Khosrork

It is not exactly a surprise that the high rate of inflation in the United States has been causing havoc in the budgets of many American households. As this inflation has been concentrated in the necessary areas of food and energy, it has had a devastating effect on those of limited means and has thus forced many people to take on second jobs or perform other odd jobs in order to obtain the money that they need to feed their families and heat their homes.

Fortunately, as investors, we have better methods that we can use to obtain the money that we need to support ourselves in today’s environment. One of the best of these methods is to purchase shares of a closed-end fund that specializes in the generation of income. These funds are a good way to get income because they provide easy access to a diversified, professionally-managed portfolio of assets that is specifically designed for that task. In addition, these funds can usually deliver a higher yield than pretty much anything else in the market, including the assets in which the fund is invested.

In this article, we will discuss the Flaherty & Crumrine Dynamic Preferred and Income Fund, Inc. (NYSE:DFP), which is one closed-end fund that investors can purchase to earn an income. I have discussed this fund before, but more than a year has passed since that time, so obviously, a great many things have changed. This article will, therefore, specifically focus on these changes as well as provide an updated analysis of the fund’s financial performance. Thus, let us investigate and see if this 7.58%-yielding fund could be a good addition to your portfolio today.

About The Fund

According to the fund’s webpage, the Flaherty & Crumrine Dynamic Preferred & Income Fund has the stated objective of providing its investors with a high level of total return. This is an unusual objective for a fixed-income fund, although this one does specifically state that it emphasizes total return as the largest component of total return. The reason why this is somewhat unusual is that fixed-income securities are not generally good securities to purchase for capital gains because they do not have any inherent link to the growth and prosperity of the issuing company. After all, a company will not increase the interest rate that it pays on its loans just because its profits go up. With that said, fixed-income securities have been in a bull market for most of the past forty years but that is due to interest rates. These securities are priced based on interest rates. Basically, when interest rates decline then fixed-income securities rise in price and vice versa. This is because newly issued fixed-income securities will have a yield that corresponds to the current market interest rate so the price of already-existing securities will adjust so that they deliver a similar yield as newly-issued securities. This has to be the case because otherwise, nobody will buy a new security in falling rate environments or an existing security in rising rate environments. The reason for the forty-year bull market in bonds was thus simply that the Federal Reserve has been cutting rates since the early 1980s.

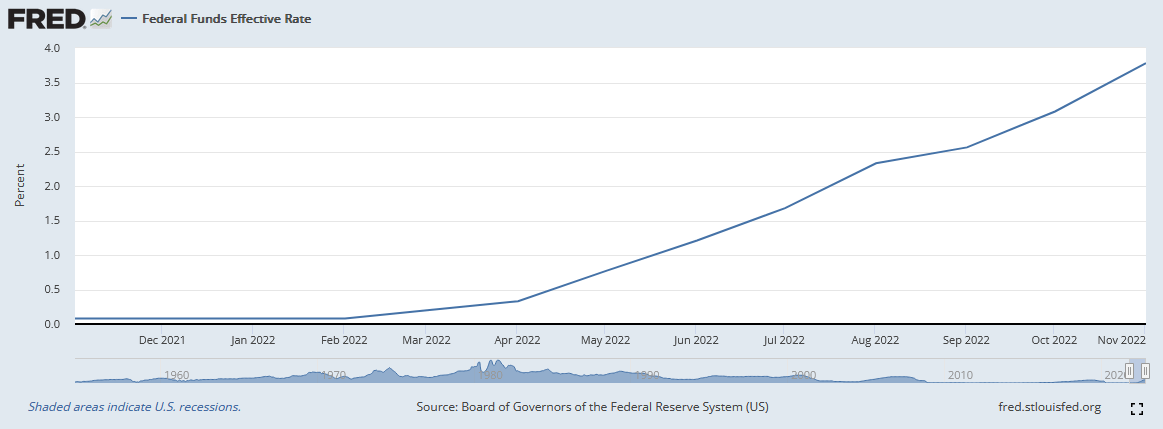

As everyone reading this is no doubt aware, the Federal Reserve switched its policy last year in response to the inflation in the economy. In order to combat it, the central bank began hiking the federal funds rate aggressively. Back in February 2022, the federal funds rate was at 0.08% but it had risen to 3.78% by November:

