CactuSoup

Energy security and food security are key investment themes for the next several years. Tight supply of both energy and food and increasing demand have been developing for years. The war in Ukraine has catapulted both to crisis level. CVR Partners, LP (NYSE:UAN), a variable MLP and a manufacturer of nitrogen fertilizers is well positioned to benefit from these two investment themes. UAN recently strengthened its balance sheet and completed major reliability enhancements in its manufacturing plants. I expect UAN to reward investors with out-sized cash distribution. UAN can turbocharge an income portfolio with just a small allocation. Furthermore, I see minimal downside risk at today’s unit price of around $102.

I have written many articles on UAN. I will refer you to my first article for background on the partnership. The only things I would add are that there are now about 10.6 million units outstanding after a reverse split, and that UAN has recently refinanced its debt to a lower interest rate and paid down $100 million of its debt. As a result, its quarterly cash interest expense has been reduced from about $15 million to about $8.5 million. All these improvements will help contribute to enhanced future cash distribution.

Energy security and food security will drive wide profit margin for UAN

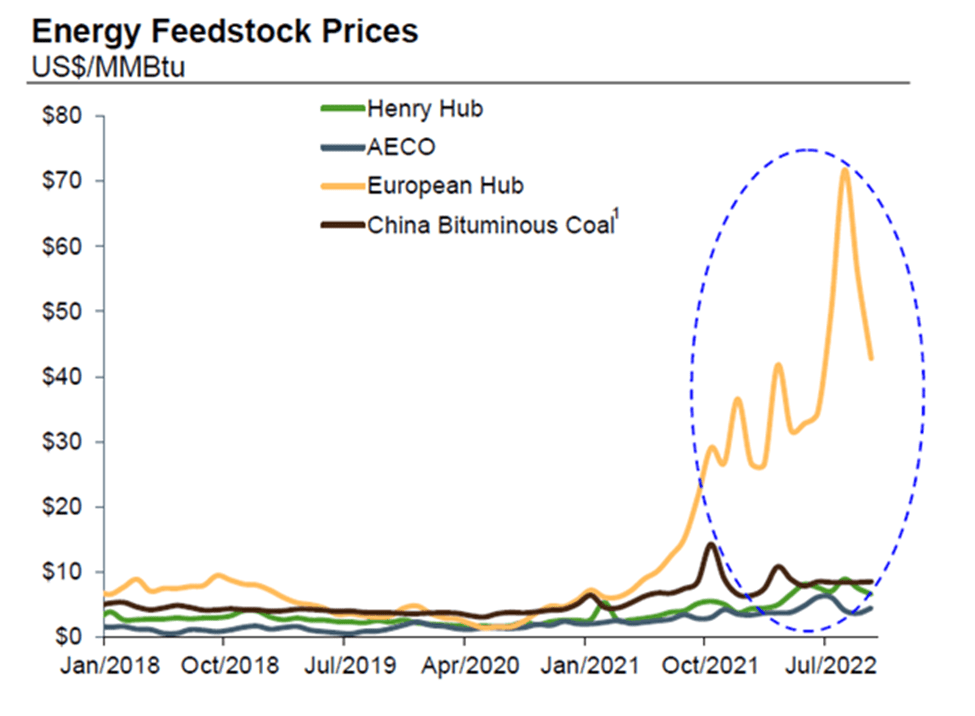

Much of Europe has been dependent on Russia for its oil and natural gas supply. When the war in Ukraine erupted, a series of events led to the European countries pivoting away from Russia as their natural gas supplier. Instead, they are buying liquified natural gas “LNG” from the US, Middle Eastern countries and African countries. Since LNG is a global commodity, the entry of the Europeans resulted in a significant increase in the spot price. European gas cost, as represented by the TTF benchmark, went up significantly (Figure 1).

