akinbostanci/iStock via Getty Images

Introduction

Are you looking for a high-growth investment opportunity in the technology sector? Look no further than Datadog (NASDAQ:DDOG), a leading provider of cloud monitoring and analytics solutions. With the cloud and DevOps market projected to grow at a CAGR of 24.5% between 2022 and 2027, DDOG is perfectly positioned to capitalize on this growth with its cloud-native monitoring and analytics platform.

With over 12,000 customers, including major brands such as Adobe (ADBE), Airbnb (ABNB), and Spotify (SPOT), and strong partnerships with major cloud providers, DDOG has a solid foothold in the market. Don’t miss out on the potential for significant returns as DDOG continues to scale its platform and expand its offerings, and enters new markets like APM and Log Management. Make sure to put this company on your watchlist.

A Leading Provider of Cloud Monitoring and Analytics Solutions

As technology continues to advance at a rapid pace, more and more companies are turning to data-driven solutions to stay competitive. One company that has made a name for itself in this space is Datadog, a leading provider of monitoring and analytics solutions for modern cloud applications.

But before we dive into the investment opportunities, let’s take a look at the background of DDOG. The company was founded in 2010 by Olivier Pomel and Alexis Lê-Quôc, who saw a need for a more comprehensive and user-friendly solution for monitoring cloud applications. With their experience in the field, they set out to create a tool that would make it easier for developers to understand and optimize their applications.

The result was Datadog, a platform that allows developers to monitor and analyze their applications in real-time, providing them with the insights they need to improve performance and prevent issues. The platform quickly gained traction, and by 2012, DDOG had raised $6 million in funding from venture capital firms such as RTP Ventures and Index Ventures.

Since then, DDOG has continued to grow and evolve. The company went public in 2019 and has since seen its stock price soar, thanks to the increasing demand for cloud-based solutions and the company’s ability to meet that demand. Today, DDOG is valued at over $20 billion and is considered one of the leading players in the cloud monitoring space.

Capitalizing on the Booming Cloud and DevOps Market with a Leading Platform and Strong Partnerships

As an investor, it’s essential to understand the investment thesis for a company before putting your money into it. In the case of Datadog, the investment thesis centers around the growth of the cloud and DevOps market, and the company’s position as a leading player in this space.

The cloud and DevOps market is projected to grow at a compound annual growth rate (CAGR) of 20.3% between 2020 and 2027, reaching $11.3 billion by 2027. This growth is driven by the increasing adoption of cloud services and the shift towards DevOps practices in software development. Datadog, with its cloud-native monitoring and analytics platform, is well-positioned to capitalize on this growth.

