Scott Heins

We cautioned investors to expect a massive slowdown in our previous article on Daqo New Energy Corp.’s (NYSE:DQ) growth momentum moving ahead as our thesis played out accordingly.

DQ posted a decline of nearly 35% from its November highs, even as it moved into its seasonally strong Q4. Even though management was confident of a strong finish in its Q3 commentary, the reality has not followed its optimism.

Notably, polysilicon prices in China have plunged to RMB164/kg as of January 3, which is likely even worse than management had anticipated. As a reminder, Daqo CEO Longgen Zhang highlighted in its Q2 commentary in August 2022, prognosticating a moderation toward the RMB250/kg zone in H1’23 before normalizing further to RMB190/kg (midpoint) in H2’23.

As such, the significant decline has likely not been contemplated, even as Daqo continued to add capacity, which is expected to reach “305,000 MT by the end of 2023.”

Daqo is still expected to lead the industry as it ramps capacity, helping to improve its scale efficiencies. However, with a waterfall decline in polysilicon prices, we believe the consensus estimates are likely due for a massive cut, which could also stretch into 2024 projections.

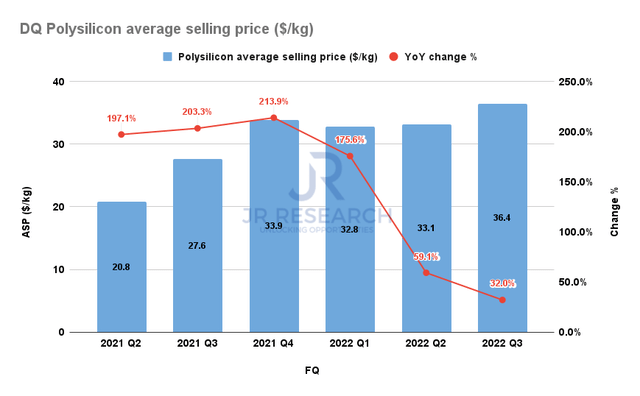

Daqo Polysilicon ASPs (Company filings)

Notably, the last time Daqo posted ASPs lower than the current market pricing was in Q2’21 when Daqo averaged $20.9/kg for its polysilicon. The current pricing dynamics suggest the spot prices have fallen to about $24/kg. We believe more over-optimistic Daqo bulls certainly didn’t see this coming.

Can it get worse than this? With an oversupply that preceded its recent battering, polysilicon customers were reported to be in a wait-and-see mode, as they anticipated prices to fall.

Given that spot prices were close to the RMB250/kg level in the third week of December, it’s possible some customers could have seen a more attractive opportunity to return to the market.

Furthermore, with China’s reopening from its harsh COVID lockdowns, it should spur a revival in the country’s demand outlook, as record polysilicon prices beset the solar industry in 2022.

Hence, we believe that the normalization phase is healthy for the industry, as record prices are not sustainable in the long term.

But does it mean that the opportunity in DQ is appropriate for investors to consider “buying the dips” after its sharp decline from its November highs?

DQ last traded at a NTM EBITDA multiple of 0.3x, well below its 10Y average of 5x. Is it cheap? Yes, it seems absurdly cheap. But, as we highlighted earlier, we assessed that the consensus estimates have yet to be slashed to reflect the market’s reality.

If we used its earnings profile from its Q2’21 as a benchmark, investors shouldn’t be surprised to see its revenue drop by 30% to 40%, depending on the cost optimization from its new production facilities. But, we expect Daqo’s cost leadership to help maintain its robust profitability, mitigating the pricing impact, which should not cause its margins to crumble.

As such, we expect its EBITDA estimates to be slashed, lifting its EBITDA multiples to about the 3.5x levels. Hence, it’s still projected to be lower than its 10Y average, suggesting that a high level of pessimism has likely been priced in.

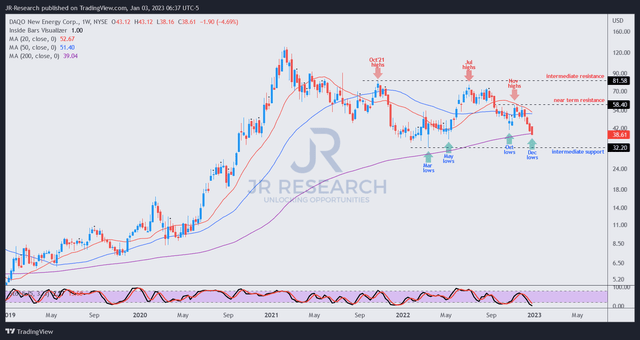

DQ price chart (weekly) (TradingView)

With DQ sellers taking out its October lows recently, market operators had likely already reacted to the supply glut and spot price collapse.

However, the critical question is whether a re-test of its March lows could be in the works?

We see that as a possibility, and buyers should assess whether March lows could hold robustly. Moreover, it coincides with the 200-week moving average (purple line), a critical defense zone for DQ buyers to undergird.

Hence, investors are urged to consider adding progressively, expecting further downside volatility to transpire.

Rating: Buy (Revise from Hold).

Be the first to comment