Figure 1: European natural gas prices have increased significantly (Nutrient 3Q2022 earning release presentation)

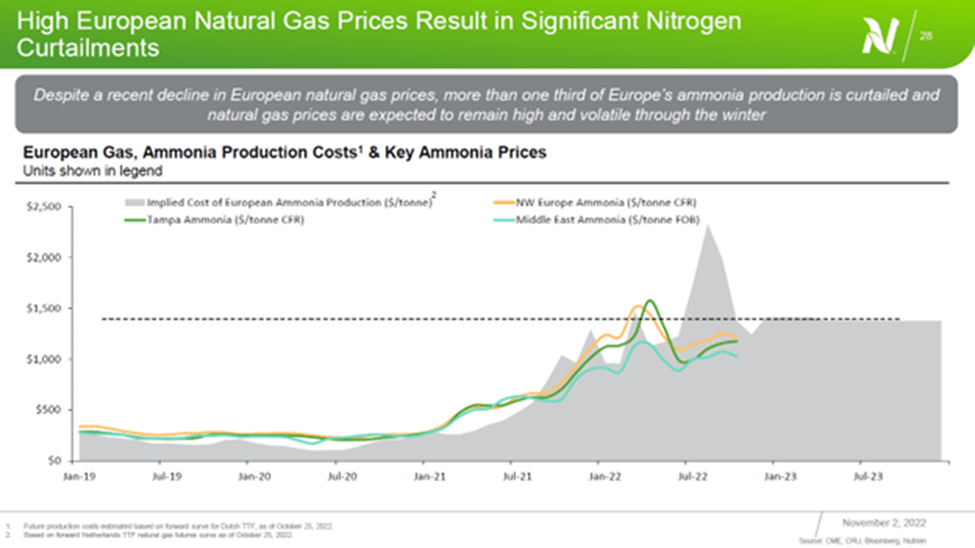

Since natural gas is the feedstock for nitrogen fertilizer (ammonia, urea, and urea ammonium nitrate) production, the rapid increase in gas price increases the cost of production for nitrogen fertilizers in Europe to a point that the cost of European manufacturers is higher than the price of the product. It is estimated that more than one third of Europe’s nitrogen fertilizer production has been curtailed (Figure 2).

Figure 2: More than one third of European ammonia production has been curtailed (Nutrient 3Q2022 earnings release presentation)

The curtailment of European production reduced worldwide supply and caused prices to increase significantly (Figure 3). While prices have been volatile, one can see that prices have generally increased from 2020 to 2021 and from 2021 to 2022.

It is widely believed that this energy security pivot away from Russian will cause sustained higher gas prices in Europe for at least several years to come, as the Europeans compete with the growing Asian countries for LNG. Hence, it is likely that energy security will continue to keep supply of nitrogen fertilizers tight, leading to sustained higher nitrogen fertilizer prices.

Figure 3: NOLA urea price history (Nutrient 3Q2022 earnings release presentation)

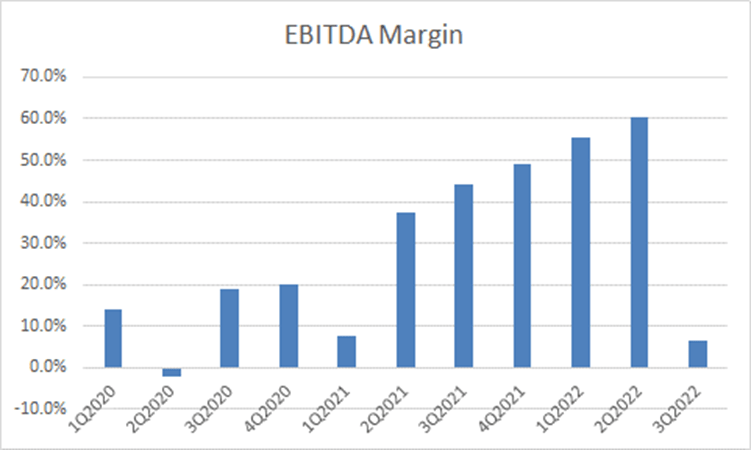

With Henry Hub prices significantly less than TTF prices (Figure 1), UAN enjoy a significant cost advantage. Hence, its profit margin has exploded (Figure 4). The dip in 2Q2021 was attributed to the disruption due to winter storm Uri. The dip in 3Q2022 was attributed to both plants down for at least a month for a turnaround and reliability upgrade.