Federal Reserve Bank of St. Louis

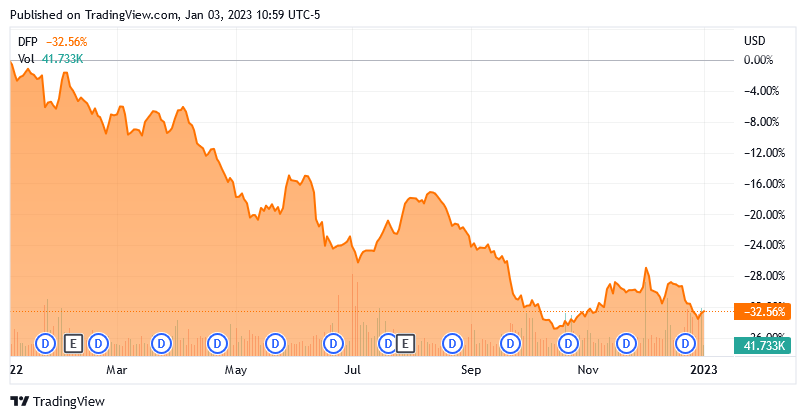

The central bank increased rates again by 50 basis points in December and is generally expected to increase the rate further in 2023. Thus, we can expect to see this number increase over the next few months. The Federal Reserve is generally projected to let rates settle in around 5% but that is by no means certain. This has had a devastating effect on the Flaherty & Crumrine Dynamic Preferred and Income Fund. Over the past twelve months, the fund has fallen 32.56%, which is one of the worst performances of any fixed-income closed-end fund:

Seeking Alpha

This performance is undoubtedly disappointing for shareholders, especially since the ICE Exchange-Listed Preferred & Hybrid Securities Index is only down 21.61% over the same period. The fact that the Flaherty & Crumrine fund has a higher yield does nothing to change this underperformance, especially since the index currently has a 6.01% yield, which is not that far below the 7.58% yield of the closed-end fund. The biggest reason for this is leverage, as we will discuss later.

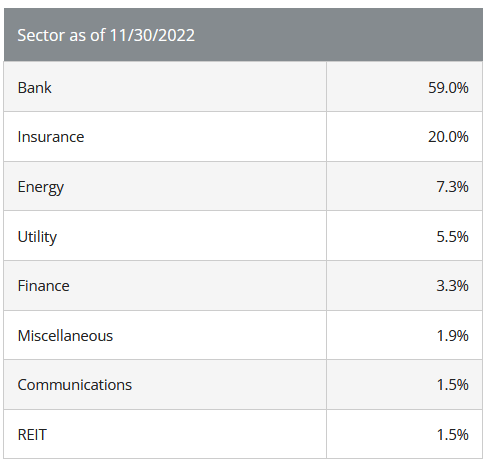

As we discussed the last time that we looked at the fund, the Flaherty & Crumrine Dynamic Preferred and Income Fund is heavily invested in banks. This remains the case today, which we can see simply by looking at the largest positions in the fund. Here they are:

Flaherty & Crumrine

This is not unusual for a preferred stock fund. After all, banks are the largest issuers of preferred stock in the market. This is due to international banking regulations that require a bank to keep a certain proportion of its assets in the form of Tier one capital. Tier one capital is that proportion of a bank’s assets that is not simultaneously a liability owed to someone else, such as a depositor. There are two ways for a bank to increase its Tier one capital when regulations require such. These two ways are to issue common stock or to issue preferred stock. A bank will, however, typically issue preferred stock in such a situation because management will not want to dilute the common stockholders. Preferred stock is usually more expensive than debt because it typically has a much higher yield. As such, it is more expensive to issue than bonds so companies in other industries will usually opt to issue bonds as opposed to preferred stock when capital is needed. Thus, by default, banks end up being among the few companies that issue preferred stock due to these regulations. A preferred stock fund will, therefore, almost always contain primarily bank stocks.

