mozcann/E+ via Getty Images

Investment thesis

Datadog (NASDAQ:DDOG) will report 2022 Q4 earnings on the 16th of February before the market opens. There are several factors, in my opinion, that point in the direction that shareholders should be more excited than usual.

Among these factors, the leading one is not surprisingly the significant slowdown in the growth of hyperscalers. However, other factors like Datadog’s strong SMB presence, its usage-based pricing model, or the particularly strong 2021 Q4 numbers that will serve as yoy comparisons are also in play.

Furthermore, I believe the better-than-expected earnings of main competitor Dynatrace (DT) – on which Datadog shares rallied more than 10% – could give investors a false sense of security. This could have set the bar higher for Datadog leaving investors more vulnerable in case of a possible disappointment.

Finally, Datadog will provide guidance for its fiscal 2023, which could be another source of concern in my opinion. These risk factors make us say that it’s better now to lean back and switch to a wait-and-see approach until the dust settles. However, in the long run, I believe owning Datadog shares is a must for investors in growth stocks.

Continued beat-and-raise requires sacrifice

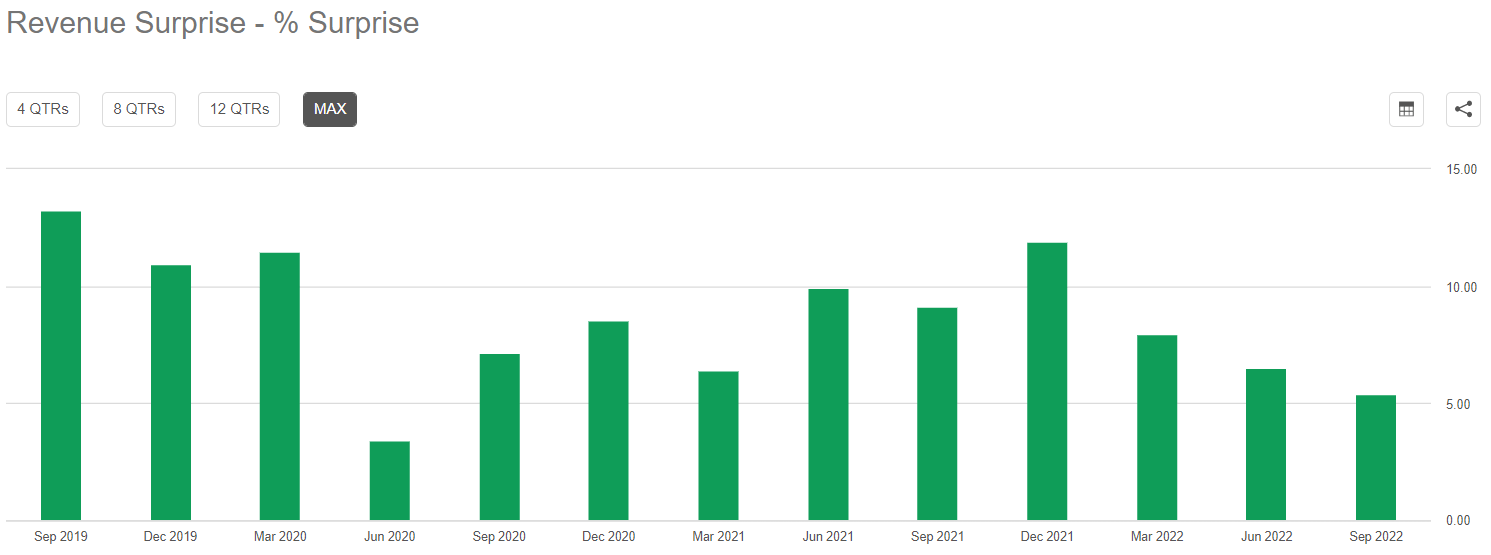

Datadog has been a classic beat-and-raise growth story since its IPO back in September 2019. This also persisted during 2022, when many other SaaS companies began to disappoint investors. Even during the beginning of Covid, when there was a sudden cutback in enterprise spending, the company managed to exceed expectations on the top line:

Seeking Alpha

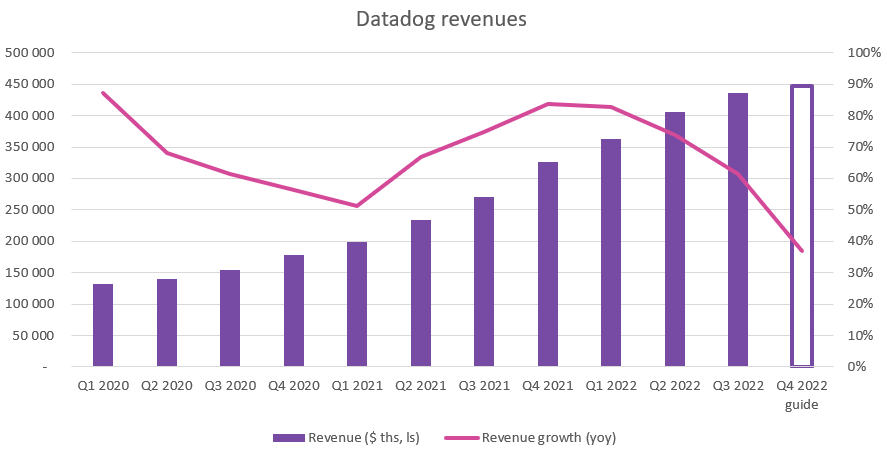

From the chart above, we can see that the magnitude of revenue beats has decreased recently to some extent, although this equaled still a ~5% beat in 2022 Q3. Management tried to ensure that this tendency continues into Q4 as they provided a somewhat soft guidance for the quarter in my opinion:

Created by author, based on company filings

The chart above shows that after growing 61% yoy in Q3 management guided for 37% yoy growth in Q4 trying to leave the door open for another beat. I think this should be possible as it would only take a 2-3% sequential increase in revenues, although the exceptionally strong Q4 quarter a year ago makes yoy growth rates harder to beat.