Figure 4: UAN EBITDA margin history (Author’s work with data from company)

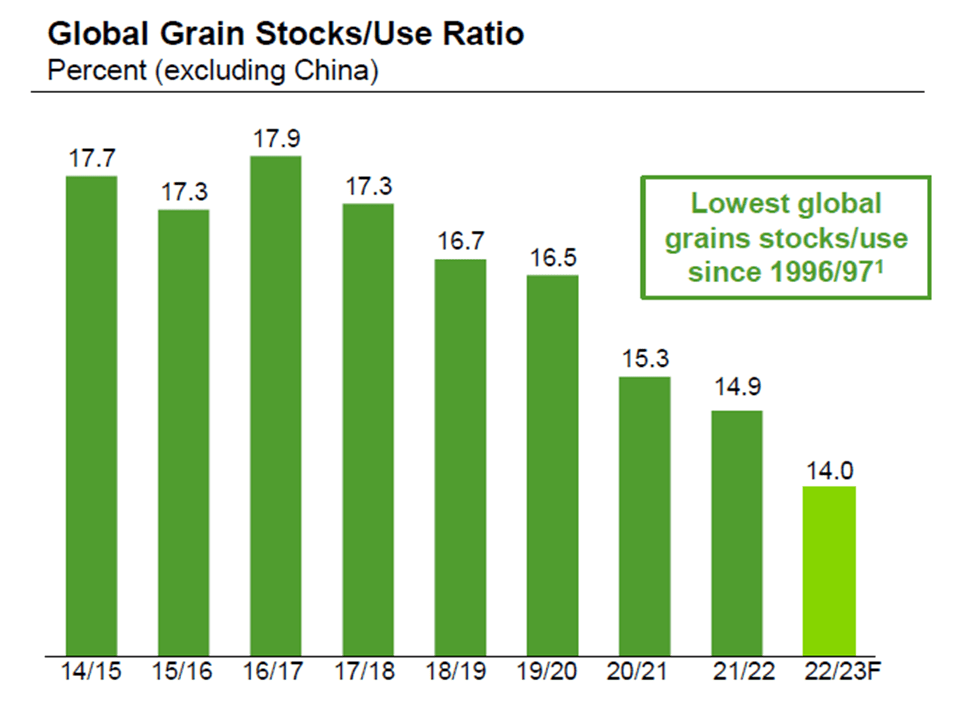

Food Security is driving tighter nitrogen fertilizer supply as well. Even before the war in Ukraine, grain supply has been getting tight (Figure 5). The world stock-to-use ratio has been declining for years and the war in Ukraine brought this issue to a crisis level. To protect their own food supply and to prevent sky-rocketing prices, many countries banned exports of grains and other food items.

Figure 5: Global grain stock/use ratio (Nutrient 3Q2022 earnings release presentation)

The stability of food supply and social order are extremely important to the Chinese government. Beginning in mid-2021, China restricted export to keep nitrogen fertilizers for its own growers. China, which typically export 5 million tonnes of urea per year, reduced its export to around 2 million tonnes in 2022.

Russia also restricted the export of nitrogen fertilizers in late 2021 to control the increase in domestic fertilizer prices. The goal was to contain domestic food inflation by assuring ample supply of fertilizers.

While some of these restrictions have been moderated during the off season, my expectation is that these restrictions will be enforced again before spring to ensure ample local supply. Hence, food security will continue to limit supply and help drive higher fertilizer prices worldwide.

