Sittipol Sukuna/iStock via Getty Images

Article Purpose

On December 16, 2022, the Index tracking the iShares Core Dividend Growth ETF (NYSEARCA:DGRO) reconstituted, resulting in the addition of high-growth stocks like Exxon Mobil (XOM) and Chevron (CVX) and the deletion of potential yield traps like 3M (MMM) and Intel (INTC). After assessing the ETF pre- and post-reconstitution, I’m pleased with the changes and see it better tracking the market next year while offering an estimated 2.43% dividend yield. Most importantly, DGRO should keep up its double-digit dividend growth rate, and I continue to view it as a solid dividend ETF going forward.

ETF Overview

Strategy and Reconstitution Summary

DGRO tracks the Morningstar US Dividend Growth Index, reconstituting annually, effective the third Friday of each December. The basic requirements are for companies to have five years of consecutive dividend growth, payout ratios less than 75%, and a positive consensus earnings forecast. Notably, the Index avoids potential yield traps by excluding the top 10% of companies by dividend yield.

The following summarizes the Index’s top 15 additions and previously failed screens. 80% were due to the “extreme dividend yield” screen, with Exxon Mobil, Chevron, and AbbVie (ABBV) being the most significant. The Index added 52 companies, but the 37 not shown have insignificant weights.

Morningstar

The Index removed 19 holdings primarily because of the extreme dividend yield screen. Intel and 3M currently have forward dividend yields of 5.62% and 4.90% and poor Seeking Alpha EPS Revision Grades. Therefore, these changes look beneficial from a momentum perspective.

Morningstar

Sector Exposures and Top Ten Holdings

DGRO’s sector exposures are shown below, with no sector dominating more than 20% of the portfolio. Health Care (19.00%) and Technology (17.45%) are prominent. Financials declined by 3.55% from 20.92% to 17.37%, while Energy increased by 5.96%. Investors treating DGRO as a core holding will appreciate this improved diversification.

iShares

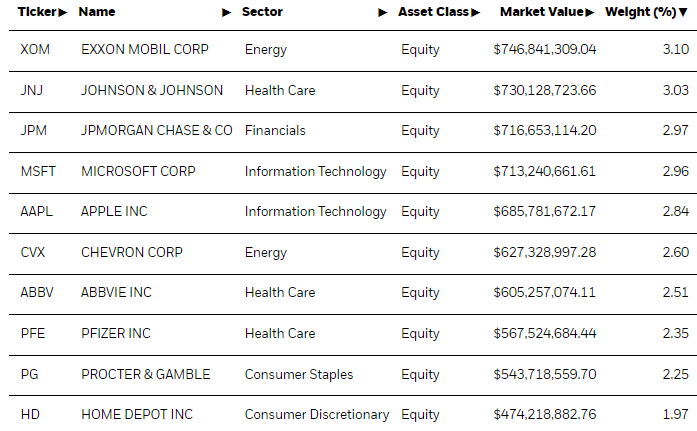

Exxon Mobil now leads the fund with a 3.10% weighting, followed by Johnson & Johnson (JNJ) and JPMorgan Chase (JPM). These holdings total 26.58% compared to 24.40% for the SPDR S&P 500 Trust ETF (SPY), indicating a bit less diversification than the straightforward market approach.

