Lisa Bronitt/iStock Editorial via Getty Images

It is time for yet another round of earnings reports by the major US-based airlines. As usual, my focus of attention will be on Delta Air Lines (NYSE:DAL) due to (1) the company’s relevance in the US air travel space and (2) the fact that DAL remains my favorite airline stock at the moment, certainly within the Big 3 legacy group.

Analysts expect revenues of $12.7 billion to rise 34% YOY, which would represent an annualized increase of just below 4% compared to the last pre-pandemic holiday quarter — yes, the COVID-19 crisis is very much over for air carriers. A projected EPS of $1.33, if achieved, would be a massive improvement over this time last year. But the figure would still fall a solid 22% below 2019 levels due, in great part, to higher fuel costs.

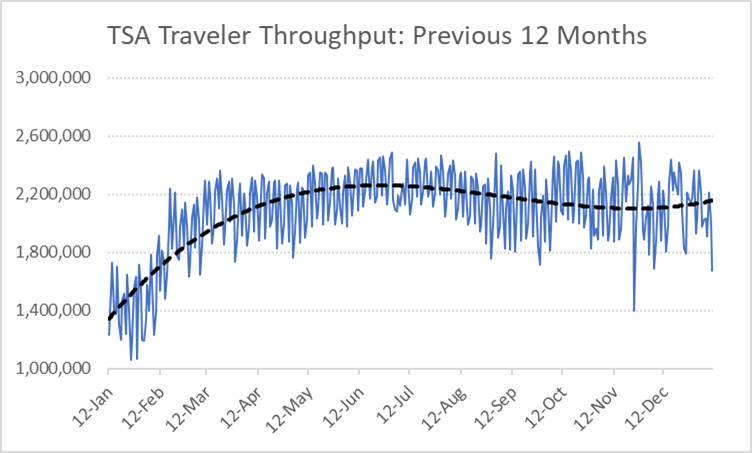

While Wall Street pros and investors will certainly glance at the numbers above on earnings day, as they usually do, I think that very little about Delta’s Q4 performance will matter to the stock. First, the recovery in air traffic is a well-known phenomenon (see chart below). Few fail to recognize that airlines have been undergoing a period of unusually strong demand driven by post-COVID consumer behavior that favors travel spending.

TSA.gov

Second, Delta has recently provided guidance for the quarter: revenue growth of 7% or 8% vs. 2019; op margin of 11%; and EPS of $1.37 at the midpoint of the range. So, it is unlikely that the Atlanta-based carrier will deliver numbers that deviate much from the company’s updated projections.

More important than the earnings print itself, I present next (1) what I believe to be the most important topic of conversation for DAL investors in the short term, followed by (2) my stance towards investing in the airline space today.

Striking the iron while it’s hot

It is hard to grasp how quickly the business landscape has changed for the airline industry in the past three years.

Grounded aircraft and lockdowns led passenger traffic at US airports to reach below 100,000 people per day at one point in April 2020, a 96% decline vs. only two months earlier. Now, carriers can’t seem to find enough seats to offer to their passengers, who in turn have been paying 36% more YOY (or 9% more compared to pre-pandemic levels) to board a commercial airplane.

Last quarter, Delta was able to fly only 63 billion seat miles, a 17% decline YOY. The company blamed “aircraft availability, regional pilot shortages, and hiring and training needs” for the sharp drop in capacity — an issue that is certainly not Delta-specific, to be fair. The recent spike in holiday-season flight cancellations has not helped to put airline investors at ease.

Now, Delta and its peers are faced with the challenge of (1) getting as many wheels off the ground as they can to address surging demand before (2) the global economic landscape deteriorates, which seems to be a consensus expectation for the new year. Delta’s ability to strike the iron while it is still hot is what I believe will be most important in determining the direction of the stock price in the foreseeable future.

DAL: a relative winner

Much more than a short-term trader, I prefer to invest in stocks for the long run and within the context of a diversified portfolio. This being the case, I like to allocate my money to assets that are:

- Generally resilient to fluctuations in economic activity: very bad news for the highly procyclical airline space, whose stock prices tend to endure some of the most dizzying levels of volatility in the market.

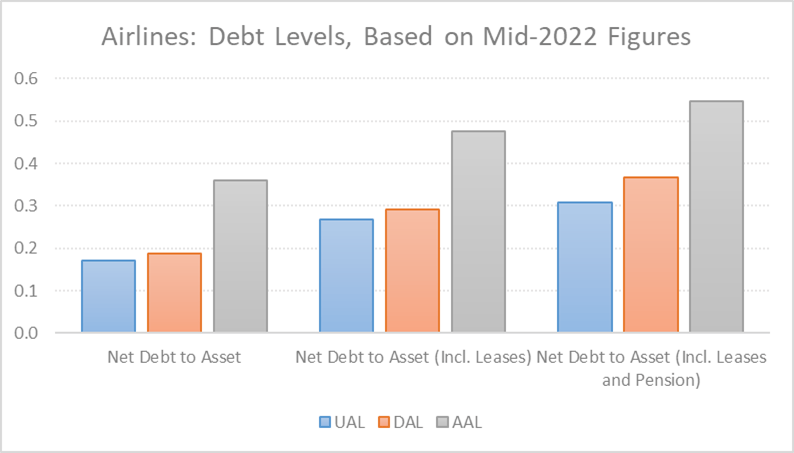

- Of high quality: good news for DAL, given the company’s relatively low levels of debt (see chart below) and strong competitive position in profitable markets, both domestically and internationally.

DM Martins Research

In the end, I am highly skeptical of the airline sector today, especially when we do not seem to be in the earlier stages of economic expansion. Quite the opposite, in fact: think of how hard central banks have been trying to stall the global economy in the past 12 months to curb inflation. But if I were to pick a small group of airline stocks to either diversify my portfolio or to place a long-short trade, DAL would very likely be close to the top of my buy list.

It helps that Delta trades at a low 2023 P/E of only 7.6x, a multiple that looks even better if considering the company’s outlook of over $7 in EPS in 2024 for a guided bottom-line growth rate of 17% at the very least, if not much more.

Be the first to comment