xjben/iStock via Getty Images

Investment thesis

In my previous article covering the company, I rated Daktronics (NASDAQ:DAKT) shares a Buy given its leading position in the US market and attractive valuation at a P/E multiple of 9.2. I outlined my expectations for solid mid-single growth with rising margins in the medium term. The company’s Q1 fiscal 2025 results indicated that growth fell slightly short of my expectations, although margins remained strong. In addition to the weaker growth, I also attribute the subsequent share price drop to the uncertainty around the increased investments that management is making to improve the competitiveness of its products, while also improving the overall profitability of the company. Despite Daktronics differentiating itself from competitors through a more premium value proposition, which includes high-touch services and software control systems, the company needs to be more competitive with respect to pricing in order to generate solid revenue growth. Despite the risks I see, with the stock now trading at a P/E multiple of 8.5, I continue to find the valuation attractive, and therefore maintain my Buy rating.

Key takeaways from Q2 earnings and my expectations looking ahead

Q1 Earnings presentation

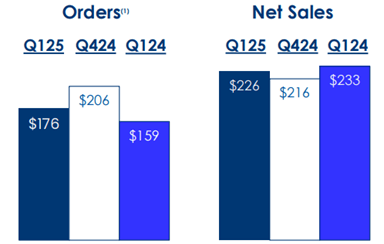

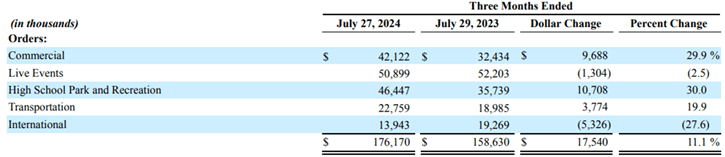

Net sales for Daktronics came in at $226 million in Q1, representing a 3% year-over-year decline, as shown above. Gross margins were strong at 26.4%, which led to operating margins remaining solid at 10%, a 100 basis point improvement versus the prior quarter. The company’s outlook for growth remained muted, given that the backlog declined to $267 million from $317 million at the end of the last quarter. This decline is likely explained by seasonality in the business, with the backlog likely to grow in Q3 and Q4. Though overall order growth remained healthy, growing 10% year over year, this was slightly lower than my expectations. As illustrated below, the High School and Transportation segments remain the primary drivers of growth. Meanwhile, Commercial orders have rebounded from last quarter’s weak intake, increasing by 30% year-over-year and 24% sequentially. International orders, though down year over year, have shown sequential improvements in the last two quarters, and continues to represent a large future growth opportunity for the company.

Q1 Financial report

The company’s gross margins continue to remain strong and have been trending higher. However, this has likely resulted in a lower overall growth rate. Discussing management’s priority to maintain pricing versus competitors while losing certain customers as a result, the company’s CEO stated:

In this price-sensitive – highly price sensitivity market, I suspect we don’t have as higher market share as we had previously going into COVID. In other areas, I believe we’ve been able to maintain our market share quite well.

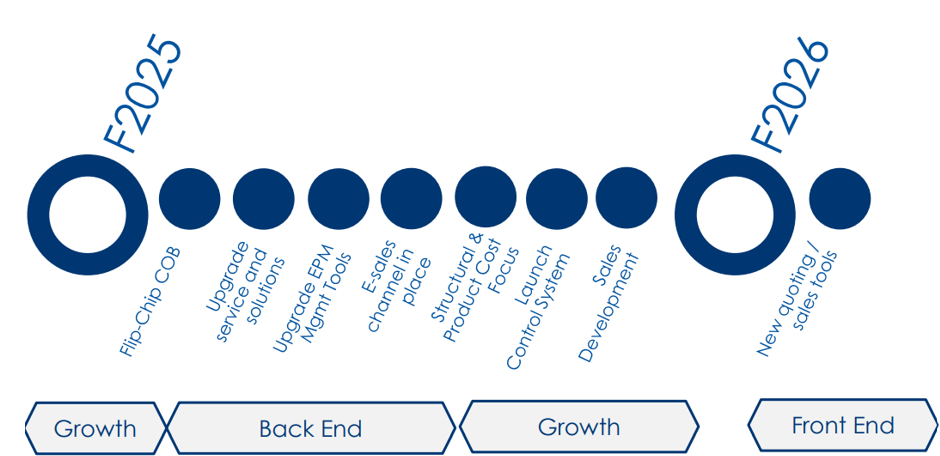

In order to make its products more competitive, management is aiming at leveraging its strong financial position to pursue a digital transformation with the aim of lowering product as well as structural costs. As depicted in the roadmap below, the investments span from optimizing the company’s sales and quoting process to introducing more software solutions that enable customers to control the products, including data access and storage in the cloud. While these investments are expected to add around $9 million in costs this year, I believe that if successful, this could result in increased market competitiveness for its products and structurally higher overall margins for the business.

