OlenaMykhaylova

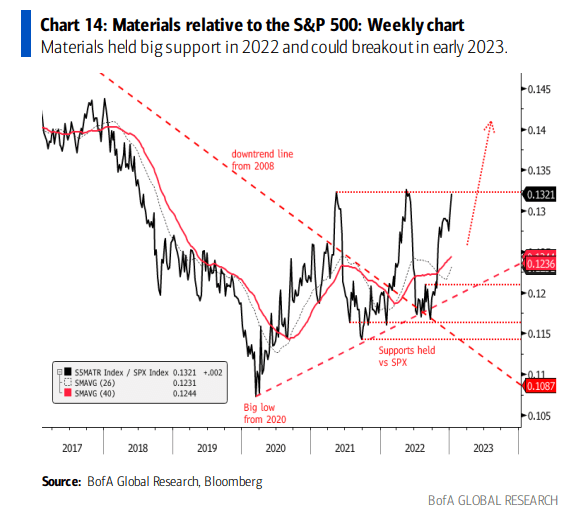

The Materials sector continues to help drive stocks off their mid-October lows. I like this look below from Steve Suttmeier at BofA. His technical work suggests that this small part of the S&P 500 could see more relative gains.

Not all stocks in the group are created equal, though. I see one name with a sketchy chart that is unfavored by all of Seeking Alpha’s factor grades. But what do I see when assessing the latest financials? Let’s dive in.

Materials: Triple-Top Relative Breakout On the Way?

BofA Global Research

According to Bank of America Global Research, with revenues of $11.4bn in 2021, Crown Holdings (NYSE:CCK) is a leading global supplier of metal packaging products (primarily beverage and food cans) to consumer products companies. CCK is organized as follows: Americas Beverage (39% of total sales), European Beverage (16%), Asia Pacific (12%), Transit Packaging (22%), and non-Reportable segment (11%). CCK operates in 47 countries with over 33,000 employees.

The Pennsylvania-based $10.5 billion market cap Container & Packaging industry company within the Materials sector has negative trailing 12-month GAAP earnings and pays a small 1.0% dividend yield, according to The Wall Street Journal.

CCK missed on earnings back in October, and the stock fell hard on the news driven by a guidance cut amid troubling inflationary pressure. The decline was apparently enough for activist investor Carl Icahn to take a stake in the packaging firm, though. That helped send the stock higher during the latter weeks of 2022. Meanwhile, Credit Suisse and BofA are high on CCK shares right now.

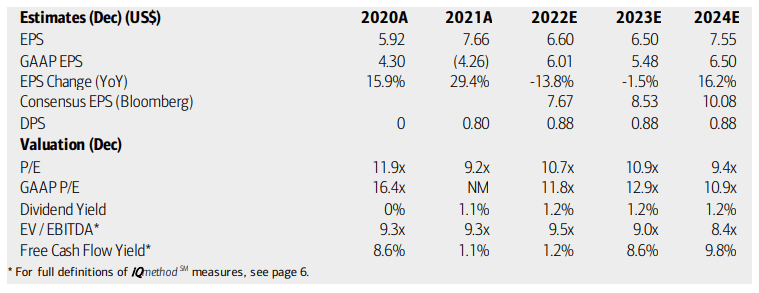

On valuation, analysts at BofA see earnings having fallen by more than 13% last year while EPS is expected to contract further to just $6.50 for 2023. Upside is then expected in 2024, though. The Bloomberg consensus forecast is considerably more upbeat about CCK’s per-share profit outlook. Dividends, meanwhile, are seen as holding at $0.88, so the yield remains light.

Both CCK’s operating and GAAP earnings multiples should hover in the low teens, below the market average, while the firm’s EV/EBITDA ratio is slightly underpriced relative to the S&P 500. With strong free cash flow expected this year, I see value in the shares despite Seeking Alpha’s sour ratings.

Crown Holdings: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

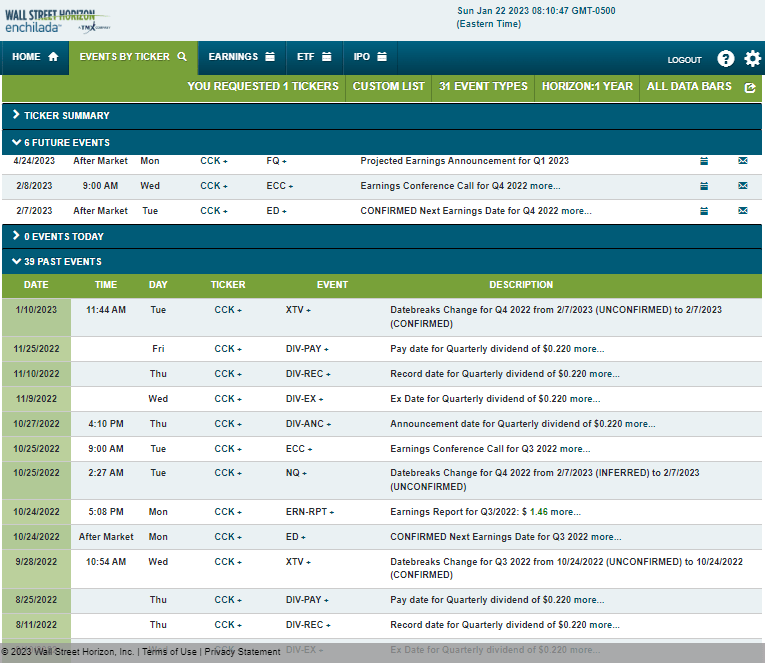

Looking ahead, corporate event data from Wall Street Horizon show a confirmed Q4 2022 earnings date of Tuesday, February 7 AMC with a conference call immediately after results cross the wires. You can listen live here. The calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Calendar

