Martin Poole/DigitalVision via Getty Images

Introduction

Deckers Outdoor (NYSE:DECK) shares have risen 7% YTD. Since my first publication on November 3, 2022, the stock is up 19.4%, outperforming the S&P index, which is up 10%. In addition, the company published its financial report for Q3 23 (fiscal), which turned out to be better than investors expected. I decided to take a quick look at reporting and make changes to my model.

The survey of 3Q 23 (fiscal) results (Q4 calendar)

Despite difficult macro headwinds, the company continues to demonstrate growth in revenue and operating margins. First of all, I would like to mention the HOKA brand, where revenue growth for the quarter amounted to 90.8%. In addition, revenue growth in the DTC (Direct-to-Consumer) segment continues to support the operating margin of the business.

Revenue growth in Q4 2022 (3Q23 fiscal) was 13.3%. In the Direct-to-Consumer (DTC) segment, revenue grew by 18.7% YoY, in the wholesale segment, revenue growth was 8% YoY. International sales were up 12.1% YoY, while domestic sales were up 13.9% YoY.

Gross margin increased from 52.3% in Q4 2021 to 53% in Q4 2022 (fiscal). SGA spending (% of revenue) decreased from 27.6% in Q4 2021 to 26% in Q4 2022. Thus, the operating margin of the business increased from 24.7% in Q4 2021 to 27% in Q4 2022.

You can see the main reporting details in the charts below.

Financial results (Official site)

The HOKA and Teva brands continue to be the main revenue drivers. HOKA sales were up 90.8% YoY to $352.1 million, while Teva sales were up 48.3% YoY to $30.5 million.

Financial results (Official press release)

Projections

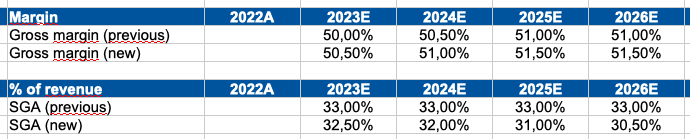

I decided to make small changes to my model based on updated comments from management, my own expectations, and the company’s reporting. Thus, I changed my forecast for gross margin and SGA expenses. In my personal opinion, thanks to the increase in the share of revenue in the DTC segment, the ability to raise prices and the growth of economies of scale, the company will be able to demonstrate an improvement in profitability and cost reduction (% of revenue).

You can find the results of my predictions and details of their change below.

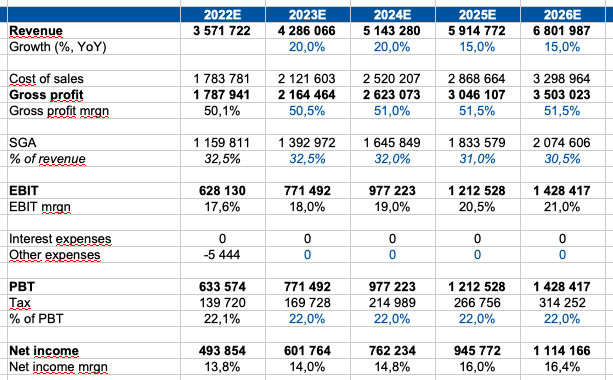

Forecast (Personal calculations)

Thus, my forecast of future cash flows is based on the following inputs:

Revenue growth: I assume that the company will show revenue growth of 20% by the end of 2020, then I predict a decline in revenue growth to 15% by 2026 against the background of the high base effect of previous years.

Gross margin: I predict that the company will show an improvement in gross margin to 51.5% by 2026 in terms of increased economies of scale, strong positioning and the ability to effectively raise prices for their products.

SGA: I believe that increasing economies of scale will reduce operating costs (% of revenue), so I predict a decline from 32.5% in 2022 to 30.5% by 2026.

Tax: I forecast tax spending at 22% of PBT until 2026 according to management comments.

Yearly projections:

Income statement (Personal projections)

Valuation

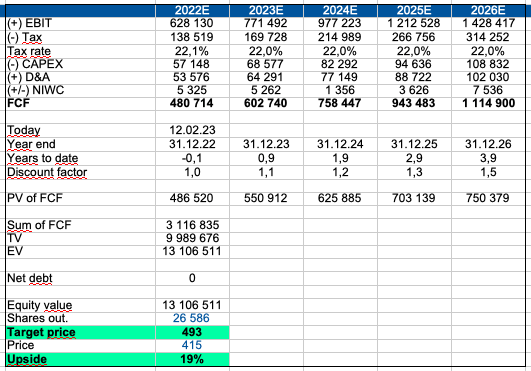

To value a company, I use the DCF method because building a DCF model allows me to take into account changes in revenue growth and operating margin in the future. In addition, the history of the company’s financial statements allows you to make assumptions about future cash flows and changes in operating costs. In addition, the company operates in a stable market where the use of DCF is most preferred.

Basic input data for calculations:

WACC: 10.8%

Terminal growth rate: 3%

DCF model (Personal calculation)

Multiples

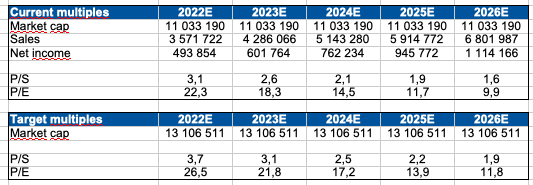

In addition, I calculated current and future P/S and P/E multiples based on my sales and net income projections. You can see the results of my calculations in the chart below.

Multiples (Personal calculations)

Drivers

Macro: decrease in inflation, growth in real incomes and recovery in consumer confidence may have a positive impact on consumer spending, which may support the dynamics of business revenue in the next periods.

Channel mix: increasing the proportion of sales coming from the DTC channel could further boost operating margins

Margin: increasing economies of scale, effective management of operating costs and higher prices could support margins going forward.

Risks

Macro: rising inflation and a decline in real income may lead to a reduction in consumer spending, which may have a negative impact on the dynamics of business revenue growth.

Margin: changing consumer preferences, rising marketing costs due to increased competition, inability to efficiently raise prices for core products, and reduced economies of scale can all result in lower operating margins for a business.

Conclusion

The company continues to post relatively strong revenue growth despite a decline in real incomes and declining consumer confidence. In addition, increasing economies of scale, increasing core product offerings and the opportunity to increase the share of more profitable sales channels allow the company to not only maintain operating margins against the backdrop of macro headwinds, but also show improvements. Thus, after making changes to my forecasts, I decided to increase the target price from $415 to $493 per share of the company. So, I still stick to my Buy recommendation for the company’s stock.

Be the first to comment