shih-wei

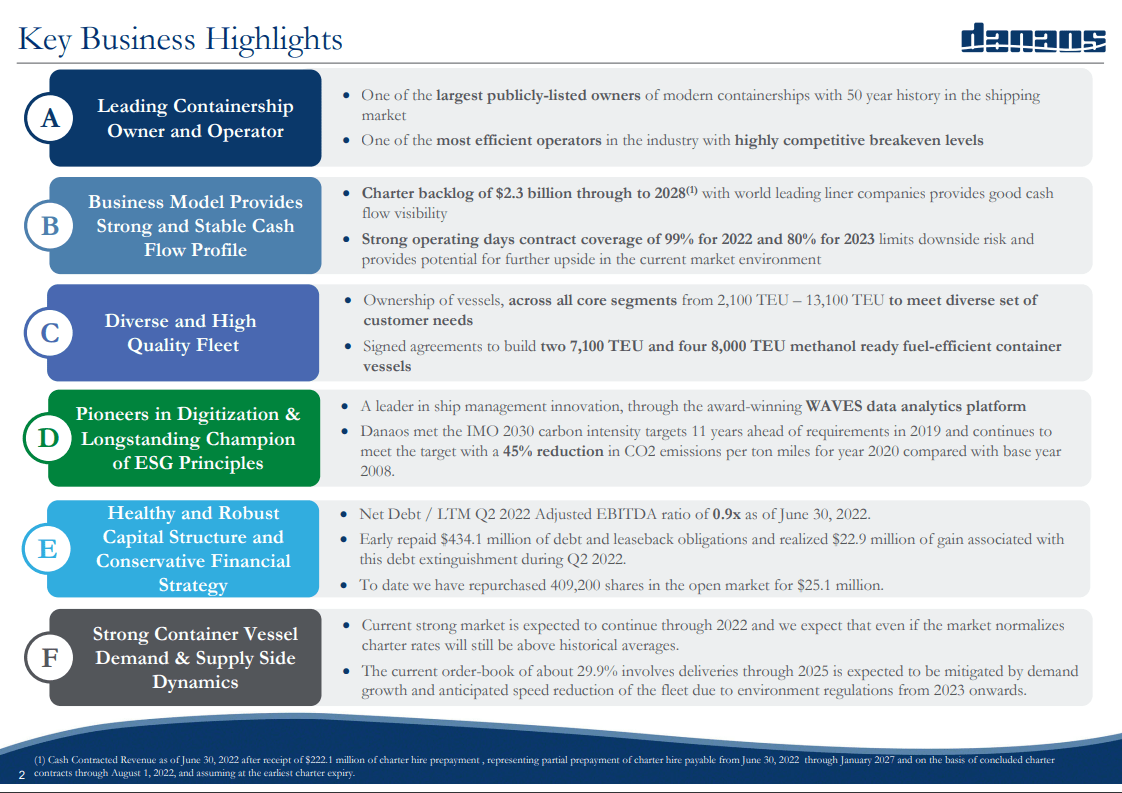

Danaos Corporation (NYSE:DAC) is a container shipping company with a market cap of ~$1.18 billion and an enterprise value of ~$1.57 billion. This translates to a share price of $54.45 per share. In the most recent quarter, the company generated earnings of $7.59 per share (a bit fattened by an incoming dividend from an equity holding). In containers, ships tend to get leased out a bit longer, and this helps with revenue and earnings visibility. At the end of the second quarter, contracted revenue added up to $2.3 billion. The average duration of contracts equating 3.6 years. 99% of its fleet was contracted out for 2022, 80% for 2023, and 55% over 2024. The company has a buyback program in place with $75 million left before it needs to go back to the board for authorization again.

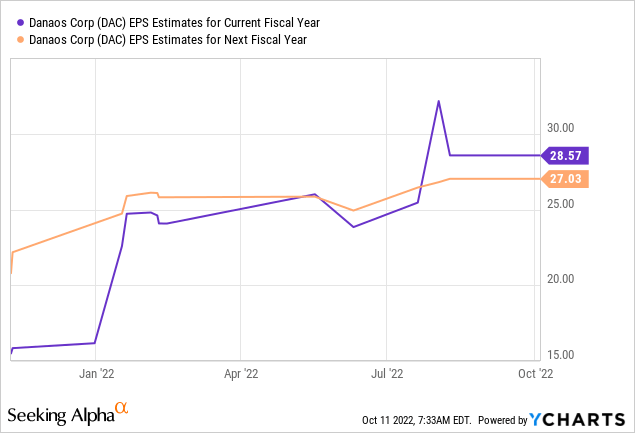

Analyst estimates look like this for this year and next:

Meanwhile, The company is ahead of the pack in terms of dealing with environmental regulation, which plays a big role in the future of shipping:

Danaos environmental regulation (Danaos)

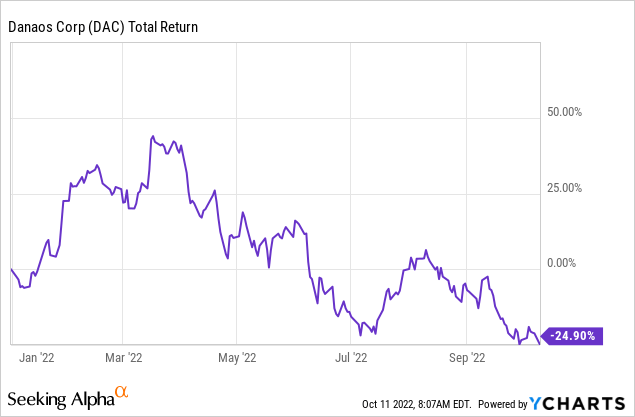

Why is this stock getting crushed in 2022?

First of all, lots of risk assets are getting crushed in 2022, and the stock is hardly exceptional outside of the energy complex.

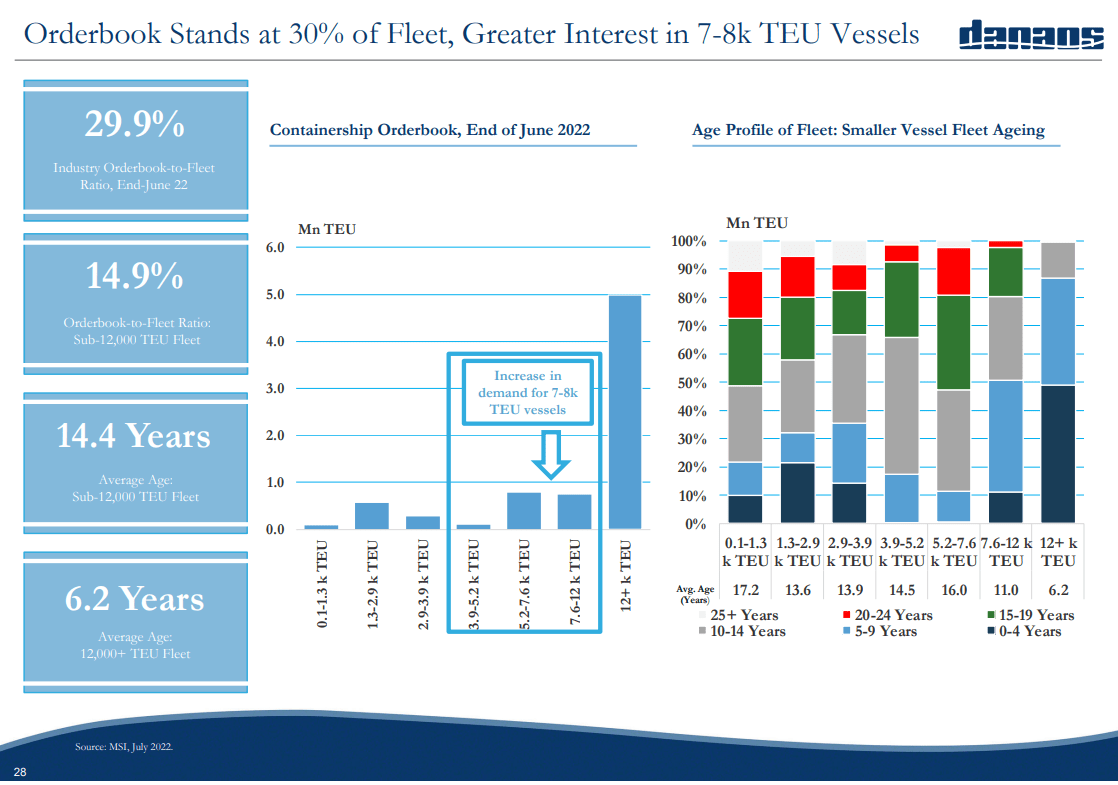

The company has a few new vessels arriving in the container market, that’s not great. They aren’t the only ones, either.

