viper-zero

Those who have been following my work know that I’m not a huge fan of investment in the airline industry. That was not a mindset that grew during the pandemic, but was driven by previous investment experience in airlines in a world where there was no pandemic, no sky-high inflation and no labor shortages. However, that does not mean that I don’t see opportunities for fruitful investment in airlines. Delta Air Lines (NYSE:DAL) is one of the names that I’m particularly upbeat on. In this report, I will have a look at what we can expect from the US airline in the fourth quarter and what the risks and opportunities are.

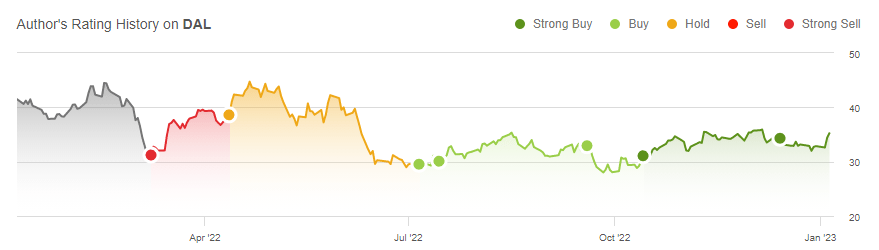

From Strong Sell To Strong Buy

Earlier this year I had a strong sell rating on Delta stock and by now I have a strong buy rating. So that requires some explanation before I proceed. So, what made me hesitant on Delta Air Lines shares? That actually was just the surge in oil prices, which at times are a prelude to a recession which led me to believe that we could eventually face extreme softening in demand and profitability as a result. So, the strong sell rating was solely based on that. In some way, a strong sell rating was actually also not what I should have tagged my report with as I did point out that doomsayer’s analysis were not considering all elements of the high fuel environment and I did point out the following:

I already decided years ago that airlines were just not my cup of tea and divested, but as a trade rather than an investment, Delta Air Lines does offer opportunities for the investor with nerves of steel. More worrying to me is that oil price surges historically have been a prelude of recessions, which likely would have more grave implications for the global economy and the airline industry.

So, I saw both the risks as well as the opportunities, and with that in mind, the sell rating was poorly chosen. What I insufficiently accounted for at the time was the fact that despite high energy prices and labor costs the air travel demand environment was so big that airlines could easily pass through costs in the form of higher fares. The classic demand-supply mechanism was in full swing.

Author rating Delta Air Lines (Seeking Alpha)

Maybe the call was not extremely poorly chosen when viewing the rating timeline in a broader scope of months. From March 2022 until July 2022, Delta Air Lines stock appreciated significantly only to end up lower compared to the sell call. That’s what I meant with the stock being somewhat more rewarding at the time for short-term swings rather than long-term investment. In July 2022, I published a new report discussing the buy opportunity for the airline’s shares recognizing that the company was facing challenges but was priced as if another crisis would hit tomorrow which given the pandemic crisis was extremely unlikely. Was it the right call? Most definitely. Shares have gained 21.4% since compared to 0.7% appreciation for the broader markets.

All too often, I see analysts but also readers sticking to their previous ratings because they simply are too proud to admit their thesis is not working out but that is not how you make money in the market. You don’t make money by saying “Well, I put this rating on the stock and the price movement is in the other direction so the market is wrong.” Sometimes that’s the case, but that’s only the case on rare occasions. I take a different approach toward things. I analyze a stock at a certain point in time looking at the cost and pricing environment and management comment which layers on top of my own analysis and at a later point in time I repeat and where needed I adjust my ratings and that is something that has helped me uncover rewarding investment opportunities. Turning a blind eye to evolving environments and sticking to emotions rather than rationale does not help you make better investment decisions but only leads to missing investment opportunities as the market is forward looking without much regard for the calls and stubbornness of analysts or readers.