The Flaherty & Crumrine Dynamic Preferred and Income Fund, Inc. is not quite as concentrated in banks as the preferred stock index, however. The fund only has 59.0% of the portfolio invested in banks:

Flaherty & Crumrine

This compares to 66.84% of the preferred stock index that is invested in such companies. However, it is important to note that the preferred stock index simply states that it is 66.84% invested in “financial institutions.” It does not specify exactly whether these are banks or some other form of a financial institution, such as an insurance company. If we assume that the index’s category includes banks, insurance companies, and specialty finance companies then the Flaherty & Crumrine Dynamic Preferred and Income Fund is substantially more exposed to these companies than the index. However, insurance companies are very different animals from banks. In particular, insurance companies are not generally hurt by rising interest rates in the way that banks can be. Although the insurance company will probably be heavily invested in bonds, it also has the flexibility to raise premiums to offset any losses on the bond portfolio. A bank cannot really do this so we need to bear this in mind when evaluating the overall risk of the fund’s portfolio.

One thing that we notice by looking at the list of the fund’s largest holdings above is that many of the companies are the same as they were a year ago. However, the fund has reduced its weight to many of the companies. In particular, its weighting to Citigroup (C) declined from 4.7% a year ago to 4.5% today. This could very easily be a case of one company’s stock outperforming another in the market, though, and the fund’s 12.00% annual turnover appears to support this idea. This is a fairly low turnover for any closed-end fund and indicates that the fund is not really changing its portfolio very much. This can be an advantage because it costs money to trade preferred stock and other assets. These expenses are billed to the shareholders and thus create a drag on the fund. After all, management will need to generate sufficient returns to cover these costs and still keep up with the index. There are very few funds that can accomplish this and as such actively-managed funds usually end up underperforming the index. As we have already seen, this is the case with this fund as it underperformed its benchmark fairly significantly over the past twelve months.

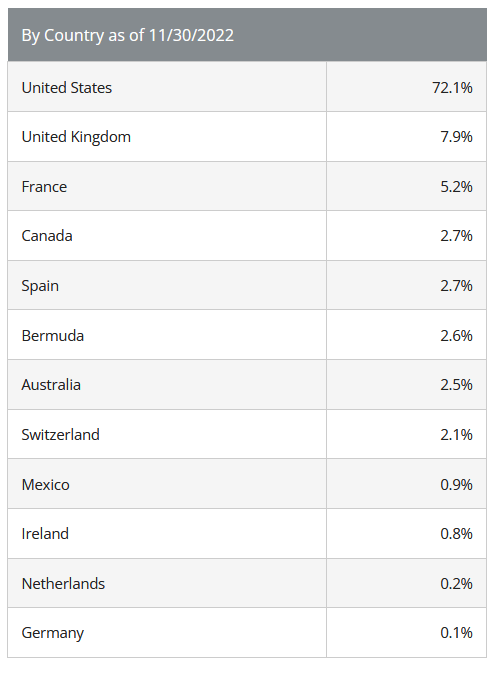

One big difference that the Flaherty & Crumrine Dynamic Preferred and Income Fund has over the index is that it is a global fund. In fact, only 72.1% of the fund’s holdings are issued by American companies:

Flaherty & Crumrine

This is something that could be a very important difference as many of these countries have their own central banks and interest rate policies. For example, the European Central Bank did not start raising rates in the Eurozone until well after the Federal Reserve had already embarked on its monetary tightening policy. That will have an impact on the performance of the securities issued by companies in these nations and thus could be one reason for the performance disparity that we see between this fund and the index.

However, it can be a good thing that this fund is investing in securities issued by non-American companies. The biggest benefit that we get from this is the protection that it provides against regime risk. Regime risk is the risk that a government or other authority takes some action that has an adverse impact on a company that is in our portfolios. An obvious example here would be a difference in interest rate policy given the impact that can have on fixed-income securities. The best way to protect ourselves against this risk is by ensuring that our assets are properly spread around multiple countries. This fund is clearly making a good effort at this, which we should appreciate.