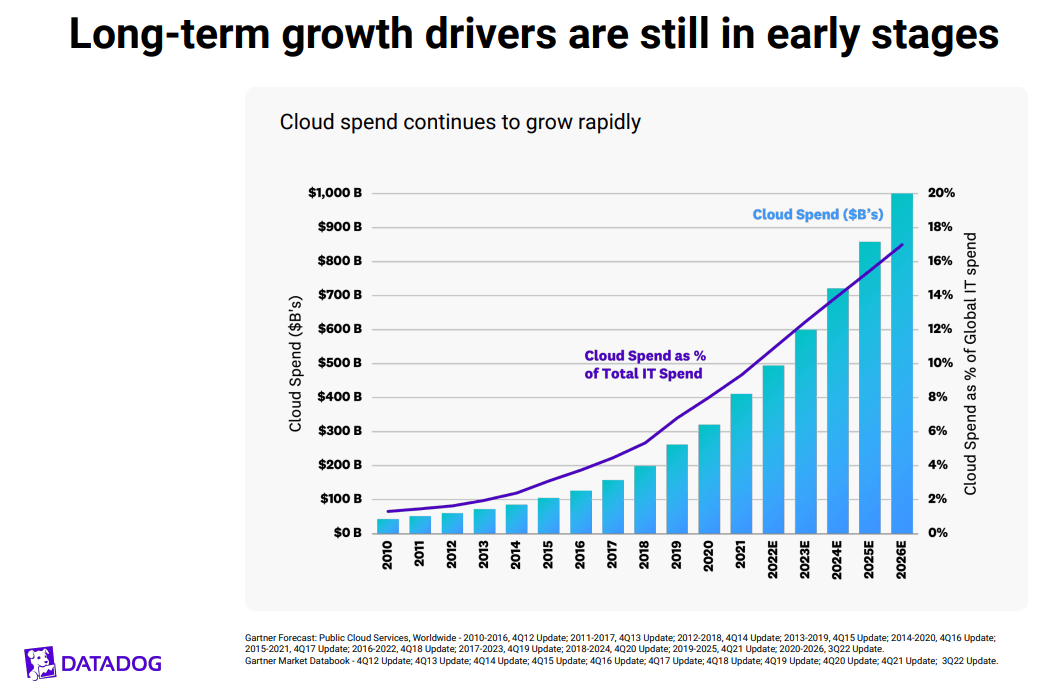

Long-term growth drivers still in early stages (Datadog Investor Presentation)

Datadog’s platform offers a comprehensive suite of tools for monitoring, troubleshooting, and optimizing cloud infrastructure, applications, and logs. The company’s platform is used by over 12,000 customers, including some of the world’s leading brands such as Adobe, Airbnb, and Spotify. This customer base, along with the company’s strong partnerships with major cloud providers such as AWS, Azure, and GCP, gives Datadog a solid foothold in the market.

The company’s recent IPO in September 2019 was a success, with its stock price rising over 100% in its first day of trading. This strong performance is a testament to the market’s confidence in Datadog’s potential for growth. As the company continues to scale its platform and expand its offerings, it is likely to attract more customers and increase its revenue.

Furthermore, Datadog’s focus on expanding its product offerings and entering new markets, such as the APM and Log Management markets, can fuel further growth for the company. Additionally, the increasing adoption of cloud services and DevOps practices by enterprise customers presents a significant opportunity for the company to expand its customer base and increase its revenue.

In summary, the investment thesis for DDOG centers around the growth of the cloud and DevOps market, and the company’s position as a leading player in this space, along with its strong partnerships, comprehensive suite of tools, and expanding product offerings, these factors make DDOG a compelling investment opportunity with the potential for significant returns.

Opportunities for Growth: DDOG’s Position in Cloud Computing, Data Analytics, IoT and Open-source Software

As an investor, there are several opportunities for growth in DDOG, a technology company that specializes in distributed systems and databases. One key area for growth is the increasing demand for better data management solutions, as more and more businesses rely on data to drive decision-making and innovation. DDOG’s expertise in distributed systems and databases positions the company well to meet this demand.

Another opportunity for growth is the growing trend towards cloud computing, as more companies move their operations to the cloud to take advantage of its scalability and cost savings. DDOG’s ability to provide robust, cloud-native solutions will be a major asset in this market. Additionally, DDOG’s focus on providing open-source software, which allows for greater flexibility and customization, will appeal to many companies. Furthermore, DDOG’s strong partnerships with major tech players such as Microsoft and Google have helped the company to gain a significant market share in the industry.

Datadog Investor Presentation

Finally, the company’s ability to provide end-to-end solutions, from data collection and processing to analytics and visualization, will also be a major advantage. All of these factors, combined with a strong management team and a solid financial position, make DDOG a compelling investment opportunity with the potential for significant growth in the future.

Basically, if we want the stock price to increase exponentially in the future, DDOG would need to continue to grow its market share and expand into new markets, while also continuing to innovate and develop new products and services. Additionally, the company would need to continue to generate strong financial results, with consistent revenue and earnings growth, to demonstrate its ability to deliver value to shareholders. If DDOG can achieve these things, the stock could see substantial gains in the future. There are several key opportunities that could fuel further growth for DDOG, and potentially drive the stock price up. One of the biggest opportunities for the company is the continued expansion of the cloud computing market. As more and more companies move their operations to the cloud, the demand for DDOG’s services and products is likely to increase. Additionally, the company’s focus on data analytics and machine learning could also prove to be a major growth driver, as more companies look to harness the power of big data to gain a competitive edge.

