Boarding1Now/iStock Editorial via Getty Images

We believe that Delta Air Lines (NYSE:DAL) is an attractive investment opportunity and should be awarded a buy rating due to the following reasons:

- The current valuation of the company is favorable.

- High oil prices should gradually drop over the next year, which would likely result in Delta Air Lines recovering its profitability and cash flow to September 2019 levels.

- The high level of debt the company took on due to COVID-19 is rapidly being paid down, and most of the company’s interest rates are fixed.

Based on the above reasons and the valuation we have performed, prospective investors should take this opportunity to buy Delta Air Lines.

Introduction to Company, Backdrop

Delta Air Lines is major airliner in the U.S. and a legacy carrier. The airline industry took a significant hit in 2020 due to the outbreak of COVID-19, but the turnaround in the industry has been exceptional. Delta Air Lines recently reported its highest September quarterly revenue on 17% less capacity than September 2019.

At the time this was written, Delta Air Lines’ share price was $38, which is about 30% down from its pre-COVID range of $50-$60 per share. In 2021, the stock traded in the range of $40 to $50 per share after a great recovery from lows of +/- $20. Since then, the stock has struggled to shake off the effects of higher fuel prices resulting from the war in Ukraine, the lack of investment by oil producers into additional production capacity limiting supply, and OPEC limiting production decisions. Given the recovery of airline travel domestically and internationally, the question then is whether or not Delta Air Lines at its current price is a buy.

September 2022 Results

Delta Air Lines reported its highest quarterly airline revenue of $12.8 billion in September 2022, which was 3% above the third quarter of 2019 ($12.5 billion). This is despite the airliner operating at 17% less capacity. The company’s adjusted operating income came in at $1.5 billion, an 11.6% margin, compared to $2 billion, a 16.4% margin, in Q3 2019. The adjusted net income before tax in Q3 2022 was $1.276 million, vs. $1.968 billion in Q3 2019. That’s a $692 million difference. Earnings per share in Q3 2022 was $1.08 vs. $2.31in Q3 2019.

From the results outlined above, it is clear that while revenue has exceeded expectations, profits have not had the same positive recovery. Reviewing the financial statements of Delta Air Lines, it is clear that the poor profitability is driven by the following:

- Aircraft fuel and related taxes being $1 billion greater than Q3 2019 on 17% less capacity due to higher fuel prices.

- The above has been partially offset by greater revenue for the quarter – about $333 million from refinery.

- To a lesser extent, there’s the interest burden of $250 million per quarter, which is almost $200 million higher than Q3 2019.

Based on the above, the key question to answer in order to determine whether or not Delta Air Lines will reach its 2019 profitability is whether the high fuel costs will continue.

High Fuel Costs

Aircraft fuel and related taxes were $1 billion greater for Q4 than Q3 2019 on 17% less capacity, which is clearly creating a hole in operating profitability. Jet fuel is primarily derived from crude oil, and therefore be driven by the price of Brent crude and WTI crude. Since Russia invaded Ukraine, the price of oil has skyrocketed.