Leverage

As stated in the introduction, closed-end funds are able to use certain techniques that allow them to produce a higher yield than the underlying assets. One of these tactics that is employed by the Flaherty & Crumrine Dynamic Preferred and Income Fund is the use of leverage. Basically, the fund is borrowing money and using those borrowed funds to purchase preferred stocks and other fixed-income assets. As long as the yield on the purchased assets is higher than the interest rate that the fund has to pay on the borrowed assets, the strategy works pretty well to boost the overall portfolio yield. The fund is capable of borrowing at institutional rates, which are much lower than retail rates, so this will usually be the case.

However, the use of leverage is a double-edged sword because debt boosts both gains and losses. This may be another reason why the fund has been significantly underperforming the index over the past twelve months. Therefore, we need to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I do not typically like to see a closed-end fund’s leverage above a third as a percentage of its assets for this reason. The Flaherty & Crumrine Dynamic Preferred and Income Fund is well above this one-third level, unfortunately. Its levered assets currently comprise 39.98% of the portfolio. Although fixed-income assets tend to be safer than common equities, this leverage still represents more risk than I would really like to see.

Distribution Analysis

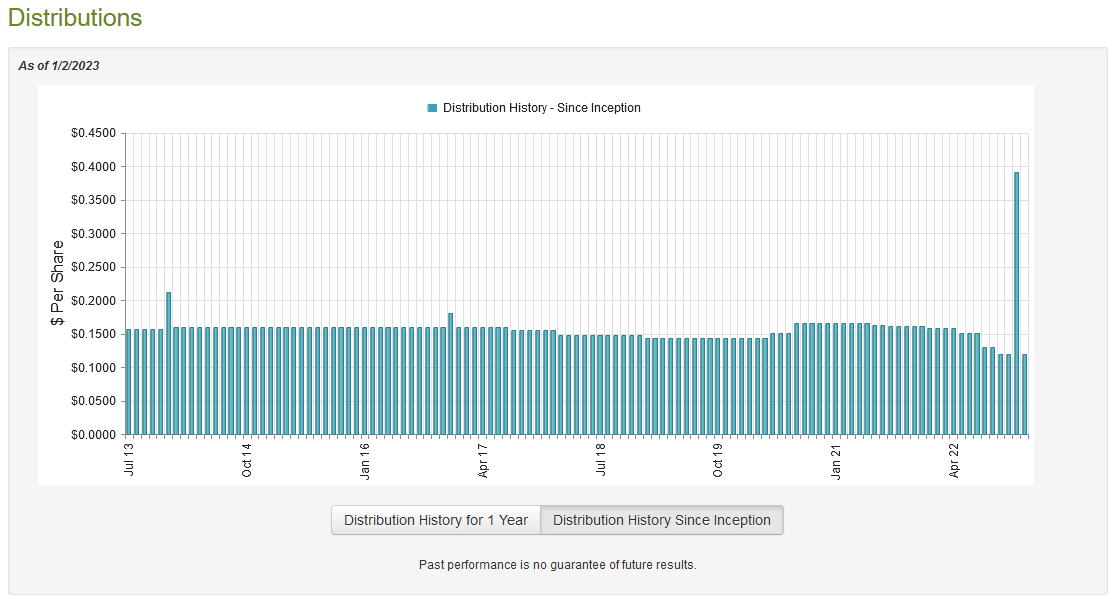

As mentioned earlier in this article, the Flaherty & Crumrine Dynamic Preferred and Income Fund has the stated objective of providing investors with a high level of total return but it aims to achieve this primarily through the generation of income. As such, we might expect that the fund will have a very high yield. This is indeed the case as the fund pays out a monthly distribution of $0.1190 per share ($1.428 per share annually), which gives it a 7.58% yield at the current price. Unfortunately, the fund has not been particularly consistent with its distribution over time and has cut it a few times since the start of 2021:

CEF Connect

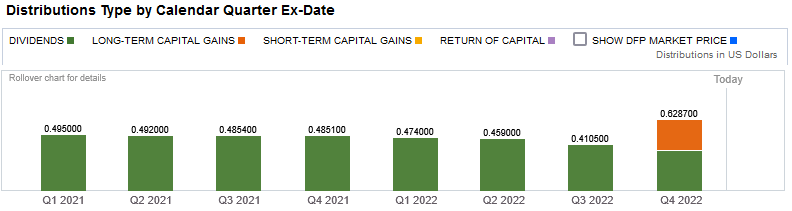

This is something that will certainly reduce the appeal of this fund in the eyes of many investors, particularly those that are looking for a safe and secure source of income with which to pay their bills. However, there may be some comfort in the fact that all of the fund’s distributions are classified as dividend income or capital gains. Unlike some of its peers, the fund has not been making return of capital distributions:

Fidelity Investments

The reason why this may be comforting is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. We seemingly do not have to worry about that here, but as I have pointed out before, it is possible for these distributions to be misclassified. As such, we will still want to investigate the fund’s finances in order to determine exactly how sustainable its distributions are likely to be.

Unfortunately, we do not have an especially recent document to consult for this purpose. The fund’s most recent financial report corresponds to the six-month period ending May 31, 2022. As such, it will not provide us with any insight into the fund’s performance over the past seven months, including the cause of the most recent distribution cut. However, it should provide us will some idea of how well the fund navigated the early stages of the Federal Reserve’s monetary tightening which began in March of 2022. During the six-month period, the Flaherty & Crumrine Dynamic Preferred and Income Fund received a total of $8,840,028 in dividends and $13,684,521 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund brought in a total of $22,575,249 during the period. The fund paid its expenses out of this amount, leaving it with $18,334,723 available for investors. This was, unfortunately, not enough to cover the $19,164,767 that the fund paid out in distributions, although it did get very close. We do still need to figure out where the fund got the remainder of the money needed, however.

One potential source for the remaining money is capital gains. Perhaps surprisingly considering the Federal Reserve’s actions during the period in question, the Flaherty & Crumrine Dynamic Preferred and Income Fund had some success at this. During the six-month period, the fund achieved net realized gains of $7,218,608 but this was offset by net unrealized losses of $84,809,410. Overall, the fund’s assets declined by $68,240,178 after accounting for all inflows and outflows. The fund did clearly have enough net investment income and realized capital gains to cover its distributions with some money left over, though, which is comforting. Overall, the Flaherty & Crumrine Dynamic Preferred and Income Fund, Inc. probably is paying out a reasonable amount and it does not appear to be overdistributing. This is nice to see.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Flaherty & Crumrine Dynamic Preferred and Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is, therefore, the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of December 30, 2022 (the most recent date for which data is currently available), the Flaherty & Crumrine Dynamic Preferred and Income Fund had a net asset value of $20.20 per share, but the shares only trade for $18.92 each. This gives the shares a 6.34% discount to net asset value at the current price. This is reasonably comparable to the 5.75% discount that the shares have averaged over the last month and represents a fairly attractive price at which to buy the shares. Overall, the price is very reasonable today.

Conclusion

In conclusion, the Flaherty & Crumrine Dynamic Preferred and Income Fund has delivered a very disappointing performance over the past year that is likely to turn many investors away. A closer look at it reveals that there is a decent amount to like in this preferred income fund. The biggest concern here is that Flaherty & Crumrine Dynamic Preferred and Income Fund, Inc.’s leverage appears fairly high, so there will likely be more losses if interest rates increase, as expected. However, most analysts believe that the worst is behind us and that any further rate increases will be muted. The fund appears to be paying out only money that it can afford through its distribution and the price is quite reasonable today. While it might make sense to hold off buying shares until interest rates have peaked, I also could not fault anyone that wants to slowly start buying Flaherty & Crumrine Dynamic Preferred and Income Fund, Inc. and reinvesting the distributions while waiting.

Be the first to comment