Fleet growth container shipping (Danaos)

Meanwhile, Maritime consultancy Hackett Associates projects a 2.9% decrease in TEU imports and a 9.6% fall for 2023. But remember that its fleet is utilized very well for this year and next.

container outlook (NRF & S&P Global Commodity Insights)

Next year should have an impact on the market and is likely to have a dampening effect on the available supply of vessels. Some vessels will likely be taken out of operation and/or decrease speed. At lower speeds, emissions are lower, and vessels are cheaper to operate in terms of fuel/mile.

What demand looks like in 2024 and beyond is anyone’s guess. By then, we may have gone through a recession, and the Fed may have stalled rate hikes and/or gone back to QE or even lower rates.

It’s also possible we’ll have a recession, the Fed keeps hiking rates slowly, and this is met with significant fiscal stimulus (the Russian war on Ukraine is the perfect backdrop).

An alternative scenario would be the Fed continuing to fight inflation, and governments worldwide obliging by refraining from stimulus as their economies are being squeezed.

In any case, I agree the immediate outlook isn’t exactly rosy and highly uncertain afterward. But there are valuations where uncertainty is quite acceptable to me.

That’s provided the wrong kind of uncertainty doesn’t result in my equity zeroing out through some kind of default. Shipping companies are known to go bankrupt from time to time. Danaos isn’t exactly the most obvious candidate, though. It just made $600 million in cash from operations in H1 2022.

In contrast, Danaos has around ~$900 million in debt. Around $300 million of that debt is fixed at 8.5%.

Danaos debt overview (Danaos)

Fixed-rate debt is quite sweet if the Fed continues to hike aggressively. The company has around $319 million in cash or equivalents at the end of June. Cash helps counterbalance some of the floating-rate debt. In addition, the company has a very interesting equity interest (~5,6 million shares) in container liner company ZIM Integrated Shipping Services Ltd. (ZIM). This equity interest is worth a whopping $134 million. In my humble opinion, ZIM shares are quite attractive as well.

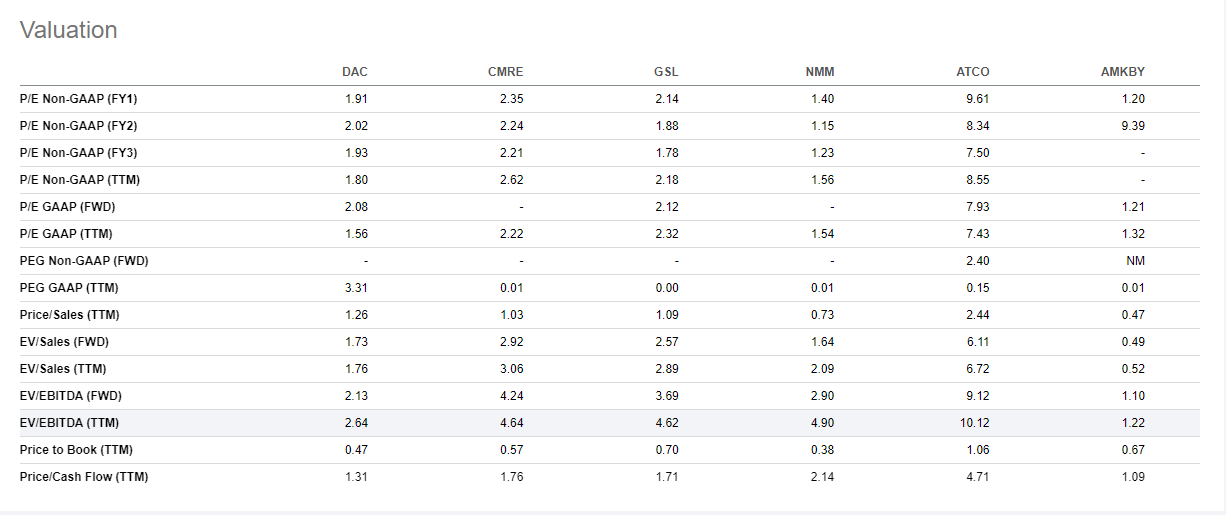

Container shipping valuations (Seeking Alpha)

With a big part of the fleet on highly profitable contracts and a huge revenue backlog, the cash balance and the equity interest, the debt load seems manageable even through a highly adverse period for containers. With a high probability of coming through the next containership downcycle, the company looks quite a bit too cheap at ~2x forward earnings, 1.7x forward sales, trading at less than 50% of book value, and ~2.13x forward EBITDA. Even among peers, the company trades cheap on most multiples before taking the ZIM equity interest into account.

Be the first to comment