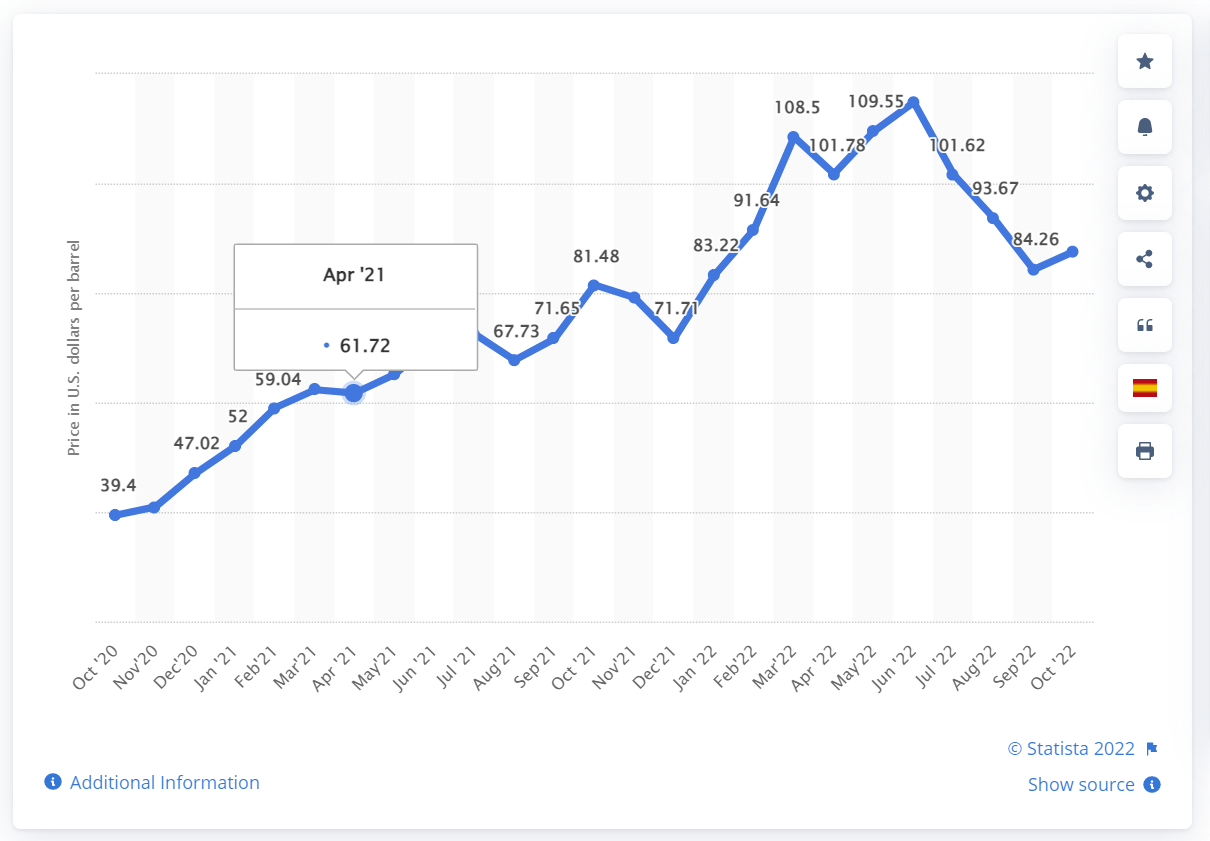

Brent monthly average crude oil price 2022 (Statista)

The price of Brent crude oil, the international benchmark, averaged $64 per barrel in 2019. The price of West Texas Intermediate crude oil, the U.S. benchmark, averaged $57 per barrel in 2019. Comparing this to Q3 2022, which had an average of $100 per barrel for Brent crude and $93 per barrel for WTI crude, shows why profitability has been affected so badly in the last quarter. Looking forward to the latest quarter that will be reported on shortly, prices have improved substantially. The average Brent crude price in Q4 2022 was $88.72 per barrel and the WTI average price was $82.79 per barrel. This is a +/- 12.5% improvement that will help profitability for Q4.

Management expects Q4 adjusted fuel price per gallon of between $3.35 and $3.55 compared to an adjusted fuel price of $3.53 per gallon in Q3. We believe that there might be a more favorable final result due to the continued decline in oil prices from Q4, as noted above.

We also take comfort from the fact that Delta Air Lines does understand this risk. In the 10-K the company identified the following key risks to its business related to fuel:

In our business and results of operations are dependent on the price of aircraft fuel. High fuel costs or cost increases, including in the cost of crude oil, could have a material adverse effect on our results of operations.

Our aircraft fuel purchase contracts alone do not provide material protection against price increases as these contracts typically establish the price based on industry standard market price indices.

The competitive nature of the airline industry may affect our ability to pass along rapidly increasing fuel costs to our customers. In addition, because passengers often purchase tickets well in advance of their travel, a significant rapid increase in fuel price may result in the fare charged not covering that increase. At times in the past, we often were not able to increase our fares to offset fully the effect of increases in fuel costs, and we may not be able to do so in the future.

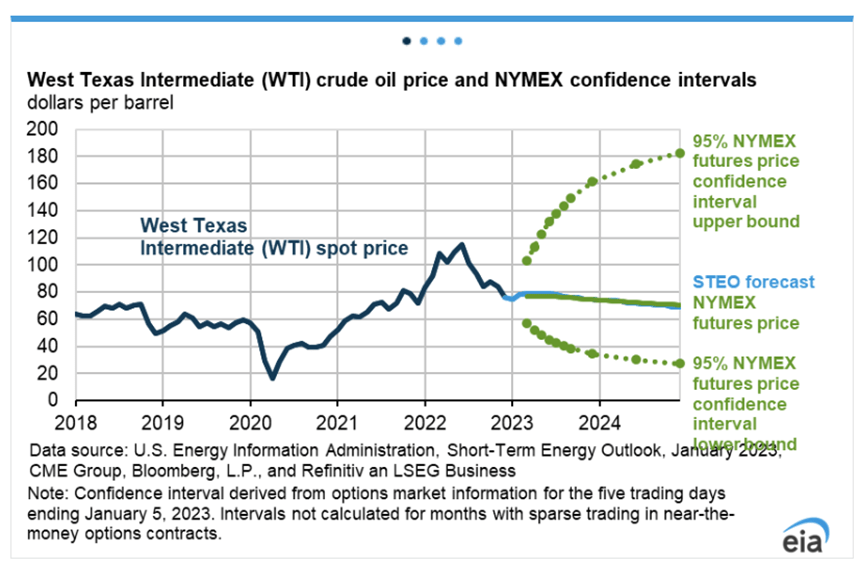

Looking at the forecasts for the price of oil in 2023, it would appear that things are starting to look better. The U.S. Energy Information Administration forecast the that Brent crude oil spot price will average $83 per barrel in 2023. This is a 10% favorable forecast revision from only a month ago.