Another major opportunity for DDOG is the increasing adoption of the Internet of Things (IoT) and the growing need for real-time data processing. The company’s ability to provide real-time data processing and analytics services could make it a go-to provider for IoT companies, which could further drive growth.

Overall, DDOG’s strong reputation and innovative technology make it well-positioned to capitalize on these and other opportunities in the market. Investing in DDOG could prove to be a smart move for investors who are looking for a high-growth stock with strong long-term potential.

Assessing the Risks of Investing in High-Valued SaaS Company Datadog

Investing in the Software-as-a-Service (SAAS) industry can be a high-risk venture, as valuations for companies in this sector have been known to reach stratospheric levels. One such company, Datadog Inc., has seen its share price drop 58% from its all-time high, but it is still richly valued at 19.6 times EV/Gross profit and 66 times EV/EBITDA. This is well above the industry average, making DDOG a riskier investment.

One of the main risks for DDOG is the company’s high valuation compared to its peers. The SaaS industry is known for high valuations, with some companies valued over 100 times sales during the peak of the 2021 mania. DDOG’s peers are also down, with Twilio being beaten down the most at 82%. This means that investors are paying a premium for DDOG’s stock, which could result in a significant loss if the company does not perform as well as expected.

Another risk for DDOG is the economic uncertainty that the company operates in. Management’s tone in the latest earnings call was upbeat, with no clear indication of a slowdown. However, the company provided cautious guidance for the fourth quarter, with revenue projected at $447 million, a 37% YoY growth. This cautious guidance, along with management’s emphasis on economic uncertainties, suggests that there is a high chance that the company will beat its guidance. However, this also means that the company is operating in a challenging economic environment, which could negatively impact its growth prospects.

Finally, dilution is another risk that DDOG investors should be aware of. The company’s multiples are falling, which could lead to higher dilution from SBC. This dilution could lower the returns for DDOG investors, making it a riskier investment.

In conclusion, DDOG is a riskier investment due to its high valuation compared to its peers, the economic uncertainty it operates in, and the potential for dilution. Investors should be aware of these risks before investing in the company and consider them alongside the company’s growth prospects.

Financials and Peer Comparison

Investing in the technology sector can be a lucrative opportunity for those looking to capitalize on the digital transformation and cloud migration trends that have been driving growth in recent years. One company that stands out as a particularly attractive option is Datadog, a leading provider of monitoring and analytics solutions for modern applications and infrastructure.

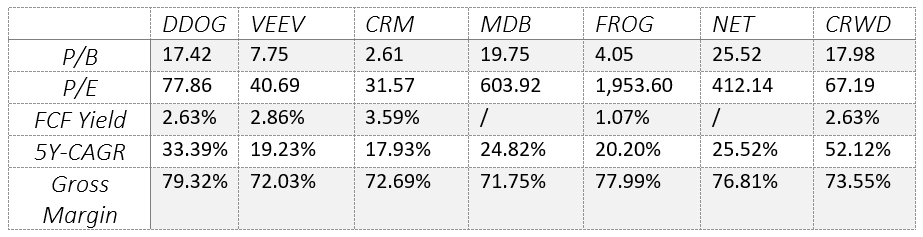

Financial Metrics of DDOG and Peers (Stock Info with Seeking Alpha)

When it comes to financial performance, DDOG compares favorably to its peers. The company boasts a price-to-book ratio of 17.42, which is significantly higher than that of competitors Veeva Systems (VEEV) and Salesforce (CRM) at 7.75 and 2.61, respectively, but similar to CrowdStrike’s (CRWD) P/B of 17.98. This indicates that DDOG is trading at a premium to its peers and is seen as a more valuable company in the eyes of investors, this is due to the fact that CRM and VEEV are both more established companies already while DDOG should still have more growth ahead of itself as can be seen in some of the other metrics we discussed.

DDOG also has a decent free cash flow yield of 2.63%, which is lower than that of VEEV and CRM at 2.86% and 3.59% respectively. Furthermore, DDOG has a higher 5-year CAGR of 33.39% compared to its peers VEEV and CRM at 19.23% and 17.93%. This highlights DDOG’s strong revenue growth and ability to generate cash, which in a later stage might fuel FCF yield and further shareholder returns.