iShares

Performance and Dividends

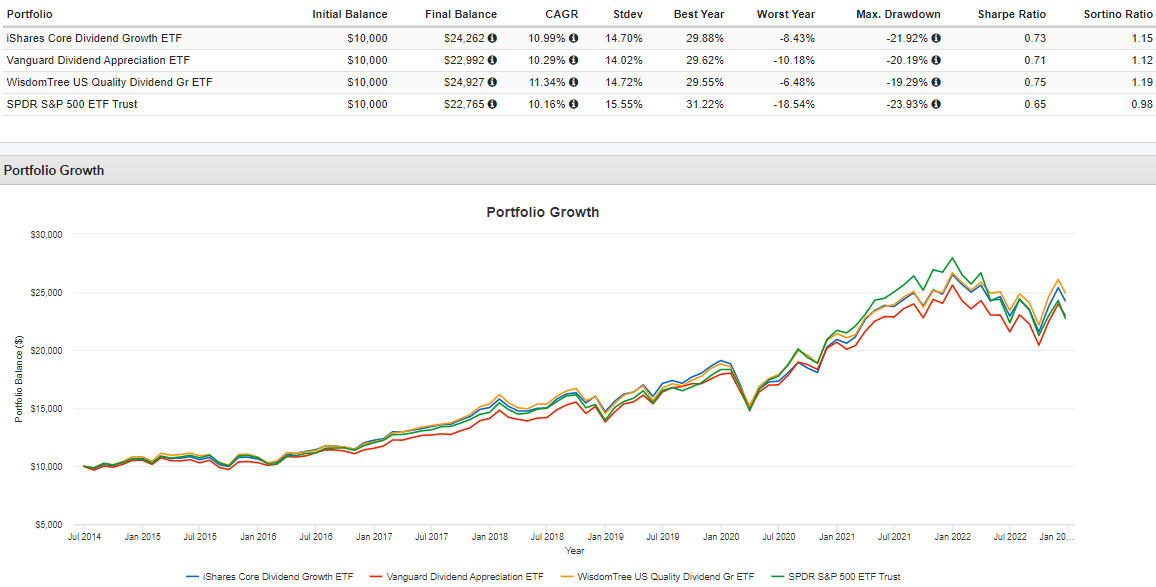

DGRO has gained an annualized 10.99% since its June 2014 inception date, besting the Vanguard Dividend Appreciation ETF (VIG) and SPY by 0.70% and 0.83% per year with comparable volatility. The WisdomTree U.S. Dividend Growth ETF (DGRW) outperformed DGRO by 0.35% per year and is beating by about 2% YTD. In a previous article, I noted DGRW’s superior profitability and lower volatility as the likely source.

Portfolio Visualizer

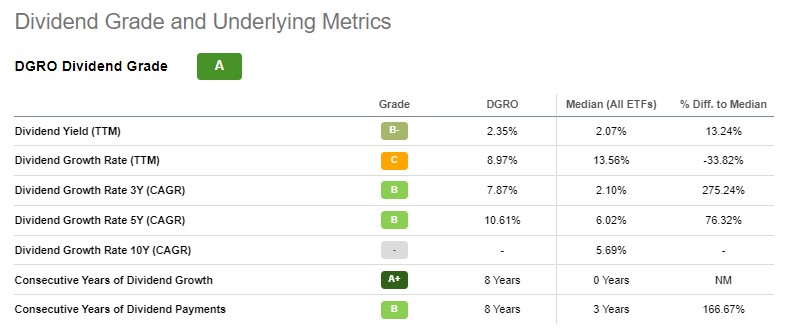

DGRO earns an impressive “A” Dividend Grade based on Seeking Alpha Factor Grades. As expected in September, DGRO’s dividend growth resumed with the last two quarterly payments, and dividends have grown at an annualized 10.61% rate over the previous five years. The downside is a relatively low starting yield of 2.35%. However, if you have a somewhat long time horizon of 7-10 years, your yield on cost will likely exceed what high-dividend ETFs currently offer. My preference is dividend growth over dividend yield.

Seeking Alpha

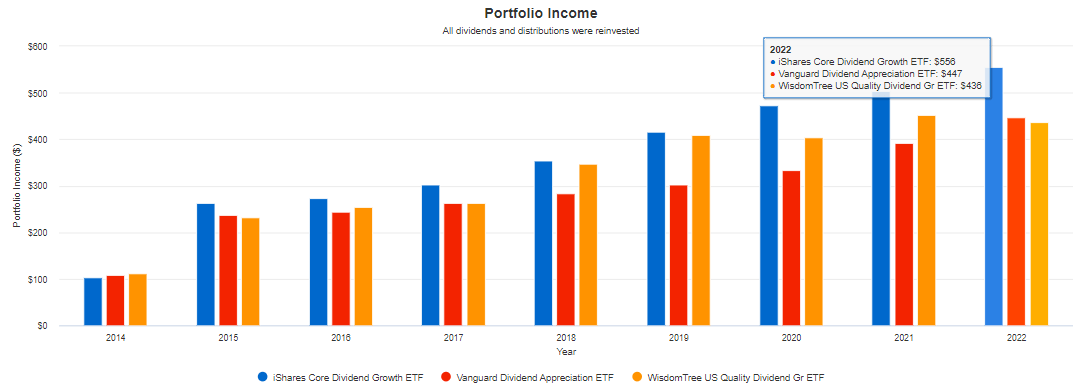

To illustrate, DGRO’s portfolio income on an initial $10,000 investment in July 2014 (with reinvested dividends) is now $556, or a $ 5.56% yield on cost. VIG’s and DGRW’s yield on cost is about 1% less, even after accounting for the one remaining monthly distribution for DGRW.