What is more concerning in my opinion, that if management wants to stick to the usual strategy of guiding extremely careful only to significantly overdeliver afterwards, the initial guide for fiscal 2023 when releasing 2022 Q4 earnings could be quite disappointing. Currently, analyst consensus for fiscal 2023 yoy revenue growth stands at ~32%. If topline growth slows to the ~40% levels for Q4 (assuming a small beat) continuing its softening trend, I doubt that management will provide a 30%+ yoy growth guidance for 2023.

I believe this could rattle investor confidence in the short run as everyone got used to the same old beat (and raise). Something similar happened to CrowdStrike (CRWD) back in November, which made eventually shares more investable in the aftermath but came with significant short-term pain. I am not saying that this definitely has to happen to Datadog, but I see heightened risks for this scenario. In the following, I want to discuss why I see it this way.

Unprecedented slowdown at hyperscalers

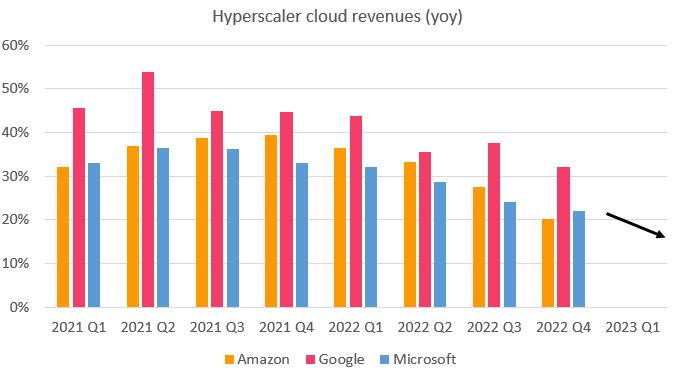

Although Datadog constantly outperforms the revenue growth of major cloud providers, it won’t be able to escape the broad-based slowdown evidenced at the cloud units of these companies:

Created by author, based on company filings

I believe that the most concerning from the perspective of Datadog is that both Amazon (AMZN) – the company’s most important partner – and Microsoft (MSFT) management talked about further weakening throughout December and January, suggesting no sharp reversal in sight. This is another argument in the favor that Datadog management will approach 2023 cautiously and provide a conservative guidance for the year that could disappoint investors.

SMB exposure and usage-based pricing pose further risks

Another important risk factor in my opinion is that Datadog has significant exposure to the SMB segment, which segment based on management comments from Amazon and CrowdStrike (and others as well) tends to cut back most on IT spending in the current downturn. Although Datadog management added on the Q2 earnings call that SMB spending on its platform is still resilient, I believe this cannot hold for long when we look at the trends at other companies.

A further risk in the current market environment lies in Datadog’s overwhelmingly usage-based pricing model. Although this model is used to serve well in the long run, it provides customers a high degree of flexibility in uncertain economic times to exercise cost control. Although the services of Datadog are mostly mission-critical to its customers, I think there are always some workloads that can be mitigated.

Finally, as most of Datadog’s customers have switched from a do-it-yourself approach in observability to the company’s platform, I believe these customers could have extra motivation to hold onto their existing DIY technologies in order to reduce costs. This could slow the net expansion of Datadog and even the acquisition of new clients.

I believe the factors stated above make Datadog vulnerable to the current economic downturn that should be reflected in the company’s fundamentals rather sooner than later.

Dynatrace earnings could give a false sense of security

One of the main competitors of Datadog, Dynatrace reported earnings on the 1st of February, surprising investors in a positive way (for details see my article: “Dynatrace Fiscal Q3 Earnings: Strong Enterprise Focus Provides Resilience”). Shares rallied 16% that day, with Datadog share price also increasing in sympathy by 10%. I believe the market has judged too quickly, as there are important differences between the two companies.

Although both companies compete for the “best-of-breed qualification” in observability, Dynatrace solely focuses on enterprise customers who tend to be more resistant in the current downturn. Furthermore, the company operates a subscription-based pricing model, providing customers less optionality to decrease spending on the platform from one day to another. Finally, Dynatrace has already made two guidance cuts in the preceding quarters, setting the bar very low for most recent earnings. I believe Datadog has still work to do on that front.

With this, I believe the expectations that Datadog earnings will positively surprise investors have grown further, which could turn into another source of disappointment in the end.

Conclusion

I regard Datadog shares as an excellent long-term investment opportunity. However, in the short run, there are several factors which prevent me from investing in the shares right now. If 2023 estimates get significantly de-risked after Q4 earnings, there could be a good risk/reward opportunity to buy shares.

Be the first to comment