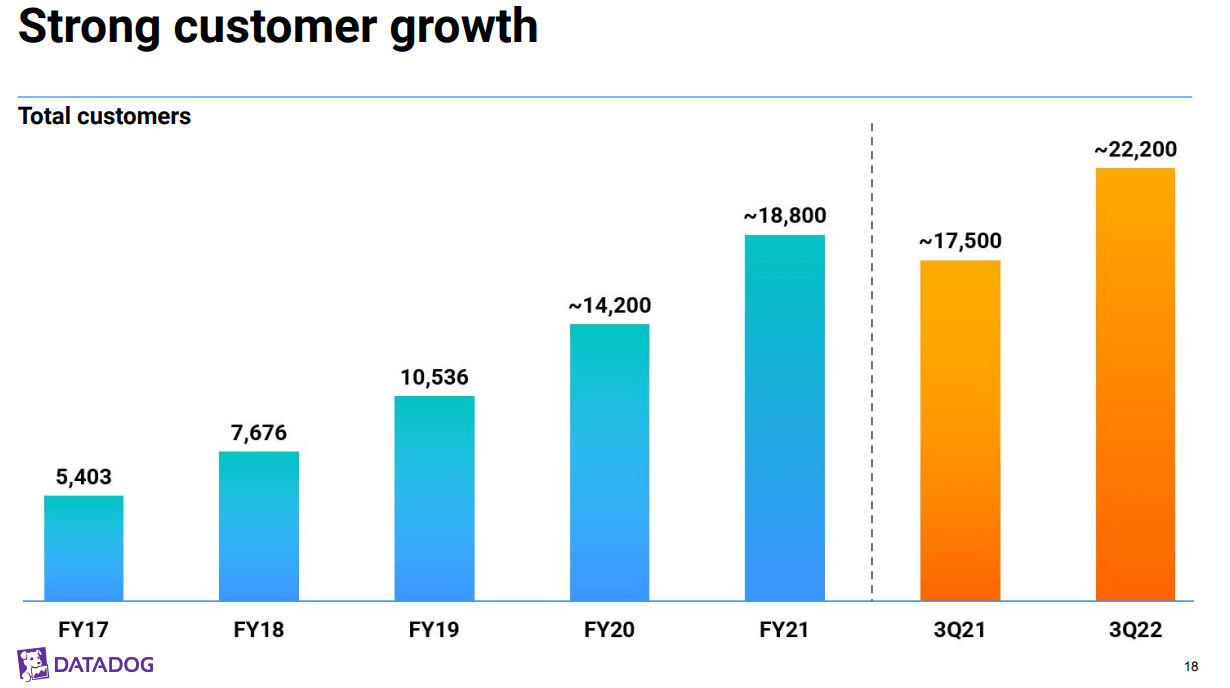

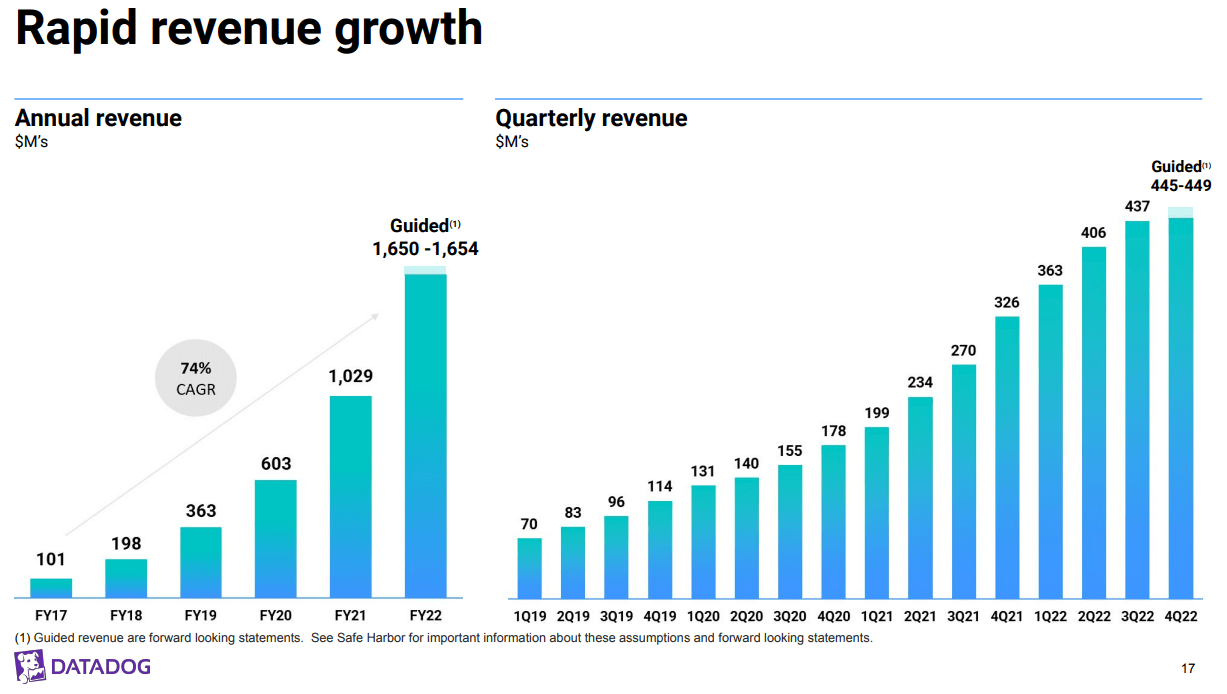

Rapid Revenue Growth (Datadog Investor Presentation)

Another key metric to look at when evaluating a company’s financial performance is gross margin. DDOG has a gross margin of 79.32%, which is higher than that of MongoDB (MDB), Cloudflare (NET), and JFrog (FROG) at 71.75% and 77.99% respectively. This is a positive sign for DDOG as it suggests that the company is able to effectively leverage its resources and maintain a strong level of profitability and pricing power.

In summary, DDOG’s strong market perception, solid cash flow generation, impressive historical growth, and high profitability make it a compelling investment opportunity in the software-as-a-service (SAAS) industry. Its numbers are indicating a strong and sustainable growth in the future and its numbers are