UAN will likely make outsized distribution in the medium term

The energy security and food security issues will not be resolved in the short term. Hence, I expect that nitrogen fertilizer prices will stay elevated in the next two years, if not longer. This will result in outsized cash distribution for UAN unit holders.

UAN distributed a total of $20.48 per unit in the 4 quarters ended in 2Q2022. Taking into account of reduction in distributable cash flow “DCF” due to debt repayment, interest payment, reduction in DCF due to plant reliability and other items, I estimated that UAN’s pro forma DCF could have been as high as $38 per unit in that four-quarter period. The volume adjusted price of its urea ammonium nitrate product was $425 per ton in that period. This pro forma DCF estimation was described in a previous article. In the same article, I described that UAN has cleaned up its balance sheet and its plant reliability issues. Hence, I expect that with a similar product price for the next four quarters, UAN would be able to generate DCF in that same order of magnitude.

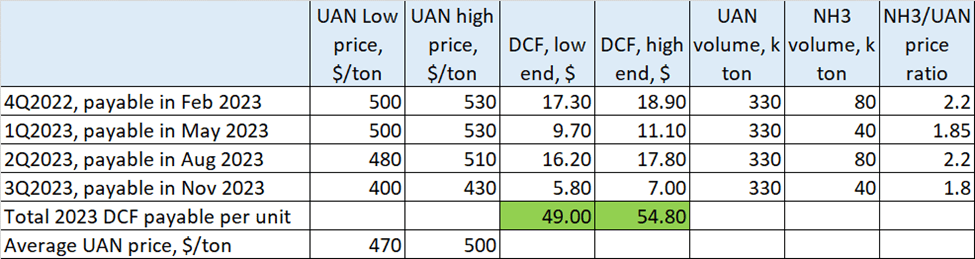

Cash distribution in 2023 will be affected by prices of products and plant utilization between October, 2022 and September, 2023. I believe that the prices for the October 2022 to March 2023 period are in the book as UAN has likely sold forward all of its 1Q2023 production. It is likely that UAN has partly sold forward its 2Q production as well. Given today’s future prices for 2Q2023, we can get a good estimation of 2Q2023 prices. Gate prices, and hence DCF for three of the four quarters for 2023 can be reasonably estimated, leaving only the 3Q prices to be determined.

After making some reasonable assumptions and using data available to me for prices for 4Q2022 and the first two quarters of 2023, and purely guessing 3Q2023 prices, I build a very simplified model for DCF for 2023. The results are shown in Figure 6. Figure 6 shows that my model yields a DCF per unit between $49 to $55 for 2023. The actual quarterly results may be different than the model. However, I believe that over the year, the DCF will likely fall within the range of the model results.

Given that UAN is trading around $102 per unit, this means that roughly half of the unit price may likely be returned to an investor over the next twelve months. And if the energy and food security issues continue in 2024, it is possible that similar DCF is possible.

Figure 6: A model for 2023 DCF (Author’s model)

The immediate question is: why is the unit price of UAN so low if we are looking at between $49 and $55 of distribution over the next twelve months? I think investors are gun shy due to (1) the volatility of fertilizer prices, (2) the concern that high fertilizer prices are not sustainable, (3) UAN has not had a consistent track record of DCF, and (4) income investors do not like a variable MLP, as they want a steady and hopefully consistently increasing dividend payout.

I believe that the energy and food security issues have fundamentally changed the landscape of the nitrogen fertilizer business. While fertilizer prices will be volatile, I believe that prices through a cycle will be substantially higher going forward. For income investors, I believe that allocating a small portion of their portfolio to UAN will turbocharge their portfolio yield with very low risk.