Wall Street Horizon

The Technical Take

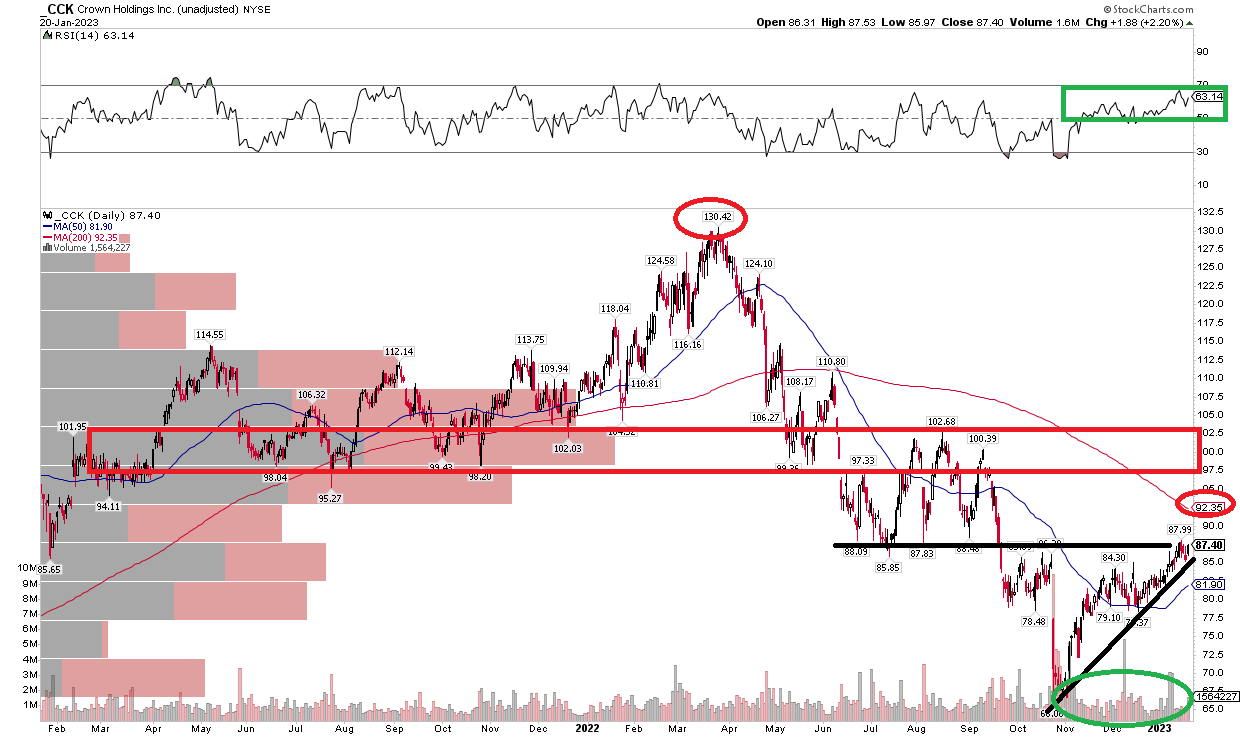

CCK completed a bearish head and shoulders topping pattern at its October-November low just under $70. Notice in the chart below that shares peaked near $130 in early 2022, then plunged but found support around $100. That $30 difference is then taken as a target off the $100 shoulder line to arrive at a roughly $70 target. Now that the pattern has been completed, it’s an all-clear to get long, right? Wrong.

Head and shoulders patterns are often continuation patterns just as much as reversals. In this case, the stock has retraced higher to the $88 mark – which is resistance from the July through September range last year. I see the risk of more downside here considering that the 200-day moving average is sloping downward and there is even more resistance seen in the $95 to $103 range as evidenced by high overhead supply of shares there. On the bullish side of the ledger are strong RSI momentum and positive volume trends lately.

Summing it all up, I see long-term support in the $60s and would be a buyer there. There’s significant technical work for the bulls to navigate through.

CCK: Bearish Ascending Wedge – Shares Encountering Resistance

Stockcharts.com

The Bottom Line

I like the valuation and free cash flow generation with Crown Holdings, but the chart warrants caution. It is one of those juxtapositions investors often face. I would be a buyer on a pullback if we get it, but I don’t want to go chasing the stock at clear resistance. I am a hold for now but hopefully can revisit this one later in 2023.

Be the first to comment