above industry averages. It is worth noting that DDOG’s strong financial performance and fundamentals, make it a solid choice for long-term investors seeking to capitalize on the ongoing digital transformation and cloud migration trend. It is crucial to consider that while the company may experience further decline in the immediate future, given the current economic climate. However, it is also important to note that the company’s valuation, while relatively high when compared to certain competitors, is still well-positioned to capitalize on long-term growth opportunities.

Technical Analysis

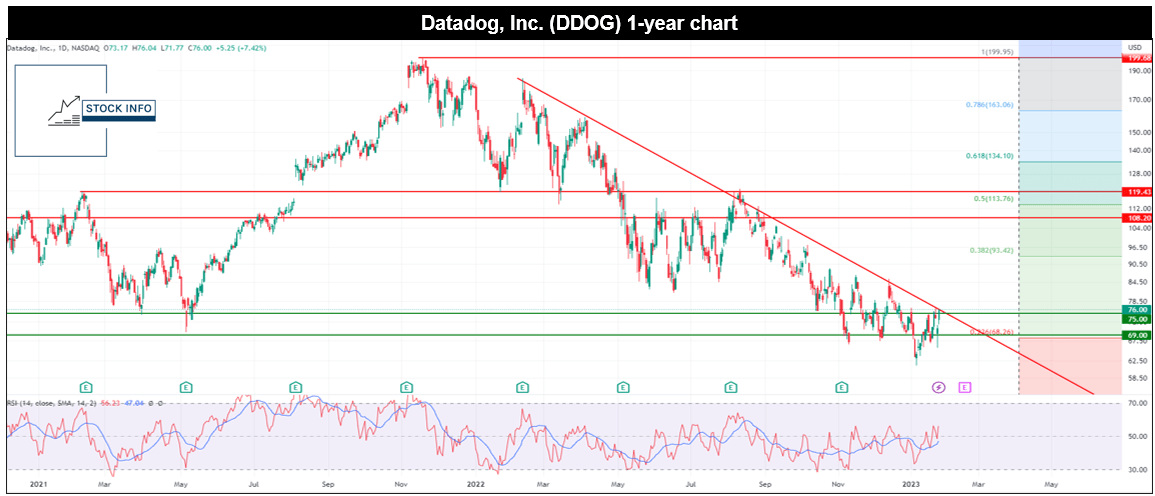

As can be seen in the chart below the company is currently in a downtrend, as most other high growth companies over the last year. The company is currently still down close to 62% since its all-time high at the end of 2021.