UAN can turbocharge the yield of an income portfolio with low downside risk

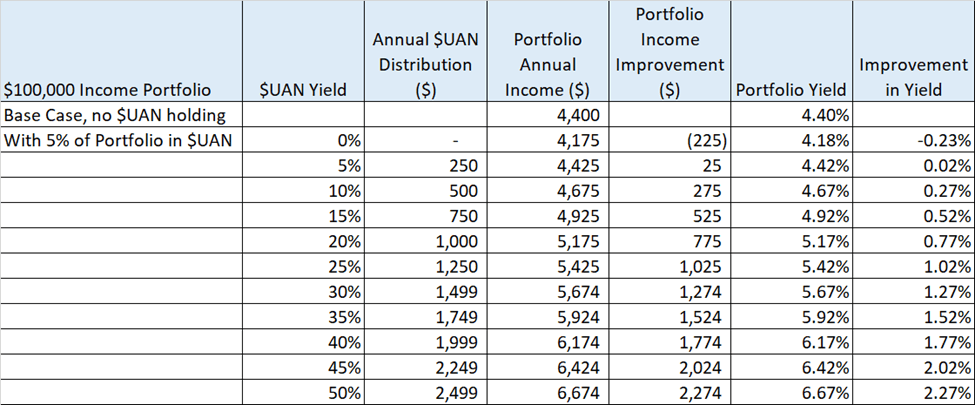

I have built a model of a $100,000 portfolio with 80% allocated to dividend stocks/MLPs, with an average yield of 4.5% (before investing in UAN), and with 20% allocated to money market fund with an yield of 4%. I further assume a change of the stock/MLP allocation by allocating 5% of the portfolio to UAN, while keeping the cash allocation at 20%. With these assumptions, I modeled the improvement in income and yield of this portfolio with varying UAN yield. This is shown in Figure 7.

Figure 7: A 5% allocation to UAN in an income portfolio can turbocharge income and yield (Author’s model)

Figure 7 shows that if my model of 2023 DCF is correct, a 5% allocation to UAN causes the portfolio’s income to improve by about $2,274 compared to a based case of $4,400. That is to say, a 5% allocation to UAN can potentially boast the income by a bit over 50%! The downside (if UAN distributes nothing) is that the portfolio income declines by $225 or about 5%. This is a high upside potential against a small downside risk. I think it is very unlikely that UAN will distribute $0 DCF in the next twelve months. In fact, urea ammonium nitrate prices have to decline to below $160 for a twelve-month period for UAN to not distribute any DCF. This is highly unlikely given the energy and food security issues that have fundamentally changed the landscape of the industry.

I believe also that the unit price of UAN will likely increase when UAN has established a more consistent DCF history. Even if investors demand a very high yield to compensate for the volatility of the fertilizer industry and a variable MLP structure, one can see that there is very high capital appreciation potential should UAN distribute about $50 per unit. Unit price will likely decline should UAN fails to make DCF distribution. However, I believe that the replacement cost of the plants, which I estimate to be between $2 to $2.5 billion (against a current EV of around $1.6 billion), will provide comfort for a long-term investor.

In addition to the risk of unit price volatility, the DCF estimation is subject to many risks. Weather, actual realized product prices, price of corn, farm profitability, resolution to the war in Ukraine, changes in the trade flow of fertilizers, inflation, interest rates, price of natural gas and LNG, price of oil and other factors may impact the price of fertilizers. UAN is also subject to operational issues, impacting the saleable volume of products. Changes in the price of gas and pet coke used in production will impact UAN’s cost of production. Government regulations regarding ethanol blending will affect the price of corn, and hence the demand for fertilizers. Other laws and regulations affecting farm economics and tax law changes that affect MLP ownership will affect UAN’s DCF and unit prices as well.

Takeaway

Energy and food security concerns have fundamentally changed the nitrogen fertilizer industry. UAN is well positioned to benefit from this change. For an income investor, UAN can provide an outsized upside benefit for income with a relatively small downside risk. The share price can be volatile, but may provide an upside benefit in the next twelve months as well.

Be the first to comment