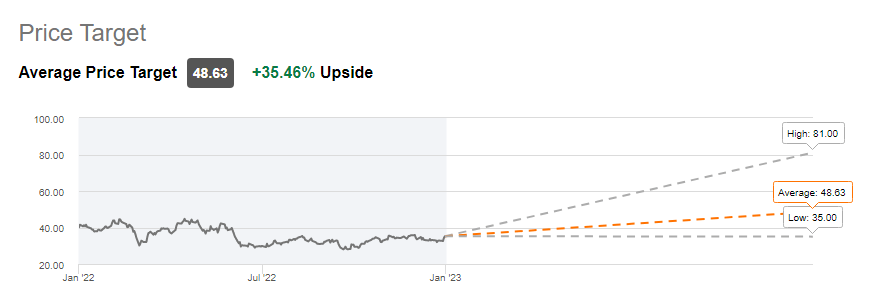

What Is Delta Air Lines Stock Worth?

Delta Air Lines price target consensus (Seeking Alpha)

Currently, Wall Street sees 35.5% upside from current levels. In my December piece, after Delta provided some targets toward 2024 I projected 35% to 95% upside for Delta stock. That huge spread between those two points was driven by differences in the assumed earnings multiple. However, since then we saw stock prices climb 6.7% compared to a 2% loss for the broader markets. So far things are playing out well and I continue to believe Delta Air Lines stock could fly even higher ultimately with a price in the range of $60 to $65 per share.

What To Expect For The Fourth Quarter?

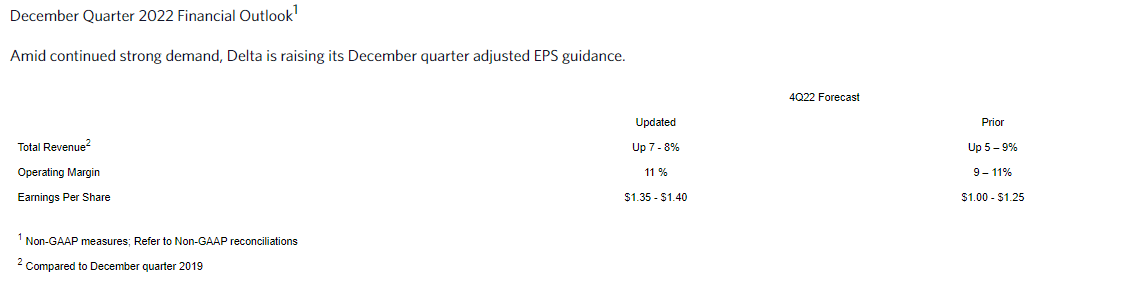

Delta Air Lines Q4 2022 guidance (Delta Air Lines)

In early December, Delta expected 7% to 8% higher revenue compared to the comparable pre-pandemic quarter with margins of 11% and $1.35 to $1.40 in earnings per share. That was an upbeat update to its earlier forecast for the fourth quarter. For the four quarter, the analyst consensus is $1.35 in earnings per share and a revenue of $12.39 billion. It will be interesting to see whether Delta will be able to get to those numbers.

During the winter storm that impacted flight schedules there was an understandable focus on the non-performance of Southwest Airlines (LUV) which will see a cost impact of $1.25 billion stemming from the chaos. It will be interesting to see what Delta Air Lines, which was the distant number two in terms of cancellations with 806 cancellations since the 25th of December, will see in cost pressure but I wouldn’t be surprised if we see the fourth quarter numbers being closer to what was expected in the initial guidance rather than what was presented in the most recent December guidance. If there’s a significant impact I would think that earnings could end up on the high side of the previously guided range.

Conclusion: Delta Air Lines Buy Rating Stays

Overall, I do expect a strong quarter with modest impact from the winter storm but the overall picture for Delta remains intact. I would not be too surprised if we see Delta’s figures closer to the previously guided range rather than the most recent guided range but overall I do believe that Delta Air Lines is positioned well to execute its 2023 and 2024 plan. So, any weakness that might be seen in Delta’s results is not a major concern to me and I believe that if there is a negative share price reaction that will provide another entry point for longer-term focused investors as demand is still strong and Delta Air Lines is pacing well on its value creation efforts.

Be the first to comment