WTI Oil Forecast 2023 (U.S. Energy Information Administration)

Goldman Sachs predicts that Brent crude oil will be $110 a barrel in the back end of 2023. The market consensus appears to show a slight but uncertain ease up in oil prices in 2023; however, a truly big change looks only likely in 2024. Delta Air Lines does not hedge its fuel prices significantly, so should the prices remain at current levels as predicted, profitability in 2023 will stay significantly lower than 2021 and 2019. We think the reality might be a bit different than these forecasts. In our view, any commodity that experiences an increase in price of this magnitude will eventually see a price slump, as elevated prices are usually not sustainable.

The narrative of oil prices is shifting, despite upward pressures from China’s moves to ease virus curbs. Oil prices have recently been falling as fears of supply disruption eased on news that the G7 were considering a high price cap on Russian oil. This is higher than what the market expected and reduces the risk of global supply disruptions. Additionally, a greater-than-expected build up in U.S. gasoline inventories and concerns about the global growth outlook, in addition to a soft physical market and falling liquidity, have added downward pressure on prices. It is clear that there has been a general decline in the expectations for oil prices. In our view, any commodity that experiences a large increase in prices will eventually see the price slump as elevated prices are usually not sustainable.

There is always the risk that this does not play out in a positive way, but we believe the current Delta Air Lines share price has factored in a more persistently high oil price. As such, the downside risk for the stock price remains low.

Valuation – Qualitative and Quantitative Factors

To value the company, we have used two valuation techniques:

- EV/EBITDA (FWD)

- Non-GAAP P/E

The EV/EBITDA (FWD) for Delta Air Lines is 8.10, the industry mean is 10.40, and Delta Air Lines’ five-year average is 9.35. If the company recovers to its historic average or moves in line with the industry average, we believe there is at least 15% share appreciation to be had at a moderate risk level.

Delta Air Lines’ current share price of $38 per share comes with a non-GAAP forward price/earnings ratio of 12.46x. The industry median is 16.66x and Delta Air Lines’ five-year average is 10.27x. The price/earnings multiple incorporates the interest expense from the large debt burden and hence why we believe it’s an important valuation metric, given the large amounts of debt taken on by Delta Air Lines. We believe that historic benchmarks should be adjusted for the change in the industry. Airlines in 2022 faced higher fuel costs, fewer business class flights, higher costs related to increased debt loads taken during COVID-19, and climate change pressures. The offsetting effects are the restructuring savings Delta Air Lines has enjoyed, due to the forced changes in the industry that make the company more lean and efficient.

To derive the value of the company, we have assumed that September 2022 Q3’s non-GAAP EPS of $1.51 per share will, at a minimum, continue for the next four quarters, giving us a 2023 EPS of +$6 per share. At an estimated price/earnings of 8, the share target will be $48 per share – a +25% share appreciation from the current price. We have assumed the historical price/earnings ratio of 10x will be adjusted down to 8x due to longer-than-expected elevated oil prices, as well as other structural changes in the airline industry.

Based on both valuation metrics above, one would expect that, as the industry continues to normalize, there is a minimum of 15%-25% share appreciation available in the next year. In the longer term, there might be the possibility of an even higher return given management’s believe that, in 2024, EPS will be $7 and $4 billion of free cash is possible.

Risks

The odds of a U.S. recession are rising, and the chances it will be mild are falling. This might very well mute demand for flights in the short to medium term. Historically, airlines have suffered due to recessions and this might be the case again. While it appears as if the risk is moderate right now due to the countercyclical phase of the airline industry, this is yet to be proven in 2023. An offsetting factor to this risk is the fact that airline industry revenues are still $20 billion to $30 billion below the historical trend vs. GDP in the U.S., highlighting the significant recovery opportunity still ahead.

Delta Air Lines currently has $20.5 billion in net debt. Per management, 17% of the debt is variable and the rest fixed. In 2021 the company paid almost $1.3 billion in interest, which was $1 billion greater than 2019. In 2022 that number will be close to $1 billion, creating a significant hole in profitability for the time being. Management is currently paying off the debt at about $5 billion per year and aims to have net debt down to $15 billion by 2024, which – compared to Q3 2019’s $10.2 billion – is healthy, considering everything that the industry had to go through during COVID-19.

Management has also stated that it will aim to improve Delta Air Lines’ investment grade rating back to pre-COVID levels, which we believe will be a positive and a possible catalyst for further share appreciation. A more favorable investment grade will help secure better debt terms when bringing more of the airline’s capacity back online and will support further expansion. The debt burden and interest expense of at least $500 million will be around for at least another one to two years. This will continue to be an overhang, but we believe the direction of the debt levels is positive and the risk is moderate due to the majority of interest rates being fixed.

Conclusion

The risks mentioned in this analysis are, in our opinion, temporary problems. We definitely see a route to capital appreciation for Delta Air Lines, and once fuel costs come down we believe holding a high-quality company with minimal downsides like Delta Air Lines in your portfolio is a positive.

Be the first to comment