Stock Info with TradingView

We have to be honest, the company got ahead of itself at that time. An environment with endless money printing and new investors getting into the market fueled the stock price to incredible highs. DDOG went up 186% in just over 6 months from the Covid-19 bottom to its all-time high.

Currently, the stock is fighting the downtrend again. A breakout above the red trend line resistance would be a very bullish sign. In addition, the $75 level could provide decent support, which could make this quite an interesting buying opportunity if this is the start of a new bull market.

That said, we don’t think this bear market is over yet, but companies like DDOG might not suffer as much as other companies in a recession. Although this might be the case, the stock could revisit the $60 level again. Earnings and earnings guidance in particular will be important to give some direction.

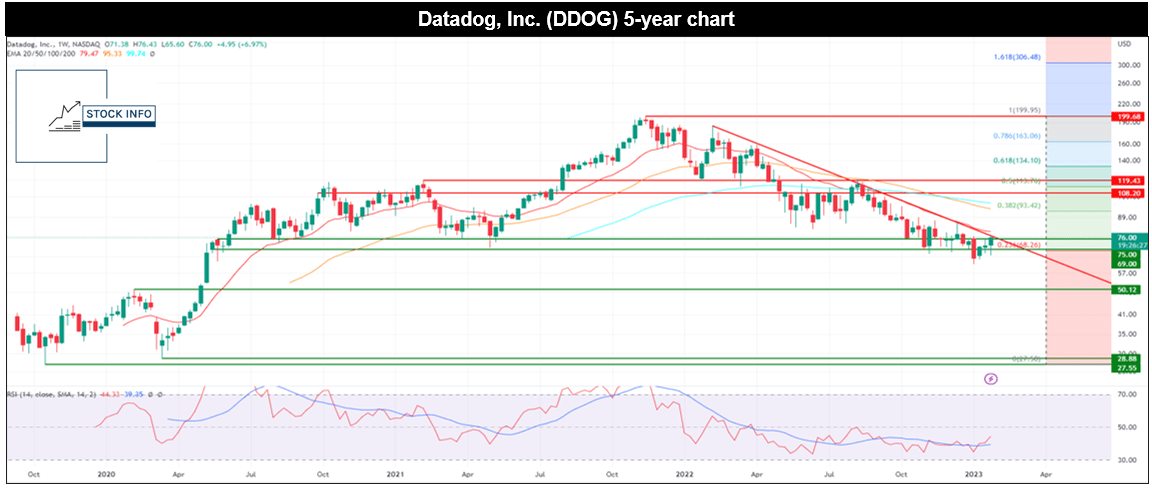

Stock Info with TradingView

When we take a look at the long-term chart, we can see the company is still way above its covid-19 low and its 2019 high of $50. The company has improved significantly over that time, should the company revisit the $50 level it would provide an incredible buying opportunity. The stock is currently hovering below all of its WMA’s, these levels could provide some resistance in the future as well.

Conclusion

In conclusion, Datadog is a leading provider of cloud monitoring and analytics solutions, perfectly positioned to capitalize on the projected growth of the cloud and DevOps market. With over 12,000 customers and strong partnerships with major cloud providers, DDOG has a solid foothold in the market. The company’s IPO was a success, and as it continues to scale its platform and expand its offerings, it is likely to attract more customers and increase its revenue.

Additionally, DDOG’s focus on expanding its product offerings and entering new markets, such as the APM and Log Management markets, can fuel further growth for the company. With its comprehensive suite of tools, expanding product offerings, and strong partnerships, DDOG is a compelling investment opportunity with the potential for significant returns. Therefore, we give DDOG a buy rating, as we believe it is an enticing opportunity for investors with a long-term horizon.

Be the first to comment