Portfolio Visualizer

ETF Analysis

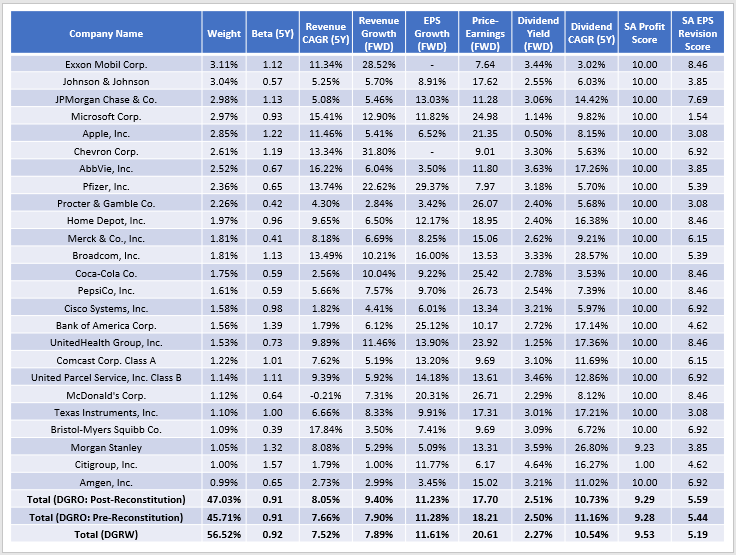

One of the reasons why DGRO is solid is that despite the sometimes-eventful reconstitutions, the portfolio’s features are consistent year-to-year. For example, investors won’t wake up one December morning to find DGRO’s estimated dividend yield or growth has plummeted. The following table demonstrates that consistency by comparing DGRO’s fundamentals pre- and post-reconstitution. I’ve also included DGRW’s fundamentals in the final row.

The Sunday Investor

DGRO’s five-year beta remains at 0.91, about average for large-cap dividend ETFs, indicating that it can provide some downside protection in a market downturn. That, along with its relatively low 17.70x forward earnings valuation, is why DGRO and its peers outperformed in 2022. DGRO’s top holdings include several that share these two features, including AbbVie, up 25% YTD. DGRO’s top five additions previously failed the extreme dividend yield screen, and they’re all performing well this year, thereby reducing their yields. This way, DGRO becomes better from a momentum perspective at each reconstitution, though it’s essential to look for signs of style drift throughout the year.

Seeking Alpha

In a prior review, I noted how DGRO’s sales and earnings growth rates were stronger than high-dividend peers like SCHD and CDC. These features meant DGRO was better able to support future dividend growth, too, and I’m pleased to see these metrics improve even more: 9.40% vs. 7.90% pre-reconstitution. Importantly, this improvement did not sacrifice profitability by adding more small- and mid-cap stocks. DGRO’s weighted-average market capitalization increased from $252 billion to $281 billion, and its top 25 holdings list is full of companies with “A+” Seeking Alpha Profitability Grades.

Compared to DGRW, DGRO now looks superior. Along with better growth and valuation metrics, DGRO’s EPS Revision Score of 5.59/10 suggests stronger sentiment on Wall Street. The only area where DGRW looks more attractive is its profitability score (9.53/10 vs. 9.29/10). However, both scores are strong, and it’s unnecessary to be too strict with this criterion.

The portfolio’s gross dividend yield on dividends is 2.51% or 2.43% after fees. In other words, the trailing 2.35% dividend yield is accurate, as is the 10.73% historical dividend growth rate listed in the earlier table. Again, I appreciate consistency, even if the reconstitution resulted in some notable changes.

Investment Recommendation

The key takeaway from this year’s reconstitution was the addition of Exxon Mobil and Chevron, two relatively-low risk Energy companies that pay solid dividends, have good estimated growth, and provide a necessary inflation hedge should that continue to be problematic in 2023. My target for the sector is 10%, and DGRO’s 7.28% is now in the acceptable range and above what S&P 500 Index ETFs offer. AbbVie is another excellent addition, and like most companies, the Index added it because of recent price appreciation. In contrast, the Index removed struggling companies like Intel and 3M. These are two examples of companies with negative earnings momentum, indicated by “D” and “C-“ EPS Revisions Grades. To buy them now is a contrarian play, and not only is that too speculative, but it also goes against DGRO’s dividend growth objectives. If it’s dividend consistency rather than dividend growth you’re seeking, I recommend readers check out NOBL instead.

While reconstitutions sometimes change the underlying fundamentals of an ETF, DGRO’s was consistent, and that’s something shareholders should welcome. The ETF trades at an attractive 17.70x forward earnings, has double-digit earnings and dividend growth, and an estimated 2.43% dividend yield that will eventually catch up to most higher-yielding peers. Mission accomplished, as far as I’m concerned, and I think 2023 will be another solid year for this popular dividend growth ETF. Thank you for reading, and I hope you all have a Happy Holidays and take a well-deserved break!

Be the first to comment