Chris McGrath/Getty Images News

Company overview

Daqo New Energy Corp. (NYSE:DQ) is a Chinese polysilicon manufacturer engaged in the manufacturing and selling of high-purity polysilicon to photovoltaic product manufacturers who process polysilicon into ingots, cells, and modules for solar power solutions. The company sells ready-to-use polysilicon packed to meet crucible stacking, pulling, and solidifying needs.

Investment case

Daqo had 105,000 tons of polysilicon capacity in operation, all located in Xinjiang. The company has been increasing its production capacity for a while now. Phase 5A of the Inner Mongolia project, with a 100,000 MT nameplate capacity, is currently under development and is scheduled for completion in the second quarter of 2023. With the recently announced Phase 5B project, the company’s total annual production capacity would rise to 305,000 MT by the end of 2023.

Growing polysilicon market: A major tailwind

In 2021, the total volume of the global polysilicon market was estimated at 585.6 tons. With a CAGR of 14.5% between 2022 and 2029, the market is projected to grow from 664.1 tons in 2022 to 1,718.0 tons by 2029. The production of solar cells is increasing, driving the demand for these products. The market is segmented into electrical components and solar photovoltaics. Projections indicate a significant increase in the solar photovoltaics market throughout the forecast horizon. Rapid expansion in solar photovoltaic systems worldwide is a substantial factor in this growth.

Producing power from renewable resources is a significant priority for the international economy. Due to environmental and climatic changes, there is a transition from carbon-based petroleum derivatives to cleaner alternative energy sources. About a quarter of the electricity produced by the power sector comes from renewable energy sources like solar, wind, and hydroelectric power. The growth of the polysilicon business would benefit significantly from a greater emphasis on renewable energy. Over the past decade, the worldwide renewable energy generation business has changed, and electricity-producing capacity has grown by about 8.0% yearly, as reported by the IEA. Sustainable growth in the energy sector is linked to fewer greenhouse gas emissions, less air pollution, lower operating costs, and a stronger system.

War in Ukraine is an additional Catalyst for a shift toward clean energy

In addition to the necessity of addressing climate change, which is a key factor in pushing clean energy reforms and supporting policies to accelerate the use of solar energy, the conflict in Ukraine has reminded stakeholders of the need for energy independence as higher natural gas and oil prices trigger an energy crisis in countries reliant on energy imports.

Solar PV technology is convenient and easy to install and is set for mainstream adoption in the next 20 to 30 years, as the price has now reached grid parity. Renewable energy has become more appealing as a result of rising energy prices, particularly in countries that are currently experiencing energy shortages and are looking for energy security for the future. With increasing global policy support and favorable economics, solar PV market demand and prices will continue to be robust, bringing healthy and sustainable profits to the solar manufacturing value chain.

High barriers to entry support existing industry leaders like Daqo

Polysilicon remained a drag on the whole solar PV manufacturing value chain in the first half of 2022, despite a 53.4% YoY rise in production volumes in China. Polysilicon remains one of the sectors with the highest barriers to entry, resulting in slow expansion growth due to difficulties in obtaining energy consumption approvals, protracted construction, and ramp-up times, combined with the operational inexperience of new companies. This mismatch will continue for a while, allowing the sector to benefit from robust market demand.

Embarking on polysilicon capacity expansion

In June 2022, Daqo New Energy’s main operating subsidiary, Xinjiang Daqo, sold private shares on the Shanghai Stock Exchange. The sale brought in a total of RMB 11 billion in gross proceeds. After the private offering is finished, Daqo New Energy will own about 81.26% of Xinjiang Daqo, down from 95.60%.

While the company did not share details as to whether the proceeds would go to their books, they did state that most of the offering’s proceeds will go towards the 100,000 MT Phase 5A polysilicon project in Inner Mongolia. This new project is being built right now, and it should be done by the end of the second quarter of 2023. The company can make about 130,000 MT of high-purity polysilicon per year at the moment. The primary output from 5A will start in Q1-2023 next year and be ramped up in Q2-2023.

Listing in Hong Kong under consideration

The SEC has reprimanded the Chinese companies that are listed in the United States because they did not follow the rules set by the Sarbanes-Oxley Act of 2002. In 2020, the U.S. Congress passed the Holding Foreign Companies Accountable Act (HFCAA), which prohibits companies from trading on U.S. exchanges if their audits of the past three consecutive years are not available. Several Chinese companies have been found to be out of compliance because they didn’t share data with U.S. regulators when asked to by Chinese authorities who were worried about national security.

Both countries are mulling over a workable deal, but delistings of Chinese companies over non-compliance are a real possibility as of today. Daqo commented on the issue in the last quarter’s earnings call and stated that the company is ‘seriously considering” a primary listing on Hong Kong Stock Exchange. If the company gets a primary listing in Hong Kong, it will be eligible for the Stock Connect program, which will let investors from mainland China trade the stock. This will lower the risk of the U.S. being taken off the list because investors in mainland China will be able to give a lot of money, in my opinion.

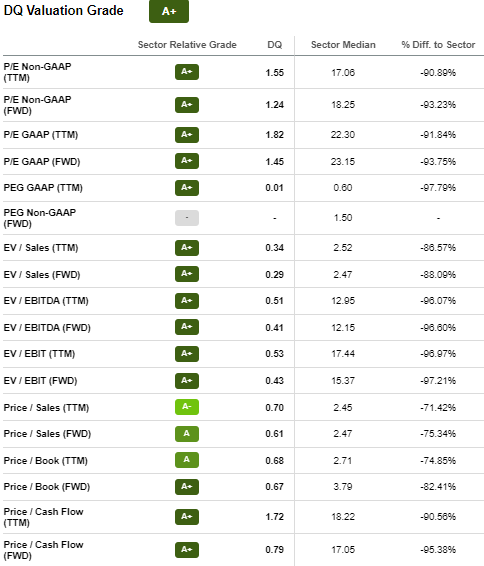

Valuation

The TTM and forward valuation metrics represent a sliver of green in an otherwise drab financial landscape, as the company’s relative valuation multiples are all below the median for its industry. Long-term investors view the current low price of the company as a golden opportunity to enter this burgeoning business at a discount.

Seeking Alpha

Risks

Regulatory risk for Chinese companies in the U.S. market is getting worse, which can lead to delisting and affect dividend payments to shareholders. This is one of Daqo’s downside risks. Moreover, a sharp decline in Polysilicon prices as new capacities come online in 2023 and a slower-than-expected ramp-up in production of the company’s new plant in Mongolia will also hamper any upside in the stock. A 23% reduction from the average 2022 wafer price of $0.13/W, as predicted by CEA, is possible by the end of 2023. This could lead to a drop in the price of polysilicon of about $10 per kilogram. It was recently speculated by BloombergNEF that by the end of 2023, there will be enough polysilicon production facilities to produce 500 GW of solar modules.

However, it appears that this risk is largely priced in. Some of these ratios are insanely low. A PE ratio of under 2 is nearly unheard of, especially for a company growing at the rate of DQ. Even though there is not a small amount of risk and positions shouldn’t be too big, the ridiculously low valuation and positive macroeconomic trends make this a good place to invest.

Conclusion

Polysilicon prices are expected to remain relatively stable in the coming quarters, as polysilicon capacity is arriving at a slower rate than previously anticipated. I think that putting money into solar infrastructure could help companies like Daqo. With the ramping up of 5A, which will take the total production capacity to 305,000 MT by 2024, the company will gain a larger market share in the PV segment. Moreover, I believe that Daqo’s valuation is cheap, and I see limited downside risk at this level.

Be the first to comment