Q1 Investor presentation

Valuation

Based on the company’s Q1 order intake and the expected seasonality implied in management’s guidance, I now expect annual revenue for fiscal 25 to be $830 million. This would imply an annual growth of 1.5%, versus my prior forecast of 5%. Despite the investments that management is making, I still expect operating margins to be approximately 10%, with capex of around $20 million. Consequently, operating income should be $83 million, with net income at around $67, assuming a 20% tax rate. This translates to earnings per share of $1.43, based on 47 million shares outstanding. At today’s share price of $12.2, shares are valued at a P/E multiple of 8.5. I expect FCF to align closely with net income, with more favorable working capital expected in the coming quarters. Given the company’s net cash position of $50 million, the valuation is even cheaper on an enterprise basis. However, I will point out that the company’s shares outstanding are likely to increase by 8.6% due to the $25 million convertible note due in 2027, which has a conversion price of $6.31 per share.

Given management’s ambition to grow annual revenue to $1 billion in the medium term, while also improving the company’s margin profile, I continue to find the current valuation appealing. Industry peers such as LSI Industries (LYTS) continue to trade at P/E multiples close to 16, while growing at mid-single-digit rates.

Risks

The biggest threat facing the company’s outlook for growth and profitability, according to me, is from competition. Daktronics continues to differentiate itself through its value-added services and software offerings. However, as I discussed previously, the company seems to be losing out to rivals from Southeast Asia when it comes to price-sensitive customers. One of the main factors driving the increased investments that management is making, is with the aim of lowering product costs.

Further economic weakness could negatively impact the company’s outlook, especially affecting orders from the commercial sector. However, the company’s broad customer base, which includes schools and government agencies, helps to mitigate this risk to a certain extent.

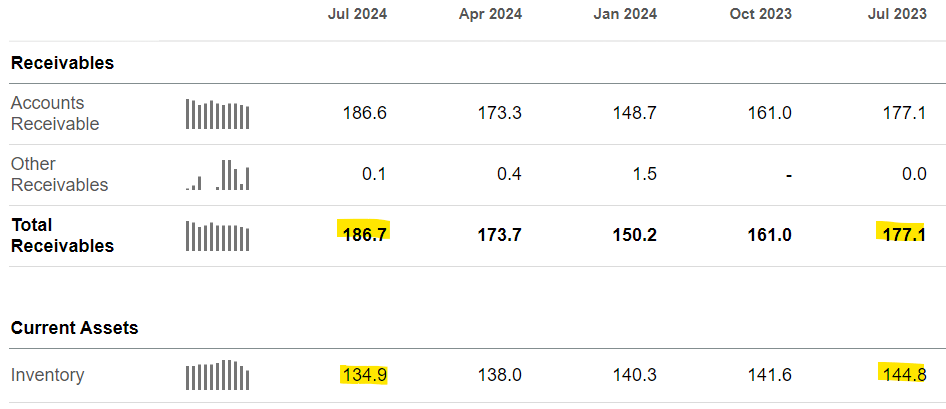

Another aspect that investors ought to pay close attention to is the growth in accounts receivable held on the balance sheet, as this will impact the business’s FCF generation. As shown below, management has prudently reduced inventory levels over the last few quarters, and I expect a similar dynamic to play out with respect to monetizing its accounts receivable, which should lead to improvements in FCF.

Seeking Alpha

Final thoughts

I believe that management’s strategic investments to increase the competitiveness of its product offering while also lowering the structural costs of the business is the right way forward for the company. Despite lowering my growth expectations in the near term, I still remain confident in the outlook for mid-single digit growth and margin improvement in the medium term. The company has a strong balance sheet and shares are attractively valued, which leads me to maintain my Buy rating.

Be the first to comment