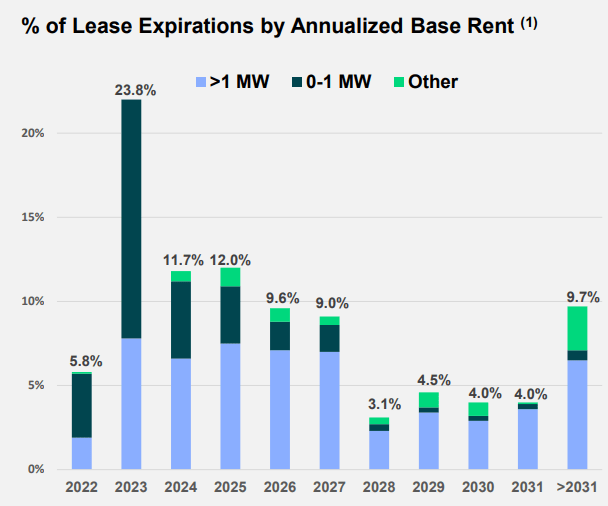

Another headwind is rising energy costs that may lead to higher customer churn, as the company may not be able to pass higher costs to its customers in upcoming rent renewals. While historically its rent retention rate is quite good at close to 80%, in the current inflationary environment the company may not be able to pass rising costs to customers like it has done in the past, putting pressure on rental income and earnings growth. As shown in the next graph, some 23.8% of leases expire in 2023, thus this is a risk that investors should not overlook as it could have a significant impact on Digital Realty’s growth in 2023.

Renewals (Digital Realty)

Conclusion

Digital Realty has strong fundamentals and a highly recurring revenue profile, which bodes quite well for sustainable dividend distributions over the long term. Moreover, it operates in an industry with strong secular growth prospects, providing it with an interesting income and growth profile over the next few years. Regarding its valuation, its currently trading at 16x P/FFO, at a discount to its historical average over the past five years, making it a good income play right now.

Be the first to comment